What is Open-circuit Self Contained Breathing Apparatus - Global Market?

Open-circuit Self Contained Breathing Apparatus (SCBA) is a critical safety device used globally, primarily in environments where the air is contaminated or oxygen-deficient. This apparatus is designed to provide the wearer with a supply of breathable air, independent of the surrounding atmosphere. It consists of a high-pressure tank, a pressure regulator, and an inhalation connection, such as a mouthpiece, mouth mask, or face mask, connected together and mounted on a carrying frame. The open-circuit design means that exhaled air is released into the environment, as opposed to being recirculated. This type of SCBA is widely used in various industries, including firefighting, industrial operations, and emergency response, due to its reliability and effectiveness in providing clean air. The global market for open-circuit SCBA is driven by the increasing demand for safety equipment in hazardous environments, stringent safety regulations, and the growing awareness of occupational safety. As industries continue to prioritize worker safety, the demand for SCBA is expected to remain strong, ensuring that workers are protected in environments where air quality cannot be guaranteed.

Single Oxygen Cylinder, Double Oxygen Cylinder in the Open-circuit Self Contained Breathing Apparatus - Global Market:

The open-circuit self-contained breathing apparatus (SCBA) market includes various configurations, notably single and double oxygen cylinders, each catering to specific needs and applications. Single oxygen cylinder SCBAs are typically lighter and more compact, making them ideal for situations where mobility and ease of use are paramount. These units are often preferred in scenarios where the duration of use is relatively short, such as in certain industrial applications or emergency situations where quick response and agility are crucial. The single-cylinder design allows for a more streamlined apparatus, which can be advantageous in confined spaces or when the user needs to move swiftly. On the other hand, double oxygen cylinder SCBAs are designed for extended use, providing a longer supply of breathable air. This configuration is particularly beneficial in firefighting operations or industrial settings where the user may be exposed to hazardous environments for prolonged periods. The additional cylinder ensures that the user has a sufficient air supply to safely complete their tasks without the need for frequent refills or cylinder changes. While the double-cylinder design adds weight and bulk to the apparatus, the trade-off is often considered worthwhile in situations where safety and endurance are prioritized. The choice between single and double oxygen cylinder SCBAs often depends on the specific requirements of the task at hand, the duration of exposure, and the level of risk involved. In the global market, both configurations are in demand, with manufacturers continually innovating to improve the efficiency, comfort, and safety features of these devices. Advances in materials and technology have led to the development of lighter, more durable cylinders and more ergonomic designs, enhancing the overall user experience. Additionally, the integration of digital monitoring systems in some SCBAs allows users to track air supply levels and other vital information in real-time, further improving safety and operational efficiency. As industries and emergency services continue to evolve, the demand for both single and double oxygen cylinder SCBAs is expected to grow, driven by the need for reliable and effective respiratory protection in diverse and challenging environments. The global market for these devices is characterized by a wide range of products, catering to different needs and preferences, ensuring that users have access to the most suitable equipment for their specific applications.

Fire Fighting, Industrial, Others in the Open-circuit Self Contained Breathing Apparatus - Global Market:

Open-circuit self-contained breathing apparatus (SCBA) plays a crucial role in various sectors, including firefighting, industrial operations, and other specialized fields. In firefighting, SCBAs are indispensable tools that provide firefighters with the necessary respiratory protection to operate in smoke-filled and toxic environments. The ability to breathe clean air allows firefighters to perform their duties effectively, whether it's rescuing individuals, extinguishing fires, or conducting search and rescue operations. The reliability and durability of SCBAs are critical in these high-stakes situations, where the safety of both the firefighters and the people they are rescuing depends on the equipment's performance. In industrial settings, SCBAs are used in environments where airborne contaminants or oxygen deficiency pose a risk to workers' health and safety. Industries such as chemical manufacturing, oil and gas, mining, and construction often require workers to operate in hazardous conditions where the air quality cannot be guaranteed. SCBAs provide the necessary protection, allowing workers to perform their tasks safely and efficiently. The use of SCBAs in these industries is often mandated by safety regulations, underscoring the importance of respiratory protection in maintaining a safe working environment. Beyond firefighting and industrial applications, SCBAs are also used in other areas such as emergency response, military operations, and hazardous material handling. Emergency responders, including paramedics and hazardous materials teams, rely on SCBAs to safely enter and operate in environments where the air is contaminated or oxygen-deficient. In military operations, SCBAs are used in situations where chemical, biological, radiological, or nuclear threats are present, providing soldiers with the necessary protection to carry out their missions. The versatility and effectiveness of SCBAs make them an essential tool in any situation where respiratory protection is required. As the global market for open-circuit SCBAs continues to grow, driven by increasing safety awareness and regulatory requirements, the demand for these devices is expected to remain strong across various sectors. Manufacturers are continually innovating to improve the performance, comfort, and safety features of SCBAs, ensuring that users have access to the most advanced and reliable respiratory protection available.

Open-circuit Self Contained Breathing Apparatus - Global Market Outlook:

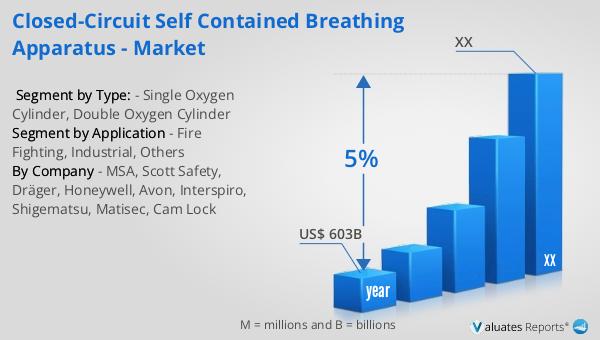

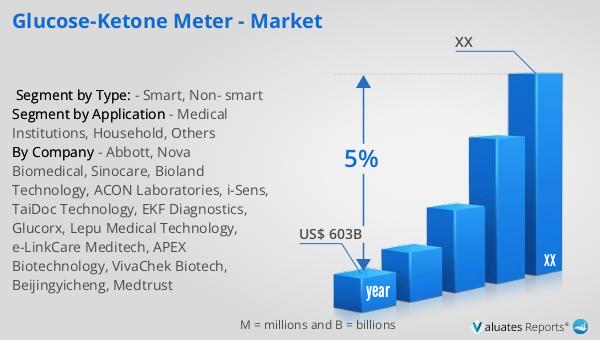

Based on our analysis, the global market for medical devices, which includes open-circuit self-contained breathing apparatus (SCBA), is projected to reach approximately USD 603 billion in 2023. This market is anticipated to expand at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing demand for advanced medical devices, technological advancements, and the rising awareness of health and safety standards across various industries. The open-circuit SCBA market, as a part of this broader medical device sector, is expected to benefit from these trends, as industries and emergency services continue to prioritize respiratory protection in hazardous environments. The growing emphasis on worker safety and the implementation of stringent safety regulations are key drivers of demand for SCBAs, ensuring that workers and emergency responders have access to reliable and effective respiratory protection. As the market continues to evolve, manufacturers are focusing on developing innovative solutions that enhance the performance, comfort, and safety features of SCBAs, catering to the diverse needs of users across different sectors. The integration of digital technologies, such as real-time monitoring systems, is also expected to play a significant role in shaping the future of the SCBA market, providing users with enhanced safety and operational efficiency. Overall, the global market outlook for open-circuit SCBAs is positive, with sustained growth expected as industries and emergency services continue to invest in advanced respiratory protection solutions.

| Report Metric | Details |

| Report Name | Open-circuit Self Contained Breathing Apparatus - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | MSA, Scott Safety, Honeywell, Drager, Interspiro, Cam Lock, Shigematsu, Avon, Matisec, Sinoma, Koken |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |