What is Global Hand Held Dermatology Cryosurgery Unit Market?

The Global Hand Held Dermatology Cryosurgery Unit Market refers to the worldwide market for portable devices used in dermatology to perform cryosurgery. Cryosurgery is a medical procedure that involves the application of extreme cold to destroy abnormal or diseased tissue. These handheld units are particularly useful in dermatology for treating various skin conditions such as warts, skin tags, and certain types of skin cancers. The devices are designed to be user-friendly, allowing dermatologists to precisely target and treat affected areas with minimal damage to surrounding healthy tissue. The market for these units is driven by the increasing prevalence of skin disorders, advancements in cryosurgery technology, and the growing demand for minimally invasive procedures. Additionally, the portability of these units makes them highly convenient for use in various healthcare settings, including dermatology clinics, beauty clinics, and hospitals. As awareness about the benefits of cryosurgery continues to grow, the demand for handheld dermatology cryosurgery units is expected to rise, making it a significant segment within the broader medical device market.

Dual Probe, Multi-Probe, Other in the Global Hand Held Dermatology Cryosurgery Unit Market:

In the Global Hand Held Dermatology Cryosurgery Unit Market, devices can be categorized based on their probe configurations, such as Dual Probe, Multi-Probe, and Other types. Dual Probe units are equipped with two probes, allowing for greater versatility and precision in treating different types of skin lesions. These units enable dermatologists to switch between probes depending on the size and type of lesion, thereby enhancing the efficiency and effectiveness of the treatment. Multi-Probe units, on the other hand, come with multiple probes of varying sizes and shapes, offering even more flexibility. This configuration is particularly beneficial for dermatologists who need to treat a wide range of skin conditions, from small warts to larger skin tags and lesions. The ability to quickly change probes without needing to switch devices can save time and improve patient outcomes. Other types of handheld dermatology cryosurgery units may include single-probe devices or those with specialized probes designed for specific applications. These units are often more affordable and easier to use, making them suitable for smaller clinics or practitioners who primarily treat common skin conditions. Regardless of the configuration, the key features of these devices include ease of use, precision, and the ability to deliver consistent and controlled freezing temperatures. The choice of unit often depends on the specific needs of the healthcare provider and the types of conditions they most frequently treat. As technology continues to advance, we can expect to see further innovations in probe design and functionality, enhancing the capabilities of these handheld cryosurgery units.

Dermatology Clinic, Beauty Clinic, Hospital, Other in the Global Hand Held Dermatology Cryosurgery Unit Market:

The usage of Global Hand Held Dermatology Cryosurgery Units spans across various healthcare settings, including Dermatology Clinics, Beauty Clinics, Hospitals, and other specialized medical facilities. In Dermatology Clinics, these units are primarily used for the treatment of skin conditions such as warts, skin tags, and precancerous lesions. The precision and control offered by handheld cryosurgery units make them ideal for dermatologists who need to target specific areas without damaging surrounding healthy tissue. In Beauty Clinics, these devices are often used for cosmetic procedures, such as the removal of benign skin growths and age spots. The minimally invasive nature of cryosurgery makes it a popular choice for clients seeking quick and effective treatments with minimal downtime. Hospitals also utilize handheld dermatology cryosurgery units, particularly in their dermatology departments. These units are valuable tools for treating a wide range of skin conditions, from common warts to more complex cases like basal cell carcinoma. The portability of these devices allows for their use in various hospital settings, including outpatient clinics and surgical units. Other specialized medical facilities, such as pediatric clinics and oncology centers, may also use these units for specific applications. For example, pediatric clinics might use cryosurgery to treat common skin conditions in children, while oncology centers could use it as part of a broader treatment plan for skin cancer patients. Overall, the versatility and effectiveness of handheld dermatology cryosurgery units make them indispensable tools in a variety of healthcare settings, contributing to improved patient outcomes and satisfaction.

Global Hand Held Dermatology Cryosurgery Unit Market Outlook:

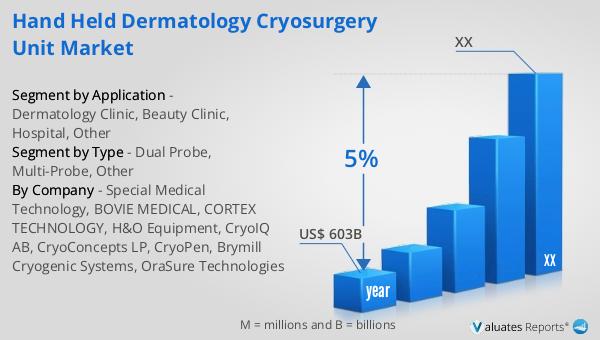

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing healthcare expenditures, and the rising prevalence of chronic diseases. The medical device market encompasses a wide range of products, from diagnostic equipment to therapeutic devices, and the demand for these products is expected to continue growing as healthcare systems worldwide strive to improve patient care and outcomes. The Global Hand Held Dermatology Cryosurgery Unit Market is a significant segment within this broader market, benefiting from the overall growth trends. As more healthcare providers recognize the benefits of minimally invasive procedures and the importance of early detection and treatment of skin conditions, the demand for advanced cryosurgery units is likely to increase. This market outlook highlights the potential for continued innovation and expansion in the medical device industry, offering opportunities for manufacturers, healthcare providers, and patients alike.

| Report Metric | Details |

| Report Name | Hand Held Dermatology Cryosurgery Unit Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Special Medical Technology, BOVIE MEDICAL, CORTEX TECHNOLOGY, H&O Equipment, CryoIQ AB, CryoConcepts LP, CryoPen, Brymill Cryogenic Systems, OraSure Technologies |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |