What is Global Dental Imaging Devices Market?

The Global Dental Imaging Devices Market is a rapidly evolving sector within the broader medical device industry, focusing on technologies that assist dental professionals in diagnosing and treating oral health issues. These devices are crucial for capturing detailed images of teeth, gums, and other oral structures, enabling dentists to make accurate diagnoses and develop effective treatment plans. The market encompasses a wide range of products, including both 2D and 3D imaging devices, each offering unique benefits and applications. As dental health awareness increases globally, the demand for advanced imaging technologies is on the rise. This growth is driven by factors such as the increasing prevalence of dental disorders, advancements in imaging technology, and the growing adoption of digital dental imaging systems. Additionally, the integration of artificial intelligence and machine learning in dental imaging is expected to further enhance diagnostic accuracy and efficiency. Overall, the Global Dental Imaging Devices Market plays a vital role in improving dental care quality, making it an essential component of modern dentistry.

2D Imaging Devices, 3D Imaging Devices in the Global Dental Imaging Devices Market:

2D imaging devices are a fundamental part of the Global Dental Imaging Devices Market, providing essential tools for dental professionals to capture detailed images of the oral cavity. These devices include traditional X-ray machines and digital radiography systems, which have been used for decades to diagnose a wide range of dental conditions. 2D imaging is particularly useful for identifying cavities, assessing bone levels, and evaluating the health of the roots and surrounding bone. The simplicity and cost-effectiveness of 2D imaging make it a popular choice for routine dental examinations. However, the limitations of 2D imaging, such as the inability to capture depth and the potential for overlapping structures, have led to the development of more advanced technologies. On the other hand, 3D imaging devices represent a significant advancement in dental imaging technology, offering a more comprehensive view of the oral structures. These devices, such as cone beam computed tomography (CBCT) scanners, provide detailed three-dimensional images that allow for more accurate diagnosis and treatment planning. 3D imaging is particularly beneficial for complex procedures such as implant placement, orthodontic assessments, and the evaluation of temporomandibular joint disorders. The ability to visualize the oral cavity in three dimensions helps dental professionals to better understand the spatial relationships between different structures, leading to improved treatment outcomes. Despite the higher cost and complexity of 3D imaging devices, their benefits in terms of diagnostic accuracy and patient care make them an increasingly popular choice in modern dentistry. As technology continues to advance, the integration of 2D and 3D imaging devices is expected to further enhance the capabilities of dental professionals, ultimately improving patient outcomes and satisfaction.

Hospitals, Clinics, Dental Clinics in the Global Dental Imaging Devices Market:

The usage of Global Dental Imaging Devices Market in hospitals, clinics, and dental clinics is integral to the delivery of high-quality dental care. In hospitals, dental imaging devices are used to support a wide range of dental and maxillofacial procedures. These devices enable hospital-based dental professionals to accurately diagnose and treat complex conditions, such as facial trauma, oral cancers, and congenital anomalies. The availability of advanced imaging technologies in hospitals ensures that patients receive comprehensive care, often involving multidisciplinary teams. In clinics, dental imaging devices play a crucial role in routine dental examinations and preventive care. Clinics often rely on 2D imaging devices for their cost-effectiveness and ease of use, allowing dental professionals to quickly assess the oral health of patients and identify any potential issues. However, as the demand for more precise diagnostics increases, many clinics are also incorporating 3D imaging devices into their practice. Dental clinics, which specialize in oral health care, are at the forefront of adopting advanced imaging technologies. These clinics utilize both 2D and 3D imaging devices to provide a wide range of services, from routine check-ups to complex surgical procedures. The use of dental imaging devices in these settings enhances the accuracy of diagnoses, improves treatment planning, and ultimately leads to better patient outcomes. The integration of digital imaging systems in dental clinics also facilitates better communication with patients, as they can easily visualize their oral health conditions and understand the proposed treatment plans. Overall, the use of dental imaging devices in hospitals, clinics, and dental clinics is essential for delivering high-quality dental care and improving patient satisfaction.

Global Dental Imaging Devices Market Outlook:

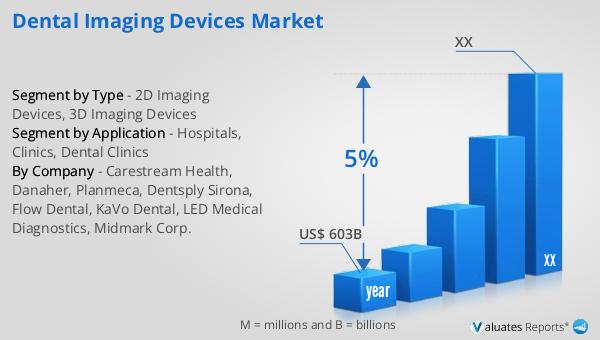

Based on our research, the global market for medical devices, which includes dental imaging devices, is projected to reach approximately $603 billion in 2023. This market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare expenditure, and the rising prevalence of chronic diseases. The demand for innovative medical devices, such as advanced dental imaging technologies, is expected to rise as healthcare providers seek to improve diagnostic accuracy and patient outcomes. Additionally, the growing awareness of oral health and the increasing adoption of digital dental imaging systems are contributing to the expansion of the dental imaging devices market. As the market continues to evolve, manufacturers are focusing on developing more efficient and user-friendly devices to meet the needs of dental professionals and patients. The integration of artificial intelligence and machine learning in dental imaging is also expected to play a significant role in shaping the future of the market. Overall, the global medical devices market, including dental imaging devices, is poised for significant growth, driven by the increasing demand for advanced healthcare solutions and the continuous innovation in medical technology.

| Report Metric | Details |

| Report Name | Dental Imaging Devices Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Carestream Health, Danaher, Planmeca, Dentsply Sirona, Flow Dental, KaVo Dental, LED Medical Diagnostics, Midmark Corp. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |