What is Specialty Nylon - Global Market?

Specialty nylon refers to a category of advanced nylon materials that are engineered to meet specific performance requirements across various industries. These materials are distinguished from standard nylon by their enhanced properties, such as increased strength, durability, and resistance to environmental factors. Specialty nylons are used in applications where traditional materials may not suffice, offering solutions that require high performance under challenging conditions. The global market for specialty nylon is driven by the demand for materials that can withstand extreme temperatures, resist chemical exposure, and maintain structural integrity over time. Industries such as automotive, electronics, and textiles are increasingly adopting specialty nylon due to its versatility and reliability. As technology advances and industries seek more efficient and sustainable materials, the demand for specialty nylon is expected to grow. This growth is fueled by innovations in manufacturing processes and the development of new nylon composites that offer even greater performance benefits. The specialty nylon market is characterized by a diverse range of products, each tailored to meet the specific needs of different applications, making it a dynamic and evolving sector within the global materials market.

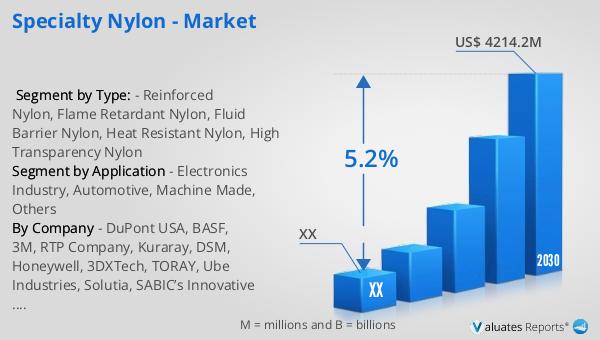

Reinforced Nylon, Flame Retardant Nylon, Fluid Barrier Nylon, Heat Resistant Nylon, High Transparency Nylon in the Specialty Nylon - Global Market:

Reinforced nylon is a type of specialty nylon that is enhanced with fillers such as glass fibers or carbon fibers to improve its mechanical properties. This reinforcement significantly increases the material's strength, stiffness, and impact resistance, making it ideal for applications that require high structural integrity. Reinforced nylon is commonly used in the automotive industry for components like engine covers, intake manifolds, and structural parts, where durability and weight reduction are crucial. Flame retardant nylon, on the other hand, is engineered to resist ignition and slow down the spread of fire. This type of nylon is essential in industries where safety is a priority, such as electronics and construction. It is used in the manufacturing of electrical connectors, circuit breakers, and other components that must adhere to strict fire safety standards. Fluid barrier nylon is designed to resist the penetration of liquids and gases, making it suitable for applications in the chemical and medical industries. This type of nylon is often used in the production of protective clothing, seals, and gaskets that require a high level of impermeability. Heat resistant nylon is formulated to withstand high temperatures without degrading, making it ideal for use in environments where thermal stability is essential. This type of nylon is used in automotive and industrial applications where components are exposed to high heat, such as under-the-hood parts and machinery components. High transparency nylon is a specialty nylon that offers excellent clarity and optical properties, making it suitable for applications that require transparency and aesthetic appeal. This type of nylon is used in the production of lenses, light covers, and other components where visual clarity is important. Each of these specialty nylons is designed to meet specific performance criteria, providing solutions for a wide range of industrial challenges. The global market for specialty nylon continues to expand as industries seek materials that offer superior performance and reliability.

Electronics Industry, Automotive, Machine Made, Others in the Specialty Nylon - Global Market:

Specialty nylon finds extensive usage across various industries due to its unique properties and adaptability. In the electronics industry, specialty nylon is used for manufacturing components that require high precision and reliability. Its flame retardant properties make it an ideal choice for electrical connectors, circuit boards, and housings, where safety is paramount. The material's ability to withstand high temperatures and resist chemical exposure ensures that electronic components remain functional and safe over extended periods. In the automotive sector, specialty nylon is utilized for its strength, lightweight nature, and resistance to wear and tear. It is used in the production of engine components, fuel systems, and interior parts, contributing to overall vehicle efficiency and performance. The use of reinforced nylon in automotive applications helps reduce vehicle weight, leading to improved fuel efficiency and reduced emissions. In machine-made applications, specialty nylon is employed for its durability and resistance to abrasion. It is used in the manufacturing of gears, bearings, and other mechanical components that require long-lasting performance under continuous stress. The material's ability to maintain structural integrity under high loads makes it a preferred choice for industrial machinery and equipment. Beyond these industries, specialty nylon is also used in various other applications, such as textiles, sports equipment, and consumer goods. Its versatility and performance characteristics make it suitable for a wide range of products, from high-performance fabrics to durable consumer electronics. As industries continue to evolve and demand more advanced materials, the role of specialty nylon in providing innovative solutions is expected to grow, driving further advancements in material science and engineering.

Specialty Nylon - Global Market Outlook:

The global market for specialty nylon was valued at approximately $2,936 million in 2023. This market is projected to expand significantly, reaching an estimated size of $4,214.2 million by 2030. This growth represents a compound annual growth rate (CAGR) of 5.2% over the forecast period from 2024 to 2030. The North American market for specialty nylon, although not specified in exact figures, is also expected to experience growth during this period. The increasing demand for high-performance materials across various industries, such as automotive, electronics, and textiles, is a key driver of this market expansion. As industries continue to seek materials that offer superior performance, durability, and sustainability, the specialty nylon market is poised for significant growth. The development of new nylon composites and advancements in manufacturing processes are expected to further enhance the market's potential. This growth trajectory highlights the importance of specialty nylon as a critical material in addressing the evolving needs of modern industries. The market's expansion reflects the ongoing innovation and adaptation within the specialty nylon sector, positioning it as a vital component of the global materials market.

| Report Metric | Details |

| Report Name | Specialty Nylon - Market |

| Forecasted market size in 2030 | US$ 4214.2 million |

| CAGR | 5.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | DuPont USA, BASF, 3M, RTP Company, Kuraray, DSM, Honeywell, 3DXTech, TORAY, Ube Industries, Solutia, SABIC’s Innovative Plastics, Mitsubishi Group, WEIFANG DONGSHENG PLASTIC TECHNOLOGY CO.,LTD, Julier Technology, Shakespeare, Royal DSM N.V, Lanxess |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |