What is Global Ophthalmic Coater Market?

The Global Ophthalmic Coater Market refers to the industry focused on the production and application of specialized coatings for ophthalmic lenses. These coatings are essential for enhancing the performance and durability of lenses used in eyeglasses, contact lenses, and other optical devices. The market encompasses various types of coatings, including UV protective, scratch-resistant, antifogging, and antireflective coatings. These coatings are applied to lenses to improve their functionality, protect them from damage, and enhance the visual experience for users. The demand for ophthalmic coatings is driven by the increasing prevalence of vision-related issues, the growing awareness of eye health, and advancements in coating technologies. The market serves a wide range of end-users, including glasses factories, optical shops, and other sectors that require high-quality optical coatings. As the global population ages and the need for vision correction rises, the Global Ophthalmic Coater Market is expected to continue its growth trajectory, providing innovative solutions to meet the evolving needs of consumers.

UV Protective Coating, Scratch Resistant Coating, Antifogging Coating, Antireflective Coating in the Global Ophthalmic Coater Market:

UV Protective Coating, Scratch Resistant Coating, Antifogging Coating, and Antireflective Coating are integral components of the Global Ophthalmic Coater Market. UV Protective Coating is designed to shield the eyes from harmful ultraviolet rays, which can cause long-term damage such as cataracts and macular degeneration. This coating is particularly important for individuals who spend a significant amount of time outdoors, as it helps to block both UVA and UVB rays, ensuring comprehensive eye protection. Scratch Resistant Coating, on the other hand, enhances the durability of ophthalmic lenses by creating a hard surface that resists scratches and abrasions. This is crucial for maintaining the clarity and longevity of lenses, especially for those who use their glasses frequently or in environments where lenses are prone to damage. Antifogging Coating addresses the common issue of lenses fogging up due to temperature changes or humidity. This coating is particularly beneficial for individuals who engage in activities that cause rapid temperature shifts, such as moving from a cold environment to a warm one. By preventing fogging, this coating ensures clear vision at all times. Lastly, Antireflective Coating reduces glare and reflections on the surface of lenses, enhancing visual clarity and comfort. This coating is especially useful for activities that require precision and focus, such as driving at night or working on a computer. By minimizing reflections, it allows more light to pass through the lens, improving overall vision quality. Together, these coatings play a vital role in enhancing the functionality and user experience of ophthalmic lenses, making them indispensable in the Global Ophthalmic Coater Market.

Glasses Factory, Optical Shop, Other in the Global Ophthalmic Coater Market:

The Global Ophthalmic Coater Market finds extensive usage in various areas, including glasses factories, optical shops, and other sectors. In glasses factories, ophthalmic coatings are applied during the manufacturing process to ensure that the lenses meet high standards of quality and performance. These factories utilize advanced coating technologies to apply UV protective, scratch-resistant, antifogging, and antireflective coatings to lenses, enhancing their durability and functionality. The application of these coatings in glasses factories is crucial for producing lenses that offer superior protection and visual clarity to consumers. Optical shops, on the other hand, play a significant role in the distribution and customization of ophthalmic lenses. These shops often provide personalized services, such as fitting lenses with specific coatings based on the individual needs of customers. For instance, an optical shop may recommend UV protective coating for a customer who spends a lot of time outdoors or antireflective coating for someone who works extensively on a computer. By offering a range of coating options, optical shops help consumers make informed choices that enhance their visual experience. Additionally, other sectors, such as healthcare facilities and research institutions, also utilize ophthalmic coatings for various applications. In healthcare settings, these coatings are used in the production of medical devices and instruments that require high-quality optical components. Research institutions, on the other hand, may use ophthalmic coatings in the development of new technologies and innovations in the field of vision care. Overall, the Global Ophthalmic Coater Market serves a diverse range of end-users, providing essential coatings that enhance the performance and durability of ophthalmic lenses across different sectors.

Global Ophthalmic Coater Market Outlook:

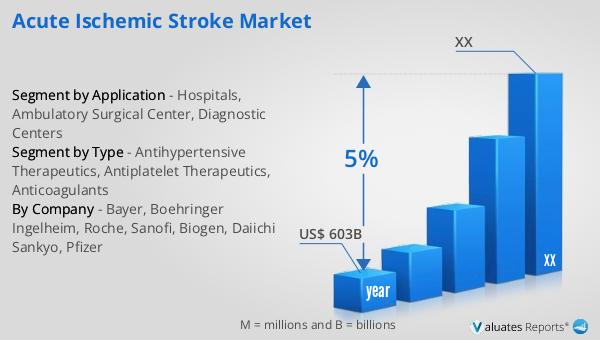

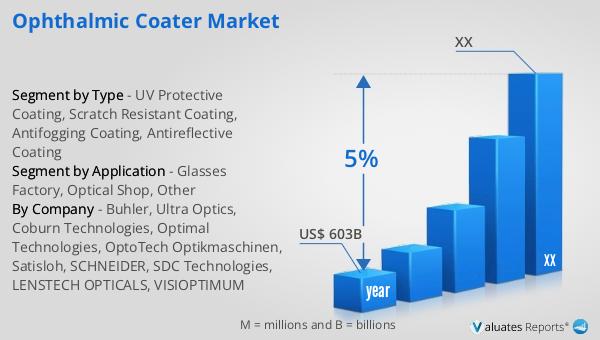

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion by the year 2023, with an anticipated growth rate of 5% CAGR over the next six years. This significant market size underscores the increasing demand for advanced medical technologies and devices across the globe. The steady growth rate reflects the ongoing advancements in medical research, the rising prevalence of chronic diseases, and the growing emphasis on improving healthcare infrastructure. As the medical device industry continues to evolve, it is expected to play a crucial role in enhancing patient care and treatment outcomes. The projected growth also highlights the importance of innovation and investment in the development of new medical devices that can address the diverse needs of patients and healthcare providers. With a focus on improving the quality of life and extending life expectancy, the global medical device market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | Ophthalmic Coater Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Buhler, Ultra Optics, Coburn Technologies, Optimal Technologies, OptoTech Optikmaschinen, Satisloh, SCHNEIDER, SDC Technologies, LENSTECH OPTICALS, VISIOPTIMUM |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |