What is Global LCD Display Module Market?

The Global LCD Display Module Market refers to the worldwide industry focused on the production and sale of Liquid Crystal Display (LCD) modules. These modules are essential components in a wide range of electronic devices, serving as the interface through which users interact with technology. LCD modules are used in everything from smartphones and televisions to industrial equipment and automotive displays. The market encompasses various types of LCD technologies, including Twisted Nematic (TN), Super Twisted Nematic (STN), Vertical Alignment (VA), and Thin Film Transistor (TFT), each offering unique benefits and applications. The demand for LCD display modules is driven by the increasing need for high-quality displays in consumer electronics, advancements in display technology, and the growing adoption of smart devices. As technology continues to evolve, the LCD Display Module Market is expected to expand, offering more advanced and efficient display solutions to meet the diverse needs of consumers and industries worldwide. The market's growth is also influenced by factors such as technological innovations, consumer preferences, and the integration of LCD modules in emerging applications like smart homes and automotive systems.

TN, STN, VA, TFT, Others in the Global LCD Display Module Market:

In the Global LCD Display Module Market, various types of LCD technologies are utilized, each with distinct characteristics and applications. Twisted Nematic (TN) displays are among the most common types of LCDs, known for their fast response times and cost-effectiveness. They are widely used in applications where speed is crucial, such as gaming monitors and basic consumer electronics. However, TN displays often have limited viewing angles and color reproduction compared to other types. Super Twisted Nematic (STN) displays offer improved viewing angles and better contrast than TN displays, making them suitable for devices like calculators and older mobile phones. STN technology is often used in applications where cost is a significant factor, and high color fidelity is not a primary requirement. Vertical Alignment (VA) displays provide better color reproduction and wider viewing angles than TN and STN displays. They are commonly used in televisions and computer monitors where image quality is important. VA technology offers a good balance between performance and cost, making it a popular choice for mid-range display applications. Thin Film Transistor (TFT) displays represent a more advanced type of LCD technology, offering superior image quality, color accuracy, and viewing angles. TFT displays are used in high-end devices such as smartphones, tablets, and premium monitors. They are also more expensive to produce, which is reflected in the cost of devices that use them. Other types of LCD technologies include In-Plane Switching (IPS) and Advanced Fringe Field Switching (AFFS), which are variations of TFT technology designed to further enhance color accuracy and viewing angles. These technologies are often used in professional-grade monitors and devices where display quality is paramount. The choice of LCD technology in a particular application depends on factors such as cost, performance requirements, and the intended use of the device. As the Global LCD Display Module Market continues to evolve, manufacturers are constantly innovating to improve the performance and efficiency of LCD technologies, catering to the diverse needs of consumers and industries.

Smart Home, Smart Finance, Communication Equipment, Industrial Automation, Utilities, Healthcare, Automotive, Others in the Global LCD Display Module Market:

The Global LCD Display Module Market finds extensive usage across various sectors, each benefiting from the unique advantages offered by LCD technology. In the realm of Smart Homes, LCD modules are integral to devices such as smart thermostats, security systems, and home automation panels, providing intuitive interfaces for users to control and monitor their environments. In Smart Finance, LCD displays are used in ATMs, point-of-sale terminals, and digital signage, offering clear and reliable interfaces for financial transactions and information dissemination. Communication Equipment, such as smartphones and tablets, relies heavily on LCD technology for vibrant and responsive displays that enhance user experience. In Industrial Automation, LCD modules are used in control panels and monitoring systems, providing operators with critical data and system status updates in real-time. Utilities also benefit from LCD technology, with applications in smart meters and grid management systems that require reliable and energy-efficient displays. In Healthcare, LCD displays are used in medical devices and diagnostic equipment, offering precise and clear visuals that are crucial for patient care and monitoring. The Automotive sector utilizes LCD modules in dashboards, infotainment systems, and rear-seat entertainment, enhancing the driving experience with high-quality visuals and interactive interfaces. Other areas where LCD display modules are used include education, retail, and transportation, each leveraging the technology's versatility and efficiency to improve functionality and user engagement. As the demand for smart and connected devices continues to grow, the Global LCD Display Module Market is poised to expand its reach across these diverse sectors, offering innovative solutions that enhance the way we interact with technology.

Global LCD Display Module Market Outlook:

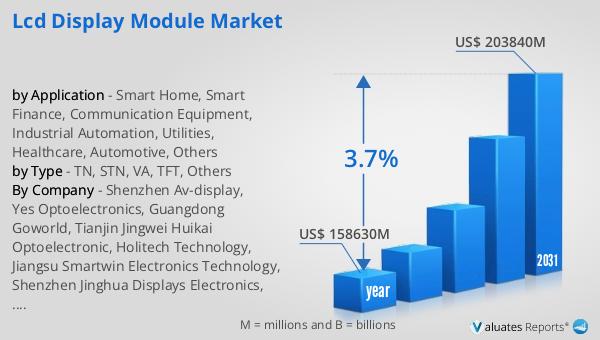

The global market for LCD Display Modules was valued at $158.63 billion in 2024 and is anticipated to grow to a revised size of $203.84 billion by 2031, reflecting a compound annual growth rate (CAGR) of 3.7% during the forecast period. This growth trajectory underscores the increasing demand for LCD display modules across various industries and applications. The market's expansion is driven by the rising adoption of smart devices, advancements in display technology, and the growing need for high-quality visual interfaces in consumer electronics, automotive, healthcare, and industrial sectors. As technology continues to evolve, LCD display modules are becoming more sophisticated, offering enhanced performance, energy efficiency, and versatility. This has led to their widespread adoption in emerging applications such as smart homes, smart finance, and communication equipment. The market's growth is also supported by the increasing integration of LCD modules in automotive systems, healthcare devices, and industrial automation, where reliable and efficient displays are essential. As a result, the Global LCD Display Module Market is expected to continue its upward trajectory, providing innovative solutions that cater to the diverse needs of consumers and industries worldwide.

| Report Metric | Details |

| Report Name | LCD Display Module Market |

| Accounted market size in year | US$ 158630 million |

| Forecasted market size in 2031 | US$ 203840 million |

| CAGR | 3.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Shenzhen Av-display, Yes Optoelectronics, Guangdong Goworld, Tianjin Jingwei Huikai Optoelectronic, Holitech Technology, Jiangsu Smartwin Electronics Technology, Shenzhen Jinghua Displays Electronics, Shenzhen Solarbrite Display, Jenson Display, Techshine Electronics, Raystar Optronics, Winstar Display, Ampire |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |