What is X-ray Therapy Equipment - Global Market?

X-ray therapy equipment is a crucial component in the global medical device market, primarily used for therapeutic purposes rather than diagnostic. This equipment utilizes high-energy radiation to treat various medical conditions, most notably cancer. The global market for X-ray therapy equipment is driven by the increasing prevalence of cancer and advancements in technology that enhance the precision and effectiveness of treatments. These devices are designed to target and destroy cancerous cells while minimizing damage to surrounding healthy tissues. The market is characterized by continuous innovation, with manufacturers focusing on developing more efficient and patient-friendly devices. Additionally, the rising demand for non-invasive treatment options and the growing awareness about early cancer detection and treatment contribute to the market's expansion. As healthcare systems worldwide strive to improve cancer care, the demand for X-ray therapy equipment is expected to grow, making it a vital segment of the medical device industry. The market's growth is also supported by government initiatives and funding aimed at improving cancer treatment infrastructure. Overall, the X-ray therapy equipment market plays a significant role in enhancing patient outcomes and advancing cancer treatment globally.

Breast Cancer Treatment, Skin Cancer Treatment, Vulvar Cancer Treatment, Others in the X-ray Therapy Equipment - Global Market:

X-ray therapy equipment is pivotal in the treatment of various types of cancer, including breast cancer, skin cancer, vulvar cancer, and others. In breast cancer treatment, X-ray therapy, also known as radiation therapy, is often used post-surgery to eliminate any remaining cancer cells and reduce the risk of recurrence. It can be administered externally or internally, depending on the specific needs of the patient. The precision of modern X-ray therapy equipment allows for targeted treatment, minimizing exposure to surrounding healthy tissues and reducing side effects. In skin cancer treatment, X-ray therapy is particularly effective for non-melanoma skin cancers, such as basal cell carcinoma and squamous cell carcinoma. It is often used when surgery is not feasible or as an adjunct to surgical procedures. The ability to precisely target cancerous lesions makes X-ray therapy a valuable tool in dermatological oncology. Vulvar cancer treatment also benefits from X-ray therapy, especially in cases where surgery alone is insufficient. Radiation therapy can be used to shrink tumors before surgery or to target residual cancer cells post-operatively. The adaptability of X-ray therapy equipment to different cancer types and stages makes it an essential component of comprehensive cancer care. Beyond these specific cancers, X-ray therapy is employed in the treatment of various other malignancies, including head and neck cancers, prostate cancer, and certain types of lymphoma. The versatility of X-ray therapy equipment allows for its application across a wide range of oncological conditions, providing patients with effective treatment options tailored to their individual needs. As technology continues to advance, the precision and efficacy of X-ray therapy are expected to improve, further enhancing its role in cancer treatment. The global market for X-ray therapy equipment is thus driven by the increasing demand for effective cancer treatments and the continuous development of innovative technologies that improve patient outcomes.

Hospital, Clinic, Ambulatory Surgery Center, Others in the X-ray Therapy Equipment - Global Market:

The usage of X-ray therapy equipment spans various healthcare settings, including hospitals, clinics, ambulatory surgery centers, and others. In hospitals, X-ray therapy equipment is a critical component of oncology departments, where it is used to treat a wide range of cancers. Hospitals often have the infrastructure and resources to support advanced X-ray therapy equipment, allowing them to offer comprehensive cancer care. The availability of multidisciplinary teams in hospitals ensures that patients receive holistic treatment plans that incorporate X-ray therapy as a key modality. In clinics, X-ray therapy equipment is used to provide outpatient cancer treatment services. Clinics often focus on specific types of cancer or offer specialized radiation therapy services, making them an accessible option for patients who require regular treatment sessions. The compact design and ease of use of modern X-ray therapy equipment make it suitable for clinic settings, where space and resources may be limited. Ambulatory surgery centers also utilize X-ray therapy equipment, particularly for pre-operative and post-operative cancer treatments. These centers offer a convenient alternative to hospital-based care, providing patients with access to radiation therapy in a less formal setting. The flexibility of X-ray therapy equipment allows it to be integrated into the treatment protocols of ambulatory surgery centers, enhancing their ability to deliver comprehensive cancer care. Beyond these traditional healthcare settings, X-ray therapy equipment is also used in research institutions and academic centers, where it plays a role in clinical trials and the development of new cancer treatment protocols. The versatility and adaptability of X-ray therapy equipment make it a valuable asset across various healthcare environments, contributing to the global effort to improve cancer treatment outcomes. As the demand for cancer treatment continues to rise, the utilization of X-ray therapy equipment in diverse healthcare settings is expected to grow, further solidifying its importance in the medical device market.

X-ray Therapy Equipment - Global Market Outlook:

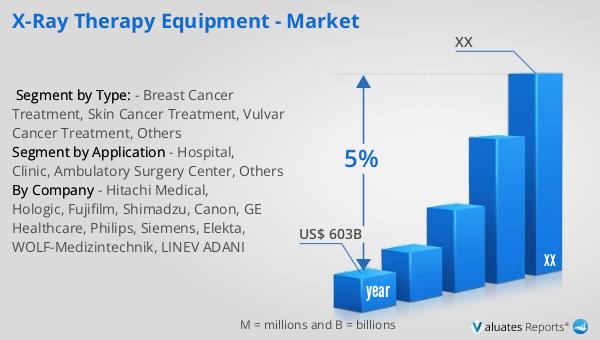

Based on our research, the global market for medical devices, including X-ray therapy equipment, is projected to be valued at approximately USD 603 billion in 2023. This market is anticipated to experience a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for minimally invasive treatment options. The medical device market encompasses a wide range of products, from diagnostic imaging equipment to therapeutic devices like X-ray therapy equipment. The growing awareness of early disease detection and the importance of timely treatment are also contributing to the expansion of the market. Additionally, government initiatives and healthcare reforms aimed at improving access to quality healthcare services are expected to support market growth. The continuous development of innovative medical devices that enhance patient outcomes and improve the efficiency of healthcare delivery is a key driver of the market's expansion. As healthcare systems worldwide strive to meet the evolving needs of patients, the demand for advanced medical devices, including X-ray therapy equipment, is expected to increase, further fueling market growth.

| Report Metric | Details |

| Report Name | X-ray Therapy Equipment - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Hitachi Medical, Hologic, Fujifilm, Shimadzu, Canon, GE Healthcare, Philips, Siemens, Elekta, WOLF-Medizintechnik, LINEV ADANI |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |