What is Non-absorbable Surgical Sutures - Global Market?

Non-absorbable surgical sutures are a crucial component in the global medical field, particularly in surgical procedures where long-term tissue support is necessary. Unlike absorbable sutures, which dissolve over time, non-absorbable sutures are designed to remain in the body indefinitely unless removed. These sutures are typically made from materials such as polypropylene, nylon, and stainless steel, which are known for their durability and strength. The global market for non-absorbable surgical sutures is driven by the increasing number of surgical procedures worldwide, advancements in suture technology, and the growing demand for minimally invasive surgeries. Additionally, the rising prevalence of chronic diseases and the aging population contribute to the market's expansion, as these factors lead to a higher number of surgeries. The market is also influenced by the continuous development of new suture materials and techniques, which aim to improve patient outcomes and reduce recovery times. As healthcare systems around the world strive to enhance surgical care, the demand for reliable and effective non-absorbable sutures is expected to grow, making this market a vital part of the medical device industry.

Polypropylene, Nylon, Stainless Steel, Other Non-absorbable Sutures in the Non-absorbable Surgical Sutures - Global Market:

Polypropylene, nylon, stainless steel, and other non-absorbable sutures each play a unique role in the global market for non-absorbable surgical sutures, catering to various surgical needs and preferences. Polypropylene sutures are widely used due to their excellent tensile strength and minimal tissue reactivity. They are particularly favored in cardiovascular and plastic surgeries, where precision and durability are paramount. Polypropylene's smooth surface allows for easy passage through tissues, reducing the risk of infection and inflammation. Nylon sutures, on the other hand, are known for their elasticity and strength, making them suitable for skin closure and other applications where flexibility is required. Nylon's ability to maintain tensile strength over time makes it a reliable choice for long-term wound support. Stainless steel sutures are the strongest among non-absorbable options, often used in orthopedic and neurosurgical procedures where maximum strength is necessary. Their resistance to corrosion and high tensile strength make them ideal for securing bones and other hard tissues. However, their rigidity can be a drawback in delicate tissues, limiting their use in certain surgeries. Other non-absorbable sutures, such as silk and polyester, offer unique benefits as well. Silk sutures, though less commonly used today due to their higher tissue reactivity, provide excellent handling characteristics and knot security. Polyester sutures, known for their high tensile strength and minimal tissue drag, are often used in cardiovascular and ophthalmic surgeries. The choice of suture material depends on various factors, including the type of surgery, the patient's condition, and the surgeon's preference. As the global market for non-absorbable surgical sutures continues to evolve, manufacturers are focusing on developing advanced materials and coatings that enhance suture performance and patient outcomes. Innovations such as antimicrobial coatings and bioactive sutures are gaining traction, offering additional benefits such as reduced infection rates and improved healing. The demand for non-absorbable sutures is also influenced by regional healthcare trends and regulatory requirements, which vary across different countries. In developed regions, the emphasis is on high-quality, technologically advanced sutures, while in developing regions, affordability and accessibility are key considerations. As the healthcare landscape continues to change, the global market for non-absorbable surgical sutures is poised for growth, driven by the need for effective and reliable surgical solutions.

Hospitals, Ambulatory Surgical Centers & Clinics in the Non-absorbable Surgical Sutures - Global Market:

Non-absorbable surgical sutures are extensively used in hospitals, ambulatory surgical centers, and clinics, each setting presenting unique demands and opportunities for these essential medical devices. In hospitals, non-absorbable sutures are a staple in operating rooms, used in a wide range of procedures from cardiovascular and orthopedic surgeries to general and plastic surgeries. Hospitals often require a diverse array of suture materials to accommodate the varied surgical needs of their patients. The ability of non-absorbable sutures to provide long-term tissue support makes them indispensable in complex surgeries where tissue healing may take longer. Additionally, hospitals benefit from the availability of advanced suture technologies, such as antimicrobial coatings, which help reduce the risk of postoperative infections. In ambulatory surgical centers, where procedures are typically less complex and patients are discharged on the same day, non-absorbable sutures are valued for their reliability and ease of use. These centers often focus on minimally invasive surgeries, where the precision and strength of non-absorbable sutures are crucial for successful outcomes. The use of these sutures in ambulatory settings is driven by the need for efficient and effective surgical solutions that minimize recovery time and enhance patient satisfaction. Clinics, particularly those specializing in dermatology and cosmetic procedures, also rely on non-absorbable sutures for their ability to provide excellent cosmetic results. In these settings, sutures like nylon and polypropylene are preferred for their smooth passage through tissues and minimal scarring. The choice of suture material in clinics is often influenced by the specific procedure and the desired aesthetic outcome. As the demand for outpatient and minimally invasive procedures continues to rise, the use of non-absorbable sutures in these settings is expected to grow. Overall, the versatility and reliability of non-absorbable surgical sutures make them a vital component in various healthcare settings, supporting a wide range of surgical procedures and contributing to improved patient outcomes.

Non-absorbable Surgical Sutures - Global Market Outlook:

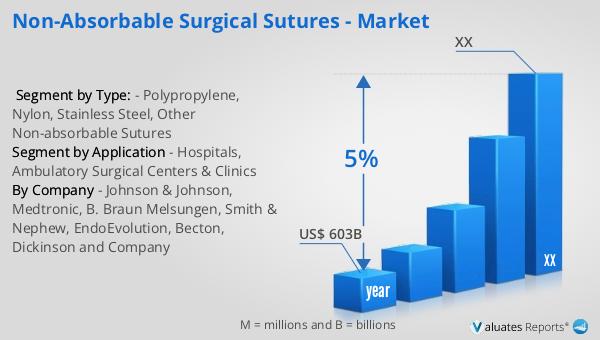

Based on our research, the global market for medical devices, which includes non-absorbable surgical sutures, is projected to reach approximately $603 billion in 2023. This market is anticipated to grow at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing prevalence of chronic diseases, advancements in medical technology, and the rising demand for minimally invasive surgical procedures. As healthcare systems worldwide continue to evolve and improve, the need for reliable and effective medical devices, such as non-absorbable sutures, is expected to increase. The aging population is also a significant factor contributing to the growth of the medical device market, as older individuals often require more surgical interventions. Additionally, the expansion of healthcare infrastructure in developing regions is creating new opportunities for market growth, as access to advanced medical technologies becomes more widespread. As the global market for medical devices continues to expand, manufacturers are focusing on innovation and quality to meet the growing demand for effective surgical solutions. This includes the development of new suture materials and technologies that enhance patient outcomes and reduce recovery times. Overall, the outlook for the non-absorbable surgical sutures market is positive, with steady growth expected in the coming years as healthcare systems worldwide strive to improve surgical care and patient outcomes.

| Report Metric | Details |

| Report Name | Non-absorbable Surgical Sutures - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Johnson & Johnson, Medtronic, B. Braun Melsungen, Smith & Nephew, EndoEvolution, Becton, Dickinson and Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |