What is Global Polypropylene Cables Market?

The global polypropylene cables market is a rapidly evolving sector within the broader cable industry. Polypropylene cables are known for their excellent electrical insulation properties, high resistance to chemicals, and durability under extreme conditions. These cables are widely used in various applications, including power transmission, telecommunications, and industrial machinery. The market's growth is driven by the increasing demand for reliable and efficient power and data transmission solutions. Additionally, the rising adoption of renewable energy sources and the expansion of infrastructure projects worldwide are contributing to the market's expansion. The versatility and robustness of polypropylene cables make them a preferred choice in many industries, ensuring their continued relevance and demand in the coming years.

Multi-Mode, Single-Mode in the Global Polypropylene Cables Market:

Polypropylene cables are categorized into two main types based on their mode of operation: multi-mode and single-mode. Multi-mode polypropylene cables are designed to carry multiple light signals simultaneously, each at a different wavelength. This makes them ideal for short-distance communication applications, such as within buildings or on campuses, where high data transfer rates are required over relatively short distances. Multi-mode cables are typically used in local area networks (LANs), data centers, and other environments where high bandwidth and fast data transmission are essential. On the other hand, single-mode polypropylene cables are designed to carry a single light signal over long distances. These cables are used in applications where data needs to be transmitted over vast distances, such as in telecommunications networks, undersea cables, and long-haul data transmission. Single-mode cables offer higher bandwidth and lower signal attenuation compared to multi-mode cables, making them suitable for long-distance communication. The choice between multi-mode and single-mode polypropylene cables depends on the specific requirements of the application, including the distance of data transmission, the required bandwidth, and the overall cost considerations. Both types of cables play a crucial role in ensuring efficient and reliable data transmission in various industries.

Submarine, Power, Oil & Gas, Automobile, Others in the Global Polypropylene Cables Market:

Polypropylene cables are extensively used in several key areas, including submarine, power, oil & gas, automobile, and others. In submarine applications, these cables are essential for undersea communication and power transmission. They are designed to withstand harsh underwater conditions, including high pressure, salinity, and temperature variations. Submarine polypropylene cables are used in undersea telecommunications networks, offshore oil and gas platforms, and renewable energy projects such as offshore wind farms. In the power sector, polypropylene cables are used for transmitting electricity from power plants to substations and from substations to end-users. These cables are known for their high electrical insulation properties, which ensure efficient and safe power transmission. In the oil and gas industry, polypropylene cables are used in various applications, including drilling, exploration, and production. They are designed to withstand harsh environmental conditions, such as extreme temperatures, high pressure, and exposure to chemicals. In the automobile industry, polypropylene cables are used in various electrical and electronic systems, including wiring harnesses, battery cables, and sensor cables. These cables are known for their durability, flexibility, and resistance to chemicals and heat. Other applications of polypropylene cables include industrial machinery, aerospace, and telecommunications. The versatility and robustness of polypropylene cables make them suitable for a wide range of applications, ensuring their continued demand in various industries.

Global Polypropylene Cables Market Outlook:

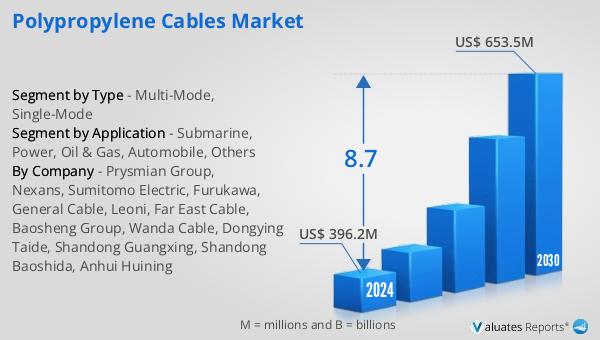

The global polypropylene cables market is expected to grow significantly in the coming years. It is projected to reach a market value of US$ 653.5 million by 2030, up from an estimated US$ 396.2 million in 2024, with a compound annual growth rate (CAGR) of 8.7% during the period from 2024 to 2030. Europe currently holds the largest market share, accounting for approximately 54% of the global market. China follows with about 24% market share. The top three companies in the market occupy around 46% of the total market share. This growth is driven by the increasing demand for reliable and efficient power and data transmission solutions, as well as the rising adoption of renewable energy sources and the expansion of infrastructure projects worldwide. The versatility and robustness of polypropylene cables make them a preferred choice in many industries, ensuring their continued relevance and demand in the coming years.

| Report Metric | Details |

| Report Name | Polypropylene Cables Market |

| Accounted market size in 2024 | an estimated US$ 396.2 million |

| Forecasted market size in 2030 | US$ 653.5 million |

| CAGR | 8.7% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Prysmian Group, Nexans, Sumitomo Electric, Furukawa, General Cable, Leoni, Far East Cable, Baosheng Group, Wanda Cable, Dongying Taide, Shandong Guangxing, Shandong Baoshida, Anhui Huining |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |