What is Global Automated Medical Analysis Market?

The Global Automated Medical Analysis Market refers to the industry focused on the development, production, and implementation of automated systems and technologies designed to analyze medical data. These systems are used to streamline and enhance the accuracy of medical diagnostics, treatment planning, and patient monitoring. Automated medical analysis tools include software and hardware solutions that can process large volumes of medical data quickly and accurately, reducing the need for manual intervention and minimizing human error. This market encompasses a wide range of applications, from laboratory automation and imaging analysis to patient data management and predictive analytics. The goal is to improve the efficiency and effectiveness of healthcare delivery, ultimately leading to better patient outcomes and reduced healthcare costs. As healthcare systems worldwide continue to adopt digital technologies, the demand for automated medical analysis solutions is expected to grow, driven by the need for more efficient and accurate diagnostic tools.

On-premises, Cloud-based in the Global Automated Medical Analysis Market:

On-premises and cloud-based solutions are two primary deployment models in the Global Automated Medical Analysis Market. On-premises solutions involve the installation and maintenance of software and hardware within a healthcare facility's own infrastructure. This model offers several advantages, including greater control over data security and system customization. Healthcare providers can tailor the system to meet their specific needs and ensure that sensitive patient data remains within their own network. However, on-premises solutions also come with significant challenges, such as high upfront costs for hardware and software, ongoing maintenance expenses, and the need for specialized IT staff to manage the system. Additionally, scalability can be an issue, as expanding the system to accommodate growing data volumes or additional users may require substantial investments in new hardware and infrastructure. In contrast, cloud-based solutions offer a more flexible and cost-effective alternative. These solutions are hosted on remote servers and accessed via the internet, allowing healthcare providers to use the software without the need for extensive on-site infrastructure. Cloud-based systems typically operate on a subscription model, which can help spread costs over time and reduce the financial burden of large upfront investments. One of the key benefits of cloud-based solutions is their scalability; providers can easily adjust their subscription plans to accommodate changing needs, such as increased data storage or additional user licenses. Furthermore, cloud-based systems often come with automatic updates and maintenance, ensuring that the software remains up-to-date with the latest features and security protocols. Data security is a critical consideration for both deployment models. On-premises solutions offer the advantage of keeping sensitive patient data within the healthcare facility's own network, potentially reducing the risk of data breaches. However, this also means that the facility is responsible for implementing and maintaining robust security measures. Cloud-based solutions, on the other hand, rely on the security protocols of the cloud service provider. Reputable providers invest heavily in advanced security technologies and practices to protect their clients' data, but healthcare providers must still ensure that the chosen provider complies with relevant regulations and standards, such as HIPAA in the United States or GDPR in Europe. Another important factor to consider is system integration. On-premises solutions can be customized to integrate seamlessly with existing systems and workflows within the healthcare facility. This can help streamline operations and improve overall efficiency. However, the customization process can be complex and time-consuming, requiring significant IT expertise. Cloud-based solutions, while generally less customizable, often come with built-in integration capabilities and APIs that facilitate interoperability with other systems. This can simplify the process of connecting different software applications and data sources, enabling a more cohesive and efficient healthcare ecosystem. In summary, both on-premises and cloud-based solutions have their own unique advantages and challenges in the Global Automated Medical Analysis Market. On-premises solutions offer greater control and customization but come with higher costs and maintenance requirements. Cloud-based solutions provide flexibility, scalability, and cost savings but require careful consideration of data security and compliance. Healthcare providers must carefully evaluate their specific needs, resources, and regulatory requirements when choosing the most appropriate deployment model for their automated medical analysis systems.

Hospital, Institute of Biochemistry, Red Cross, Other in the Global Automated Medical Analysis Market:

The Global Automated Medical Analysis Market finds extensive usage across various healthcare settings, including hospitals, institutes of biochemistry, Red Cross organizations, and other medical facilities. In hospitals, automated medical analysis systems play a crucial role in enhancing diagnostic accuracy and efficiency. These systems can process large volumes of patient data quickly, enabling healthcare professionals to make informed decisions faster. For instance, automated imaging analysis tools can help radiologists detect abnormalities in medical images with greater precision, while laboratory automation systems can streamline the processing of blood tests, reducing turnaround times and minimizing human error. By improving the speed and accuracy of diagnostics, automated medical analysis systems contribute to better patient outcomes and more efficient hospital operations. Institutes of biochemistry also benefit significantly from automated medical analysis technologies. These research institutions often handle complex and large-scale biochemical analyses that require high levels of precision and consistency. Automated systems can perform repetitive tasks, such as sample preparation and data analysis, with minimal human intervention, freeing up researchers to focus on more critical aspects of their work. Additionally, automated analysis tools can enhance the reproducibility of experiments by ensuring that procedures are carried out consistently every time. This is particularly important in biochemical research, where even minor variations in experimental conditions can lead to significant differences in results. By leveraging automated medical analysis systems, institutes of biochemistry can improve the efficiency and reliability of their research processes. Red Cross organizations, which provide emergency medical services and disaster relief, also utilize automated medical analysis systems to enhance their operations. In emergency situations, rapid and accurate diagnostics are essential for providing timely and effective care. Automated medical analysis tools can help Red Cross medical teams quickly assess the health status of patients, identify critical conditions, and prioritize treatment. For example, portable automated diagnostic devices can be used in the field to perform blood tests or analyze vital signs, providing immediate insights that guide medical decision-making. By improving the speed and accuracy of diagnostics, automated medical analysis systems enable Red Cross organizations to deliver more effective care in emergency situations. Other medical facilities, such as clinics and outpatient centers, also benefit from the adoption of automated medical analysis technologies. These facilities often operate with limited resources and staff, making efficiency and accuracy critical to their success. Automated systems can help streamline various aspects of patient care, from initial diagnostics to ongoing monitoring and treatment planning. For example, automated patient data management systems can consolidate information from multiple sources, providing healthcare providers with a comprehensive view of a patient's medical history and current condition. This can facilitate more accurate diagnoses and personalized treatment plans. Additionally, automated monitoring tools can track patients' vital signs and other health metrics in real-time, alerting healthcare providers to any significant changes that may require intervention. In conclusion, the Global Automated Medical Analysis Market has a wide range of applications across different healthcare settings, including hospitals, institutes of biochemistry, Red Cross organizations, and other medical facilities. By improving the speed, accuracy, and efficiency of medical diagnostics and data analysis, automated medical analysis systems contribute to better patient outcomes and more effective healthcare delivery. As the adoption of digital technologies continues to grow in the healthcare sector, the demand for automated medical analysis solutions is expected to increase, driving further advancements in this field.

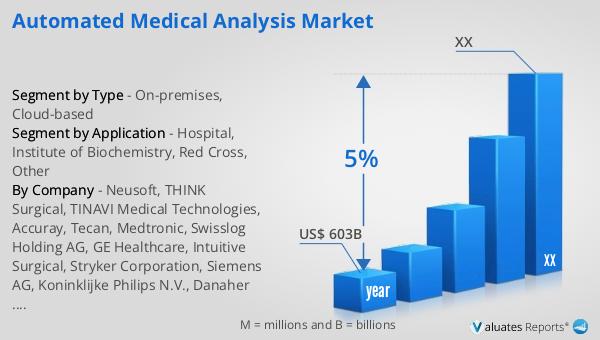

Global Automated Medical Analysis Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately USD 603 billion by the year 2023, with an anticipated compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing demand for healthcare services, and the rising prevalence of chronic diseases. The medical device market encompasses a wide range of products, from diagnostic imaging equipment and surgical instruments to wearable health monitors and implantable devices. As healthcare systems worldwide continue to evolve and adopt new technologies, the demand for innovative and effective medical devices is expected to grow. This growth presents significant opportunities for companies operating in the medical device industry, as they seek to develop and commercialize new products that meet the evolving needs of healthcare providers and patients. Additionally, regulatory changes and increasing emphasis on patient safety and outcomes are likely to drive further innovation and investment in this sector. Overall, the global medical device market is poised for substantial growth in the coming years, offering numerous opportunities for industry stakeholders to capitalize on emerging trends and advancements.

| Report Metric | Details |

| Report Name | Automated Medical Analysis Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Neusoft, THINK Surgical, TINAVI Medical Technologies, Accuray, Tecan, Medtronic, Swisslog Holding AG, GE Healthcare, Intuitive Surgical, Stryker Corporation, Siemens AG, Koninklijke Philips N.V., Danaher Corporation, Zimmer Biomet, techDetector, GRAYLIGHT IMAGING, IBM, ZwickRoell, Bertalan Mesko, AME, Siemens Healthcare |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |