What is Identity Governance and Administration - Global Market?

Identity Governance and Administration (IGA) is a crucial component in the realm of cybersecurity and data management, focusing on ensuring that the right individuals have access to the right resources at the right times for the right reasons. This global market is driven by the increasing need for organizations to manage digital identities and access rights efficiently. IGA solutions help businesses streamline identity management processes, enhance security, and comply with regulatory requirements. They provide a framework for managing user identities and access permissions across various systems and applications, reducing the risk of unauthorized access and data breaches. As organizations continue to adopt digital transformation strategies, the demand for robust IGA solutions is expected to grow. These solutions not only help in managing identities but also in auditing and reporting, ensuring that organizations can demonstrate compliance with industry standards and regulations. The global market for IGA is characterized by a diverse range of solutions, including cloud-based and on-premises options, catering to the unique needs of different industries and organizations. As the digital landscape evolves, the importance of effective identity governance and administration will continue to rise, making it a critical area of focus for businesses worldwide.

Cloud-based, On-premises in the Identity Governance and Administration - Global Market:

The Identity Governance and Administration (IGA) market is segmented into cloud-based and on-premises solutions, each offering distinct advantages and challenges. Cloud-based IGA solutions are increasingly popular due to their scalability, flexibility, and cost-effectiveness. They allow organizations to manage identities and access rights without the need for extensive on-site infrastructure, making them ideal for businesses looking to reduce IT overheads. Cloud-based solutions are also easier to update and maintain, ensuring that organizations can quickly adapt to changing security requirements and technological advancements. However, concerns about data privacy and security in the cloud remain a challenge for some organizations, particularly those in highly regulated industries. On the other hand, on-premises IGA solutions offer greater control over data and security, as they are hosted within an organization's own infrastructure. This can be particularly appealing to businesses with stringent data protection requirements or those operating in regions with strict data sovereignty laws. On-premises solutions can be customized to meet specific organizational needs, providing a tailored approach to identity management. However, they often require significant investment in hardware and IT resources, which can be a barrier for smaller organizations. Despite these challenges, both cloud-based and on-premises IGA solutions play a vital role in helping organizations manage digital identities and access rights effectively. As the global market for IGA continues to grow, businesses will need to carefully consider their specific needs and regulatory requirements when choosing between cloud-based and on-premises solutions. The choice between these two options will largely depend on factors such as budget, existing IT infrastructure, and the level of control required over data and security. Ultimately, the goal of any IGA solution is to enhance security, streamline identity management processes, and ensure compliance with industry standards and regulations. As organizations continue to navigate the complexities of the digital landscape, the demand for effective IGA solutions will remain strong, driving innovation and growth in this critical area of cybersecurity.

Manufacturing, Retail, Financial, Government, Others in the Identity Governance and Administration - Global Market:

Identity Governance and Administration (IGA) solutions are utilized across various industries, each with unique requirements and challenges. In the manufacturing sector, IGA solutions help manage the complex web of identities and access rights associated with production systems, supply chain management, and enterprise resource planning (ERP) systems. By ensuring that only authorized personnel have access to critical systems and data, manufacturers can reduce the risk of data breaches and operational disruptions. In the retail industry, IGA solutions play a crucial role in managing customer data and ensuring compliance with data protection regulations. Retailers must balance the need for personalized customer experiences with the requirement to protect sensitive information, making effective identity management essential. In the financial sector, IGA solutions are vital for managing access to sensitive financial data and systems. Financial institutions must comply with stringent regulatory requirements, and IGA solutions provide the tools needed to manage identities, enforce access controls, and demonstrate compliance. Government agencies also rely on IGA solutions to manage access to sensitive information and systems. With the increasing digitization of government services, ensuring that only authorized personnel have access to critical data is essential for maintaining public trust and security. Finally, other industries, such as healthcare and education, also benefit from IGA solutions. In healthcare, managing access to patient data is critical for ensuring privacy and compliance with regulations like HIPAA. In education, IGA solutions help manage access to student records and educational resources, ensuring that only authorized individuals can access sensitive information. Across all these industries, the primary goal of IGA solutions is to enhance security, streamline identity management processes, and ensure compliance with industry standards and regulations. As organizations continue to navigate the complexities of the digital landscape, the demand for effective IGA solutions will remain strong, driving innovation and growth in this critical area of cybersecurity.

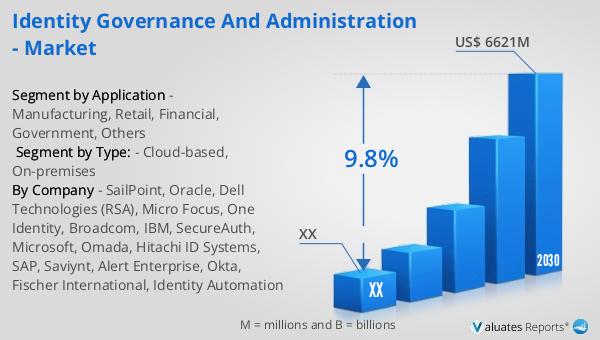

Identity Governance and Administration - Global Market Outlook:

The global market for Identity Governance and Administration was valued at approximately $3,336.3 million in 2023, and it is projected to expand to a revised size of $6,621 million by 2030, reflecting a compound annual growth rate (CAGR) of 9.8% during the forecast period from 2024 to 2030. This growth underscores the increasing importance of IGA solutions in managing digital identities and access rights across various industries. The North American market, a significant contributor to the global IGA landscape, was valued at $ million in 2023 and is expected to reach $ million by 2030, with a CAGR of % during the same forecast period. This growth trajectory highlights the region's strong focus on cybersecurity and compliance, driven by stringent regulatory requirements and the increasing complexity of digital ecosystems. As organizations in North America and around the world continue to prioritize identity governance and administration, the demand for robust IGA solutions is expected to rise. This growth will be fueled by the need to enhance security, streamline identity management processes, and ensure compliance with industry standards and regulations. As the digital landscape evolves, the importance of effective identity governance and administration will continue to rise, making it a critical area of focus for businesses worldwide.

| Report Metric | Details |

| Report Name | Identity Governance and Administration - Market |

| Forecasted market size in 2030 | US$ 6621 million |

| CAGR | 9.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | SailPoint, Oracle, Dell Technologies (RSA), Micro Focus, One Identity, Broadcom, IBM, SecureAuth, Microsoft, Omada, Hitachi ID Systems, SAP, Saviynt, Alert Enterprise, Okta, Fischer International, Identity Automation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |