What is Global Medical Headlight Source Market?

The Global Medical Headlight Source Market is a specialized segment within the broader medical devices industry, focusing on the production and distribution of headlight sources used by healthcare professionals. These headlights are essential tools in medical settings, providing focused illumination that enhances visibility during surgical procedures, examinations, and other medical tasks. The market encompasses various types of light sources, including LED, Xenon, and Halogen lamps, each offering unique benefits and applications. The demand for medical headlight sources is driven by the need for precision and clarity in medical procedures, which directly impacts patient outcomes. As healthcare facilities continue to adopt advanced technologies to improve the quality of care, the market for medical headlight sources is expected to grow. This growth is further supported by the increasing number of surgical procedures worldwide, advancements in medical technology, and the rising prevalence of chronic diseases that require surgical intervention. The market is characterized by continuous innovation, with manufacturers striving to develop more efficient, durable, and user-friendly headlight sources to meet the evolving needs of healthcare professionals.

LED, Xenon Lamp, Halogen in the Global Medical Headlight Source Market:

LED, Xenon, and Halogen lamps are the primary types of light sources used in the Global Medical Headlight Source Market, each with distinct characteristics and applications. LED (Light Emitting Diode) headlights are highly favored for their energy efficiency, long lifespan, and superior brightness. They produce a cool, white light that closely mimics natural daylight, reducing eye strain for medical professionals during prolonged procedures. LEDs are also known for their durability and low heat emission, making them a safe and reliable choice for various medical applications. Xenon lamps, on the other hand, are renowned for their intense brightness and high color rendering index (CRI), which provides excellent color accuracy. This feature is particularly beneficial in surgical settings where distinguishing between different tissues and blood vessels is crucial. Xenon lamps produce a bright, white light that enhances visibility and precision, although they tend to generate more heat and consume more power compared to LEDs. Halogen lamps, while less advanced than LEDs and Xenon lamps, are still widely used due to their affordability and availability. They produce a warm, yellowish light and have a shorter lifespan compared to LEDs and Xenon lamps. However, Halogen lamps are known for their consistent light output and are often used in less demanding medical applications. Each type of light source has its advantages and limitations, and the choice of headlight depends on the specific requirements of the medical procedure and the preferences of the healthcare professional. The continuous advancements in lighting technology are driving the development of more efficient and versatile headlight sources, ensuring that medical professionals have access to the best possible tools for their work.

Clinic, Hospital, Others in the Global Medical Headlight Source Market:

The usage of Global Medical Headlight Source Market extends across various healthcare settings, including clinics, hospitals, and other medical facilities. In clinics, medical headlights are primarily used for routine examinations and minor surgical procedures. The focused illumination provided by these headlights enhances the visibility of the examination area, allowing healthcare professionals to perform accurate diagnoses and treatments. Clinics often prefer LED headlights due to their energy efficiency, long lifespan, and minimal heat emission, which ensures patient comfort during examinations. In hospitals, medical headlights are indispensable tools in operating rooms and emergency departments. Surgeons rely on high-quality headlights to perform complex surgical procedures with precision and accuracy. The intense brightness and excellent color rendering of Xenon lamps make them a popular choice in surgical settings, as they provide clear visibility of the surgical site and help distinguish between different tissues and blood vessels. LED headlights are also widely used in hospitals due to their durability, energy efficiency, and ability to produce a cool, white light that reduces eye strain during long procedures. Other medical facilities, such as dental clinics, veterinary clinics, and outpatient surgery centers, also utilize medical headlights to enhance the quality of care provided to patients. In dental clinics, for example, headlights are used to illuminate the oral cavity during dental procedures, ensuring that dentists have a clear view of the treatment area. Veterinary clinics use medical headlights to perform surgeries and examinations on animals, where precise illumination is crucial for accurate diagnosis and treatment. Outpatient surgery centers benefit from the portability and versatility of medical headlights, which can be easily adjusted to suit different procedures and patient needs. Overall, the Global Medical Headlight Source Market plays a vital role in improving the quality of care across various healthcare settings by providing healthcare professionals with the necessary tools to perform their tasks with precision and accuracy.

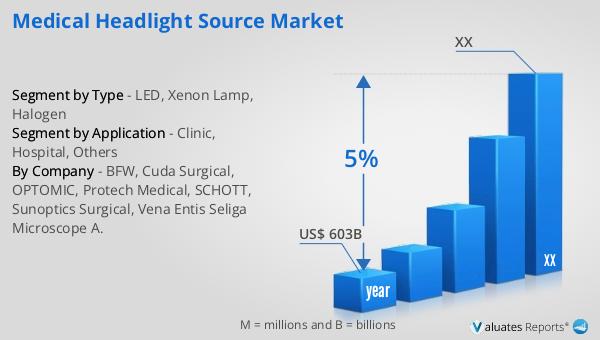

Global Medical Headlight Source Market Outlook:

Based on our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This significant market size underscores the critical role that medical devices play in the healthcare industry, driving advancements in patient care and treatment outcomes. The steady growth rate reflects the increasing demand for innovative medical technologies and devices that enhance the efficiency and effectiveness of healthcare delivery. As the healthcare landscape continues to evolve, the adoption of advanced medical devices, including medical headlight sources, is expected to rise, driven by factors such as the growing prevalence of chronic diseases, an aging population, and the need for minimally invasive surgical procedures. The continuous investment in research and development by medical device manufacturers is also contributing to the market's expansion, leading to the introduction of new and improved products that meet the evolving needs of healthcare professionals and patients. The projected growth of the global medical devices market highlights the importance of ongoing innovation and the development of cutting-edge technologies that can address the challenges faced by the healthcare industry.

| Report Metric | Details |

| Report Name | Medical Headlight Source Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | BFW, Cuda Surgical, OPTOMIC, Protech Medical, SCHOTT, Sunoptics Surgical, Vena Entis Seliga Microscope A. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |