What is Global Salad Dressing Market?

The Global Salad Dressing Market encompasses a wide range of products used to enhance the flavor and texture of salads and other dishes. This market includes various types of dressings such as vinaigrettes, creamy dressings, and specialty dressings that cater to diverse consumer preferences across different regions. The market is driven by factors such as increasing health consciousness, the rising popularity of convenience foods, and the growing trend of eating out. Additionally, the expansion of the foodservice industry and the introduction of innovative and exotic flavors have further fueled the demand for salad dressings. The market is highly competitive, with numerous players offering a variety of products to meet the evolving tastes and dietary needs of consumers. As a result, the Global Salad Dressing Market is expected to continue its growth trajectory, driven by the increasing demand for healthy and flavorful food options.

Salad dressing, Ketchup, Mustard, Mayonnaise, BBQ sauce, Cocktail sauce, Soy sauce, Fish sauce, Chili sauce, Worcestershire sauce in the Global Salad Dressing Market:

Salad dressings are a staple in many households and restaurants, offering a quick and easy way to add flavor to salads and other dishes. Ketchup, a popular condiment made from tomatoes, vinegar, sugar, and spices, is widely used not only as a salad dressing but also as a dip and ingredient in various recipes. Mustard, made from mustard seeds, vinegar, and spices, is another versatile condiment that adds a tangy flavor to salads, sandwiches, and marinades. Mayonnaise, a creamy dressing made from oil, egg yolks, and vinegar or lemon juice, is commonly used in salads, sandwiches, and as a base for other dressings and sauces. BBQ sauce, a sweet and tangy sauce made from tomatoes, vinegar, sugar, and spices, is often used as a dressing for salads, a marinade for meats, and a dipping sauce. Cocktail sauce, typically made from ketchup, horseradish, lemon juice, and Worcestershire sauce, is a popular dressing for seafood salads and a dip for shrimp. Soy sauce, a salty and savory sauce made from fermented soybeans, is commonly used as a dressing for Asian-style salads and a seasoning for various dishes. Fish sauce, made from fermented fish, is another staple in Asian cuisine, used as a dressing for salads and a seasoning for soups and stir-fries. Chili sauce, made from chili peppers, vinegar, and spices, adds a spicy kick to salads, marinades, and dips. Worcestershire sauce, a complex sauce made from vinegar, molasses, anchovies, and spices, is often used as a dressing for salads, a marinade for meats, and a seasoning for various dishes. The Global Salad Dressing Market offers a wide range of products to cater to the diverse tastes and preferences of consumers, making it an essential part of the culinary world.

Daily Use, Food Industrial in the Global Salad Dressing Market:

The Global Salad Dressing Market finds its usage in various areas, including daily use and the food industry. In daily use, salad dressings are a convenient and versatile way to add flavor and nutrition to meals. They are commonly used in households to dress salads, marinate meats, and enhance the taste of sandwiches and wraps. The availability of a wide range of flavors and types of dressings allows consumers to experiment with different tastes and create unique dishes. Additionally, the growing trend of healthy eating has led to an increased demand for low-fat, low-calorie, and organic salad dressings, making them a popular choice for health-conscious consumers. In the food industry, salad dressings play a crucial role in enhancing the flavor and appeal of various dishes. Restaurants and foodservice establishments use a variety of dressings to create signature salads, marinades, and sauces that attract customers and differentiate their offerings. The versatility of salad dressings allows chefs to experiment with different flavors and create innovative dishes that cater to the evolving tastes of consumers. Moreover, the convenience of ready-to-use salad dressings saves time and effort in food preparation, making them an essential ingredient in the foodservice industry. The Global Salad Dressing Market continues to grow as consumers seek convenient, flavorful, and healthy options for their meals, both at home and in the food industry.

Global Salad Dressing Market Outlook:

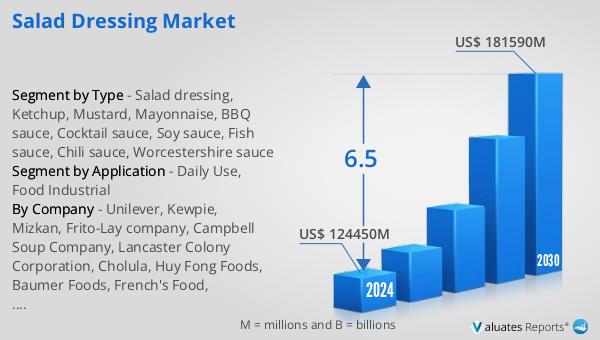

Many cultures have a specific dressing in common usage, such as the blend of yogurt, dill, cucumber, and lemon juice used in the Mediterranean to dress simple salads or the vinaigrette. The global Salad Dressing market is projected to grow from US$ 124,450 million in 2024 to US$ 181,590 million by 2030 at a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period. China is the largest market with a share of about 30%, followed by Europe and North America, both having a share of over 25 percent. In terms of product, Ketchup is the largest segment with a share of nearly 25%.

| Report Metric | Details |

| Report Name | Salad Dressing Market |

| Accounted market size in 2024 | US$ 124450 million |

| Forecasted market size in 2030 | US$ 181590 million |

| CAGR | 6.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Unilever, Kewpie, Mizkan, Frito-Lay company, Campbell Soup Company, Lancaster Colony Corporation, Cholula, Huy Fong Foods, Baumer Foods, French's Food, Southeastern Mills, Remia International |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |