What is Global Industrial Rapid Mixer Granulator (RMG) Market?

The Global Industrial Rapid Mixer Granulator (RMG) Market is a specialized segment within the broader industrial machinery market. Rapid Mixer Granulators are essential equipment used in various industries for the purpose of mixing and granulating materials. These machines are designed to efficiently blend powders and granulate them into uniform particles, which is a critical process in the production of pharmaceuticals, food products, cosmetics, and other industrial goods. The market for RMGs is driven by the increasing demand for high-quality, consistent products and the need for efficient manufacturing processes. The global market encompasses a wide range of RMGs, varying in size, capacity, and technological advancements, catering to the diverse needs of different industries. The growth of this market is also influenced by technological innovations, regulatory requirements, and the expansion of end-use industries across the globe.

Below 100 Liters, 100-500 Liters, 500-1000 Liters, 1000 Liters or More in the Global Industrial Rapid Mixer Granulator (RMG) Market:

In the Global Industrial Rapid Mixer Granulator (RMG) Market, the equipment is categorized based on their capacity, which typically ranges from below 100 liters to 1000 liters or more. RMGs with a capacity below 100 liters are generally used in small-scale production or research and development settings. These smaller units are ideal for laboratories and pilot plants where precise control and flexibility are required. They are often used for testing new formulations and processes before scaling up to larger production volumes. RMGs with a capacity of 100-500 liters are suitable for medium-scale production. These machines strike a balance between capacity and efficiency, making them popular in mid-sized manufacturing facilities. They are capable of handling larger batches than the smaller units, yet they still offer a high degree of control and precision. RMGs with a capacity of 500-1000 liters are designed for large-scale production. These machines are used in industrial settings where high volumes of material need to be processed quickly and efficiently. They are equipped with advanced features to ensure consistent quality and performance, even with large batch sizes. Finally, RMGs with a capacity of 1000 liters or more are used in very large-scale production environments. These machines are capable of processing massive quantities of material, making them ideal for industries with high production demands. They are often used in large pharmaceutical manufacturing plants, food processing facilities, and other industrial settings where efficiency and throughput are critical. Each category of RMGs serves a specific purpose and is designed to meet the unique needs of different production scales, ensuring that manufacturers can choose the right equipment for their specific requirements.

Medicines, Cosmetics, Food, Others in the Global Industrial Rapid Mixer Granulator (RMG) Market:

The usage of Global Industrial Rapid Mixer Granulator (RMG) Market spans across various industries, including medicines, cosmetics, food, and others. In the pharmaceutical industry, RMGs are crucial for the production of tablets and capsules. They ensure that the active pharmaceutical ingredients (APIs) and excipients are thoroughly mixed and granulated to achieve uniformity and consistency in the final product. This process is vital for ensuring the efficacy and safety of medications. In the cosmetics industry, RMGs are used to blend and granulate ingredients for products such as powders, creams, and lotions. The ability to achieve a homogeneous mixture is essential for the quality and performance of cosmetic products. In the food industry, RMGs are employed to mix and granulate ingredients for products like instant soups, sauces, and nutritional supplements. The granulation process helps in improving the texture, solubility, and stability of food products. Additionally, RMGs are used in other industries such as chemicals and agrochemicals, where they play a role in the production of fertilizers, pesticides, and other chemical products. The versatility and efficiency of RMGs make them indispensable in various manufacturing processes, ensuring high-quality and consistent products across different sectors.

Global Industrial Rapid Mixer Granulator (RMG) Market Outlook:

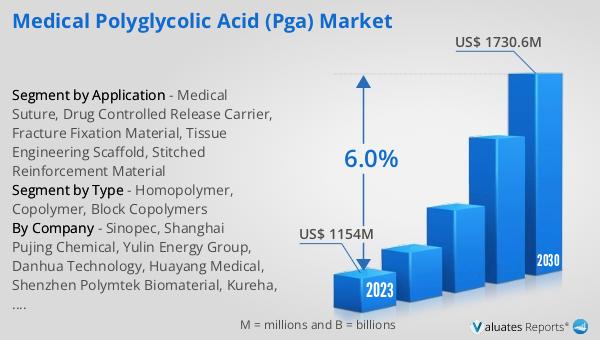

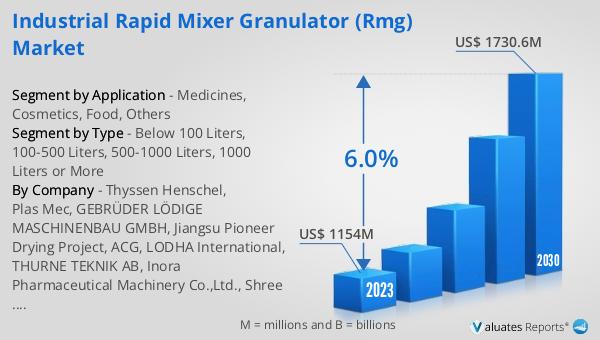

The global Industrial Rapid Mixer Granulator (RMG) market was valued at US$ 1154 million in 2023 and is anticipated to reach US$ 1730.6 million by 2030, witnessing a CAGR of 6.0% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the RMG market over the coming years. The increasing demand for efficient and high-quality manufacturing processes across various industries is a key driver for this growth. As industries continue to expand and innovate, the need for advanced mixing and granulating equipment becomes more critical. The projected growth rate indicates a robust market with opportunities for new entrants and existing players to capitalize on the rising demand. The market's expansion is also likely to be influenced by technological advancements, regulatory changes, and the growing emphasis on product quality and consistency. Overall, the RMG market is poised for substantial growth, driven by the continuous evolution of manufacturing processes and the increasing need for efficient and reliable equipment.

| Report Metric | Details |

| Report Name | Industrial Rapid Mixer Granulator (RMG) Market |

| Accounted market size in 2023 | US$ 1154 million |

| Forecasted market size in 2030 | US$ 1730.6 million |

| CAGR | 6.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Thyssen Henschel, Plas Mec, GEBRÜDER LÖDIGE MASCHINENBAU GMBH, Jiangsu Pioneer Drying Project, ACG, LODHA International, THURNE TEKNIK AB, Inora Pharmaceutical Machinery Co.,Ltd., Shree Bhagwati India, PT Karya Mandiri Machinery, Senieer, FREUND, DIOSNA, GEA Group, Nara Machinery, Werner Pfleider |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |