What is Mesalazine API - Global Market?

Mesalazine, also known as mesalamine, is an active pharmaceutical ingredient (API) primarily used in the treatment of inflammatory bowel diseases such as ulcerative colitis and Crohn's disease. The global market for Mesalazine API is driven by the increasing prevalence of these conditions, which are chronic and require long-term management. Mesalazine works by reducing inflammation in the colon, thereby alleviating symptoms and improving the quality of life for patients. The demand for Mesalazine API is also influenced by advancements in drug formulations and delivery methods, which aim to enhance its efficacy and patient compliance. Additionally, the market is shaped by regulatory approvals and the introduction of generic versions, which make the treatment more accessible and affordable. As healthcare systems worldwide continue to focus on improving patient outcomes and managing chronic diseases, the Mesalazine API market is expected to grow, driven by both established pharmaceutical companies and emerging players seeking to capitalize on this therapeutic area. The market dynamics are further influenced by research and development activities aimed at discovering new applications and improving existing formulations of Mesalazine.

Above 97 %, Above 98 %, Above 99 % in the Mesalazine API - Global Market:

In the Mesalazine API global market, the purity levels of the active ingredient play a crucial role in determining its application and effectiveness. Mesalazine is available in different purity grades, typically categorized as above 97%, above 98%, and above 99%. Each of these purity levels has specific implications for the drug's performance and its suitability for various formulations. The above 97% purity level is often used in standard formulations where the primary goal is to achieve therapeutic efficacy while maintaining cost-effectiveness. This grade is suitable for generic formulations and is widely used in regions where cost constraints are a significant consideration. The above 98% purity level offers a higher degree of refinement, which can enhance the drug's stability and reduce the risk of impurities that might affect patient safety. This grade is often preferred in formulations where a balance between cost and quality is essential, such as in branded generics or in markets with stringent regulatory requirements. The highest purity level, above 99%, is typically reserved for premium formulations where maximum efficacy and safety are paramount. This grade is used in innovative drug delivery systems and in markets where regulatory standards are exceptionally high. The choice of purity level is influenced by several factors, including regulatory guidelines, market demand, and the specific therapeutic needs of the patient population. Pharmaceutical companies must carefully consider these factors when selecting the appropriate purity grade for their Mesalazine API products. The global market for Mesalazine API is thus segmented based on these purity levels, with each segment catering to different market needs and regulatory environments. As the demand for high-quality, effective treatments for inflammatory bowel diseases continues to grow, the importance of purity levels in Mesalazine API is expected to remain a key consideration for manufacturers and healthcare providers alike.

Tablets, Capsules, Granule, Suppository, Enema, Others in the Mesalazine API - Global Market:

Mesalazine API is utilized in various pharmaceutical formulations, each designed to deliver the active ingredient effectively to the site of inflammation in the gastrointestinal tract. Tablets are one of the most common forms, offering convenience and ease of use for patients. They are typically formulated to release Mesalazine in the colon, where it exerts its anti-inflammatory effects. Capsules, similar to tablets, provide a controlled release of the active ingredient, but they may offer advantages in terms of patient compliance, especially for those who have difficulty swallowing tablets. Granules are another formulation, often used for patients who prefer not to take solid dosage forms. They can be mixed with food or liquids, making them a versatile option for different patient preferences. Suppositories are designed for rectal administration, providing direct delivery of Mesalazine to the lower part of the colon. This formulation is particularly useful for patients with distal ulcerative colitis, where the inflammation is localized in the rectum and sigmoid colon. Enemas are liquid formulations administered rectally, offering a similar benefit to suppositories but with the ability to treat a larger area of the colon. They are often used in combination with oral formulations to provide comprehensive treatment for extensive colonic inflammation. Other formulations of Mesalazine API may include topical applications or innovative delivery systems designed to enhance the drug's bioavailability and therapeutic effects. Each of these formulations is developed with the goal of optimizing the delivery of Mesalazine to the site of inflammation, thereby maximizing its therapeutic benefits while minimizing potential side effects. The choice of formulation is influenced by factors such as the severity and location of the disease, patient preferences, and the specific therapeutic goals of the treatment regimen.

Mesalazine API - Global Market Outlook:

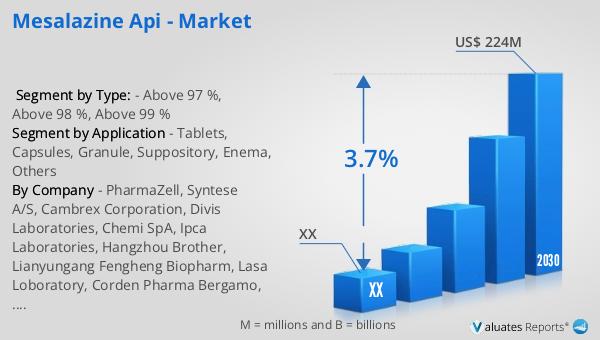

The global market for Mesalazine API was valued at approximately $161.9 million in 2023. It is projected to grow to a revised size of $224 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for effective treatments for inflammatory bowel diseases, driven by rising prevalence rates and advancements in pharmaceutical formulations. In comparison, the broader global pharmaceutical market was valued at $1,475 billion in 2022 and is expected to grow at a CAGR of 5% over the next six years. This growth is fueled by factors such as an aging population, increasing healthcare expenditure, and the continuous development of new therapies. Meanwhile, the chemical drug market, a subset of the pharmaceutical industry, was estimated to grow from $1,005 billion in 2018 to $1,094 billion in 2022. This growth highlights the ongoing demand for chemical-based therapies, including Mesalazine, which remains a critical component of treatment regimens for chronic inflammatory conditions. The Mesalazine API market, while smaller in scale compared to the overall pharmaceutical market, plays a vital role in addressing the specific needs of patients with inflammatory bowel diseases, contributing to the broader goal of improving patient outcomes and quality of life.

| Report Metric | Details |

| Report Name | Mesalazine API - Market |

| Forecasted market size in 2030 | US$ 224 million |

| CAGR | 3.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | PharmaZell, Syntese A/S, Cambrex Corporation, Divis Laboratories, Chemi SpA, Ipca Laboratories, Hangzhou Brother, Lianyungang Fengheng Biopharm, Lasa Loboratory, Corden Pharma Bergamo, Erregierre SpA, CTX Lifescience, Ishita Active Pharma Ingredients, YC Biotech (Jiangsu), Xinxiang Tianfeng Fine Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |