What is Intraoral Imaging Systems - Global Market?

Intraoral imaging systems are a crucial component of modern dental care, providing detailed images of the inside of a patient's mouth. These systems are used globally in various dental practices to enhance diagnostic accuracy and treatment planning. The global market for intraoral imaging systems is expanding as dental professionals increasingly adopt advanced technologies to improve patient outcomes. These systems include a range of devices such as intraoral scanners, X-ray systems, sensors, PSP systems, and cameras, each serving a unique purpose in capturing high-quality images of teeth and oral structures. The demand for these systems is driven by the growing awareness of oral health, the increasing prevalence of dental disorders, and the need for precise diagnostic tools. As dental care becomes more sophisticated, the role of intraoral imaging systems in providing comprehensive and efficient dental services continues to grow, making them an indispensable part of the dental industry worldwide. The market's growth is also supported by technological advancements that enhance the functionality and ease of use of these systems, making them more accessible to dental professionals across different regions.

Intraoral Scanners, Intraoral X-ray Systems, Intraoral Sensors, Intraoral PSP Systems, Intraoral Cameras in the Intraoral Imaging Systems - Global Market:

Intraoral scanners are revolutionizing the dental industry by providing a digital alternative to traditional impression methods. These devices capture detailed 3D images of the teeth and gums, allowing for precise measurements and the creation of accurate dental restorations. Intraoral scanners are particularly beneficial in orthodontics and prosthodontics, where precision is paramount. They eliminate the discomfort associated with traditional impression materials and reduce the time required for dental procedures. Intraoral X-ray systems, on the other hand, are essential for diagnosing dental conditions that are not visible to the naked eye. These systems use low doses of radiation to capture images of the teeth, roots, and surrounding bone, aiding in the detection of cavities, bone loss, and other dental issues. Intraoral sensors are a key component of digital X-ray systems, converting X-ray images into digital data that can be easily stored and analyzed. These sensors offer high-resolution images and are more environmentally friendly compared to traditional film-based X-rays. Intraoral PSP (Photostimulable Phosphor) systems are another digital imaging solution that uses reusable plates to capture X-ray images. These plates are scanned to produce digital images, offering a balance between traditional film and digital sensors. Intraoral cameras are small, handheld devices that capture detailed images of the inside of the mouth. They are used for patient education and documentation, allowing dentists to show patients areas of concern and explain treatment options. Each of these intraoral imaging devices plays a vital role in modern dentistry, enhancing diagnostic capabilities and improving patient care. The global market for these systems is driven by the increasing demand for advanced dental technologies and the growing focus on preventive dental care. As dental practices continue to embrace digital solutions, the adoption of intraoral imaging systems is expected to rise, further fueling market growth.

Dental Hospitals & Clinics, Dental Diagnostic Centers, Dental Academic & Research Institutes in the Intraoral Imaging Systems - Global Market:

Intraoral imaging systems are widely used in dental hospitals and clinics to enhance the quality of care provided to patients. These systems enable dentists to obtain detailed images of the oral cavity, facilitating accurate diagnosis and treatment planning. In dental hospitals, intraoral imaging systems are used for a variety of procedures, including routine check-ups, orthodontic assessments, and surgical planning. They help in identifying dental issues at an early stage, allowing for timely intervention and improved patient outcomes. In dental clinics, these systems are used to streamline workflows and improve efficiency. By providing instant access to high-quality images, intraoral imaging systems reduce the need for repeat appointments and enable dentists to make informed decisions quickly. Dental diagnostic centers also rely heavily on intraoral imaging systems to provide comprehensive diagnostic services. These centers use advanced imaging technologies to detect and monitor dental conditions, offering specialized services such as 3D imaging and digital radiography. Intraoral imaging systems play a crucial role in these centers by providing accurate and detailed images that aid in the diagnosis and treatment of complex dental issues. Dental academic and research institutes use intraoral imaging systems for educational and research purposes. These systems are used to train dental students and professionals, providing them with hands-on experience in using advanced imaging technologies. In research settings, intraoral imaging systems are used to study dental diseases and develop new treatment methods. The use of these systems in academic and research institutes helps in advancing dental education and improving the quality of dental care. Overall, intraoral imaging systems are an integral part of the dental industry, supporting various aspects of dental care and contributing to the advancement of dental technology.

Intraoral Imaging Systems - Global Market Outlook:

Our research indicates that the global market for medical devices, including intraoral imaging systems, is projected to reach approximately $603 billion in 2023. This market is expected to experience a steady growth rate, with a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including the increasing demand for advanced medical technologies, the rising prevalence of chronic diseases, and the growing focus on improving healthcare infrastructure. In the dental sector, the adoption of intraoral imaging systems is contributing significantly to this market expansion. These systems are becoming increasingly popular among dental professionals due to their ability to provide accurate and detailed images, enhancing diagnostic capabilities and improving patient care. The growing awareness of oral health and the need for precise diagnostic tools are also driving the demand for intraoral imaging systems. As the global market for medical devices continues to grow, the role of intraoral imaging systems in the dental industry is expected to become even more prominent. This growth presents opportunities for manufacturers and suppliers to innovate and develop new products that meet the evolving needs of dental professionals and patients. Overall, the global market for intraoral imaging systems is poised for significant growth, driven by technological advancements and the increasing demand for high-quality dental care.

| Report Metric | Details |

| Report Name | Intraoral Imaging Systems - Market |

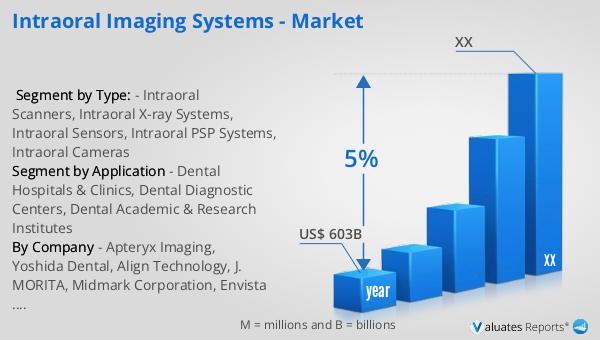

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Apteryx Imaging, Yoshida Dental, Align Technology, J. MORITA, Midmark Corporation, Envista Holdings, PLANMECA OY, ACTEON |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |