What is Global L- Cysteine and Its Hydrochloride Market?

The global L-Cysteine and its hydrochloride market is a specialized segment within the broader chemical and pharmaceutical industries. L-Cysteine is a naturally occurring amino acid that is found in various proteins and is essential for the synthesis of proteins in the human body. Its hydrochloride form, L-Cysteine Hydrochloride, is a more stable and soluble version, making it easier to use in various applications. This market encompasses the production, distribution, and utilization of these compounds across different industries. The demand for L-Cysteine and its hydrochloride is driven by their versatile applications, ranging from food and beverages to pharmaceuticals and cosmetics. The market is characterized by a mix of large multinational corporations and smaller specialized firms, all competing to meet the growing demand for these compounds. The global market is projected to grow steadily, driven by increasing awareness of the benefits of L-Cysteine and its hydrochloride, as well as advancements in production technologies that make these compounds more accessible and affordable.

L-Cysteine, L-Cysteine Hydrochloride in the Global L- Cysteine and Its Hydrochloride Market:

L-Cysteine is an amino acid that plays a crucial role in the synthesis of proteins and the production of various biomolecules in the human body. It is a sulfur-containing amino acid, which means it has a sulfur atom in its structure, contributing to its unique properties. L-Cysteine is found in high-protein foods such as poultry, eggs, dairy products, and some plant sources like broccoli and Brussels sprouts. Its hydrochloride form, L-Cysteine Hydrochloride, is created by combining L-Cysteine with hydrochloric acid, resulting in a more stable and water-soluble compound. This makes it easier to incorporate into various products and applications. In the global market, L-Cysteine and its hydrochloride are used in a wide range of industries due to their beneficial properties. For instance, in the food industry, they are used as dough conditioners, flavor enhancers, and preservatives. In the pharmaceutical industry, they are utilized for their antioxidant properties and as a precursor for the synthesis of various drugs. The cosmetics industry uses L-Cysteine and its hydrochloride for their ability to promote healthy skin and hair. Additionally, these compounds are used in animal feed to improve the nutritional quality of feed and promote the health and growth of livestock. The versatility and effectiveness of L-Cysteine and its hydrochloride make them valuable components in many products, driving their demand in the global market.

Food Industrial, Pharmaceutical Industrial, Cosmetics Industrial, Animal Feed, Beverage, Others in the Global L- Cysteine and Its Hydrochloride Market:

The global L-Cysteine and its hydrochloride market finds extensive usage across various industries due to their versatile properties. In the food industry, L-Cysteine and its hydrochloride are commonly used as dough conditioners in bakery products. They help improve the elasticity and extensibility of dough, resulting in better texture and volume of baked goods. Additionally, they act as flavor enhancers and preservatives, extending the shelf life of food products. In the pharmaceutical industry, these compounds are valued for their antioxidant properties, which help protect cells from damage caused by free radicals. They are also used as precursors in the synthesis of various drugs, including those for treating respiratory and liver conditions. The cosmetics industry utilizes L-Cysteine and its hydrochloride for their ability to promote healthy skin and hair. They are often included in formulations for shampoos, conditioners, and skincare products to enhance their effectiveness. In the animal feed industry, these compounds are added to feed to improve its nutritional quality and promote the health and growth of livestock. They help in the synthesis of proteins and other essential biomolecules, contributing to the overall well-being of animals. The beverage industry also benefits from the use of L-Cysteine and its hydrochloride, where they are used as stabilizers and flavor enhancers in various drinks. Other industries, such as biotechnology and agriculture, also utilize these compounds for their beneficial properties. The wide range of applications and the effectiveness of L-Cysteine and its hydrochloride make them valuable components in many products, driving their demand in the global market.

Global L- Cysteine and Its Hydrochloride Market Outlook:

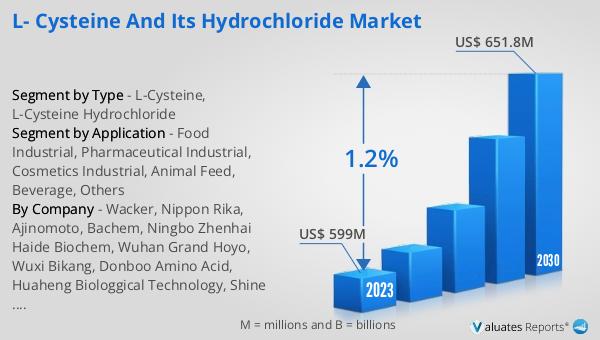

The global L-Cysteine and its hydrochloride market is anticipated to experience growth, with projections indicating an increase from US$ 606.8 million in 2024 to US$ 651.8 million by 2030. This growth represents a Compound Annual Growth Rate (CAGR) of 1.2% during the forecast period. The market is characterized by the presence of several key players, with the top five manufacturers holding a significant share of over 35%. These manufacturers are likely to continue dominating the market due to their established presence, extensive distribution networks, and ongoing investments in research and development. The steady growth of the market can be attributed to the increasing awareness of the benefits of L-Cysteine and its hydrochloride, as well as advancements in production technologies that make these compounds more accessible and affordable. The demand for these compounds is expected to rise across various industries, including food, pharmaceuticals, cosmetics, animal feed, and beverages, driven by their versatile applications and effectiveness. The competitive landscape of the market is likely to remain dynamic, with companies focusing on innovation and strategic partnerships to strengthen their market position. Overall, the global L-Cysteine and its hydrochloride market is poised for steady growth, driven by increasing demand and ongoing advancements in production technologies.

| Report Metric | Details |

| Report Name | L- Cysteine and Its Hydrochloride Market |

| Accounted market size in 2024 | US$ 606.8 million |

| Forecasted market size in 2030 | US$ 651.8 million |

| CAGR | 1.2 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Wacker, Nippon Rika, Ajinomoto, Bachem, Ningbo Zhenhai Haide Biochem, Wuhan Grand Hoyo, Wuxi Bikang, Donboo Amino Acid, Huaheng Biologgical Technology, Shine Star (Hubei) Biological Engineering, Bafeng Pharmaceuticals & Chemicals, Ningbo Haishuo Biotechnology, Premium Ingredient, Longteng Biotechnology, Haitian Amino Acid |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |