What is Global 1, 10-Phenanthroline Anhydrous Market?

The Global 1,10-Phenanthroline Anhydrous Market refers to the worldwide trade and consumption of a specific chemical compound known as 1,10-Phenanthroline in its anhydrous form. This compound is a heterocyclic organic molecule that is widely used in various industries due to its unique chemical properties. It is primarily utilized as a ligand in coordination chemistry, which means it can bind to metal ions to form stable complexes. These complexes are crucial in numerous chemical reactions and processes, making 1,10-Phenanthroline Anhydrous a valuable component in the chemical industry. The market for this compound is driven by its applications in sectors such as pharmaceuticals, where it is used in the synthesis of certain drugs, and in the food and beverage industry, where it serves as a reagent for detecting metal ions. The demand for 1,10-Phenanthroline Anhydrous is influenced by its effectiveness in these applications and the ongoing research and development activities aimed at discovering new uses for this versatile compound. As industries continue to expand and innovate, the market for 1,10-Phenanthroline Anhydrous is expected to grow, reflecting its importance in modern industrial processes.

Below 99%, Above 99% in the Global 1, 10-Phenanthroline Anhydrous Market:

In the Global 1,10-Phenanthroline Anhydrous Market, the purity of the compound is a significant factor that influences its applications and market demand. The market is generally segmented into two categories based on purity levels: below 99% and above 99%. The below 99% purity category typically includes products that are suitable for applications where ultra-high purity is not critical. These might be used in industrial processes where the presence of minor impurities does not significantly affect the outcome or efficiency of the process. For instance, in certain chemical reactions or manufacturing processes, a slightly lower purity level may be acceptable, especially if it results in cost savings. On the other hand, the above 99% purity category is crucial for applications that require high precision and reliability. This level of purity is often necessary in the pharmaceutical industry, where even trace amounts of impurities can affect the safety and efficacy of a drug. Similarly, in the food and beverage industry, high-purity 1,10-Phenanthroline Anhydrous is used to ensure that any metal ion detection is accurate and free from interference by impurities. The demand for high-purity products is also driven by the increasing regulatory standards across industries, which mandate stringent quality controls to ensure consumer safety and product effectiveness. As a result, manufacturers in the Global 1,10-Phenanthroline Anhydrous Market are continually investing in advanced purification technologies to meet these high standards. The choice between below 99% and above 99% purity often depends on the specific requirements of the end-user and the intended application. For example, research laboratories and academic institutions may prefer high-purity products for experimental accuracy, while industrial users might opt for lower purity levels if it aligns with their operational needs and budget constraints. The pricing of 1,10-Phenanthroline Anhydrous also varies with purity, with higher purity products generally commanding a premium due to the additional processing and quality assurance involved. This segmentation based on purity allows suppliers to cater to a diverse range of customers, each with unique needs and expectations. As the market evolves, the balance between these two segments may shift, influenced by technological advancements, changes in industry standards, and emerging applications that demand specific purity levels. Overall, the distinction between below 99% and above 99% purity in the Global 1,10-Phenanthroline Anhydrous Market highlights the importance of quality and precision in chemical manufacturing and underscores the diverse applications of this compound across different sectors.

Chemical Industry, Food and Beverage, Pharmaceutical, Others in the Global 1, 10-Phenanthroline Anhydrous Market:

The Global 1,10-Phenanthroline Anhydrous Market finds its applications across various industries, each leveraging the compound's unique properties to enhance their processes and products. In the chemical industry, 1,10-Phenanthroline Anhydrous is primarily used as a ligand in coordination chemistry. It forms stable complexes with metal ions, which are essential in catalysis and other chemical reactions. These complexes can facilitate the synthesis of new compounds, improve reaction efficiency, and enable the development of innovative materials. The compound's ability to bind with metals also makes it valuable in analytical chemistry, where it is used to detect and quantify metal ions in different samples. This application is crucial for quality control and environmental monitoring, ensuring that products meet safety standards and regulatory requirements. In the food and beverage industry, 1,10-Phenanthroline Anhydrous serves as a reagent for detecting metal ions, particularly iron. Its use in this sector is driven by the need to ensure food safety and quality, as excessive metal ion concentrations can be harmful to consumers. By accurately detecting and measuring these ions, manufacturers can maintain product integrity and comply with health regulations. The pharmaceutical industry also benefits from the properties of 1,10-Phenanthroline Anhydrous. It is used in the synthesis of certain drugs, where its role as a ligand helps in the formation of active pharmaceutical ingredients. The compound's high purity levels are particularly important in this sector, as even minor impurities can affect drug safety and efficacy. Additionally, its use in drug development and research supports the discovery of new therapeutic agents, contributing to advancements in healthcare. Beyond these industries, 1,10-Phenanthroline Anhydrous is utilized in other areas such as environmental science and materials engineering. In environmental applications, it aids in monitoring and controlling pollution by detecting metal contaminants in water and soil. This capability is vital for protecting ecosystems and ensuring public health. In materials engineering, the compound's ability to form metal complexes is exploited to develop new materials with enhanced properties, such as improved conductivity or strength. These diverse applications underscore the versatility and importance of 1,10-Phenanthroline Anhydrous in modern industry. As research continues to uncover new uses for this compound, its role in various sectors is likely to expand, driving further growth in the Global 1,10-Phenanthroline Anhydrous Market.

Global 1, 10-Phenanthroline Anhydrous Market Outlook:

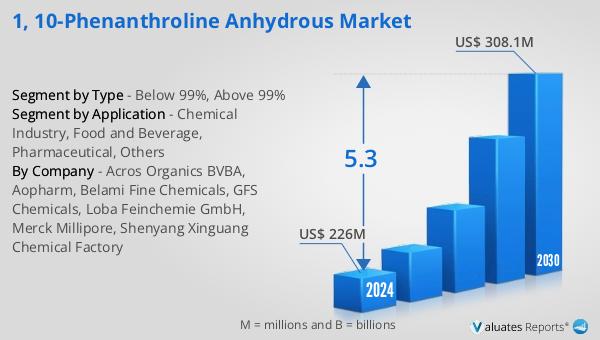

The outlook for the Global 1,10-Phenanthroline Anhydrous Market indicates a promising growth trajectory over the coming years. According to projections, the market is expected to expand from a valuation of approximately $226 million in 2024 to around $308.1 million by 2030. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 5.3% during the forecast period. Such a steady increase in market size reflects the rising demand for 1,10-Phenanthroline Anhydrous across various industries, driven by its versatile applications and the ongoing advancements in chemical research and development. The projected growth can be attributed to several factors, including the increasing need for high-purity chemical compounds in the pharmaceutical and food industries, where stringent quality standards are paramount. Additionally, the compound's role in environmental monitoring and materials engineering is likely to contribute to its expanding market presence. As industries continue to innovate and seek more efficient and effective solutions, the demand for 1,10-Phenanthroline Anhydrous is expected to rise, supporting its market growth. This positive outlook underscores the compound's significance in modern industrial processes and its potential to drive further advancements in various sectors.

| Report Metric | Details |

| Report Name | 1, 10-Phenanthroline Anhydrous Market |

| Accounted market size in 2024 | US$ 226 million |

| Forecasted market size in 2030 | US$ 308.1 million |

| CAGR | 5.3 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Acros Organics BVBA, Aopharm, Belami Fine Chemicals, GFS Chemicals, Loba Feinchemie GmbH, Merck Millipore, Shenyang Xinguang Chemical Factory |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |