What is Global Automotive Interior Coatings Market?

The Global Automotive Interior Coatings Market is a specialized sector focusing on the development, production, and application of coatings used inside vehicles. These coatings are essential for enhancing the aesthetic appeal, durability, and longevity of vehicle interiors. They are applied to various components such as dashboards, door panels, and other interior surfaces to protect them from wear and tear, UV radiation, and heat. The market's significance stems from the growing automotive industry and the increasing demand for vehicles with high-quality and aesthetically pleasing interiors. As consumers become more aware of the importance of a vehicle's interior environment, manufacturers are investing in innovative coating solutions that offer superior performance and environmental benefits. This market is driven by technological advancements, evolving consumer preferences, and stringent environmental regulations that push for the use of safer, more sustainable coating materials. As a result, the Global Automotive Interior Coatings Market is witnessing a surge in demand for products that not only enhance the visual appeal of vehicle interiors but also contribute to the overall safety and comfort of passengers.

Water Based Coating, Solvent Based Coating in the Global Automotive Interior Coatings Market:

In the realm of the Global Automotive Interior Coatings Market, Water Based Coatings and Solvent Based Coatings stand as two pivotal categories, each with its unique properties and applications. Water Based Coatings are celebrated for their environmental friendliness, as they emit lower levels of volatile organic compounds (VOCs) compared to their solvent-based counterparts. This characteristic makes them a preferred choice in regions with strict environmental regulations. They offer excellent adhesion, a low odor profile, and faster drying times, which significantly benefits the manufacturing process. On the other hand, Solvent Based Coatings have traditionally dominated the automotive interior coatings market due to their superior finish and durability. They provide a high-quality appearance, resistance to wear and tear, and longevity, which is crucial for vehicle interiors that undergo constant use and exposure to various elements. However, the environmental impact of solvent emissions has led to increased research and development efforts aimed at reducing VOC levels in these coatings. The choice between water-based and solvent-based coatings often depends on specific application requirements, regulatory compliance, and desired performance characteristics. As the automotive industry continues to evolve, the demand for innovative and sustainable coating solutions grows, driving advancements in both water-based and solvent-based technologies. This ongoing development reflects the market's commitment to meeting the dual objectives of environmental sustainability and superior product performance.

Commercial Car, Passenger Car in the Global Automotive Interior Coatings Market:

The usage of the Global Automotive Interior Coatings Market in Commercial and Passenger Cars is a testament to the diverse requirements and expectations within the automotive sector. In Commercial Cars, the focus is on durability and resistance to wear, as these vehicles are subject to rigorous use. Coatings in this segment are designed to withstand frequent cleaning, exposure to sunlight, and mechanical stress, ensuring that interiors maintain their appearance and functionality over time. The choice of coatings in commercial vehicles often leans towards those with high durability and easy maintenance properties. On the other hand, in Passenger Cars, the emphasis is not only on durability but also on aesthetics and comfort. The interior coatings used in passenger cars are selected to create a visually appealing and comfortable environment for occupants. These coatings are formulated to offer a superior finish, with a focus on color retention, texture, and overall visual appeal. Additionally, they must meet stringent safety and environmental standards, as these aspects are increasingly important to consumers. The application of coatings in passenger cars also considers the potential for customization and personalization, catering to the diverse tastes and preferences of car owners. The Global Automotive Interior Coatings Market plays a crucial role in enhancing the functionality, safety, and aesthetic appeal of both commercial and passenger vehicles, reflecting the varied demands of the automotive industry.

Global Automotive Interior Coatings Market Outlook:

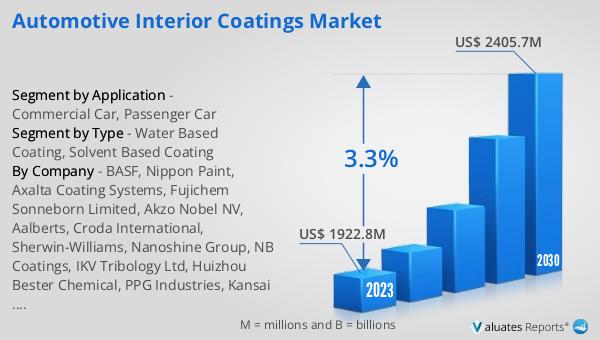

The market outlook for the Global Automotive Interior Coatings Market reveals a promising trajectory, with the market's value estimated at US$ 1922.8 million in 2023. This figure is projected to ascend to US$ 2405.7 million by the year 2030, marking a Compound Annual Growth Rate (CAGR) of 3.3% throughout the forecast period spanning from 2024 to 2030. This growth is indicative of the increasing recognition of the importance of high-quality automotive interior coatings, driven by consumer demand for vehicles that offer not only superior performance but also enhanced aesthetic appeal and comfort. The market's expansion is further fueled by technological innovations and the adoption of environmentally friendly coating solutions, aligning with global trends towards sustainability and reduced environmental impact. As the automotive industry continues to evolve, the demand for automotive interior coatings that meet these criteria is expected to rise, reflecting the market's potential for sustained growth and development in the coming years. This outlook underscores the significance of the Global Automotive Interior Coatings Market as a key component of the automotive sector, with its growth prospects closely tied to broader industry trends and consumer preferences.

| Report Metric | Details |

| Report Name | Automotive Interior Coatings Market |

| Accounted market size in 2023 | US$ 1922.8 million |

| Forecasted market size in 2030 | US$ 2405.7 million |

| CAGR | 3.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | BASF, Nippon Paint, Axalta Coating Systems, Fujichem Sonneborn Limited, Akzo Nobel NV, Aalberts, Croda International, Sherwin-Williams, Nanoshine Group, NB Coatings, IKV Tribology Ltd, Huizhou Bester Chemical, PPG Industries, Kansai Paint, KCC Corporation, Xiangjiang Kansai Paint, YATU, Kinlita, Peter Lacke, Donglai |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |