What is Global Industrial Networking Solutions Market?

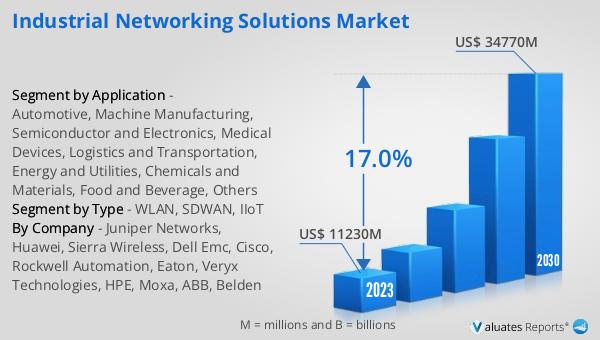

The Global Industrial Networking Solutions Market is a vast and dynamic field that encompasses a range of technologies designed to facilitate efficient communication and data exchange within industrial environments. At its core, this market addresses the growing need for robust, secure, and scalable network infrastructures capable of supporting the complex operations of modern industrial sectors. With a valuation of US$ 11,230 million in 2023, it's clear that businesses worldwide are investing heavily in networking solutions to drive productivity, enhance operational efficiency, and secure their industrial processes against cyber threats. The market's projected growth to US$ 34,770 million by 2030, at a compound annual growth rate (CAGR) of 17.0%, underscores the increasing reliance on these technologies. This surge is driven by the digital transformation of industries, the integration of Internet of Things (IoT) devices, and the need for real-time data analysis in decision-making processes. As industries continue to evolve, the demand for advanced networking solutions that can support the ever-expanding digital landscape is expected to rise, marking a significant shift towards more connected, automated, and intelligent industrial operations.

WLAN, SDWAN, IIoT in the Global Industrial Networking Solutions Market:

Diving into the specifics, the Global Industrial Networking Solutions Market is significantly shaped by technologies such as WLAN (Wireless Local Area Network), SDWAN (Software-Defined Wide Area Network), and IIoT (Industrial Internet of Things). WLAN offers a flexible and efficient means of connecting devices and systems within a localized industrial setting, eliminating the need for cumbersome wired connections and enabling mobility. This technology is crucial for sectors where real-time data access and communication between machines and operators can drastically improve operational efficiency and safety. On the other hand, SDWAN stands out by providing a more agile and cost-effective way to connect and manage networks across multiple locations. It allows businesses to route traffic through the most efficient paths, improving network performance and reliability while ensuring data security across the enterprise. The IIoT, perhaps the most transformative of the three, leverages networked sensors and devices to collect, exchange, and analyze data across various industrial operations. This connectivity not only enhances process efficiencies but also enables predictive maintenance, energy management, and customized production techniques, driving the next wave of industrial innovation. Together, these technologies form the backbone of the Global Industrial Networking Solutions Market, offering a suite of tools that empower industries to navigate the complexities of the digital era.

Automotive, Machine Manufacturing, Semiconductor and Electronics, Medical Devices, Logistics and Transportation, Energy and Utilities, Chemicals and Materials, Food and Beverage, Others in the Global Industrial Networking Solutions Market:

In the realm of the Global Industrial Networking Solutions Market, the application of these technologies spans a diverse range of sectors, including Automotive, Machine Manufacturing, Semiconductor and Electronics, Medical Devices, Logistics and Transportation, Energy and Utilities, Chemicals and Materials, Food and Beverage, among others. In the automotive industry, networking solutions facilitate the seamless integration of production lines and supply chain management, enhancing efficiency and reducing time-to-market for new vehicles. Machine manufacturing benefits from improved machine-to-machine communication, enabling automated production processes and real-time monitoring for maintenance and optimization. The semiconductor and electronics sector relies on precise and reliable data exchange to maintain production quality and efficiency, while medical devices use these solutions to ensure the accuracy and security of critical health data. In logistics and transportation, networking solutions improve tracking, routing, and delivery operations, ensuring goods move efficiently through supply chains. Energy and utilities companies leverage these technologies for smart grid management and to enhance the reliability of energy distribution. The chemical and materials sector utilizes networked sensors for monitoring and controlling chemical processes, ensuring safety and compliance. Food and beverage industries implement these solutions to streamline operations, from production to distribution, ensuring freshness and quality. Across these diverse applications, the Global Industrial Networking Solutions Market plays a pivotal role in enabling industries to achieve higher productivity, efficiency, and innovation in their operations.

Global Industrial Networking Solutions Market Outlook:

The market outlook for the Global Industrial Networking Solutions Market presents a promising future, with its value estimated at US$ 11,230 million in 2023 and expected to soar to US$ 34,770 million by 2030. This remarkable growth trajectory, characterized by a compound annual growth rate (CAGR) of 17.0% during the forecast period from 2024 to 2030, highlights the burgeoning demand for industrial networking solutions across various sectors. This surge is indicative of the critical role that networking technologies play in the modern industrial landscape, where efficiency, security, and scalability are paramount. The substantial investment in these solutions reflects a broader trend towards digital transformation, as businesses seek to leverage the power of connectivity to optimize their operations, enhance productivity, and secure their processes against emerging cyber threats. As the market continues to expand, the integration of advanced networking technologies will undoubtedly become a cornerstone of industrial innovation, driving the future of manufacturing, logistics, energy management, and more, towards a more connected and intelligent era.

| Report Metric | Details |

| Report Name | Industrial Networking Solutions Market |

| Accounted market size in 2023 | US$ 11230 million |

| Forecasted market size in 2030 | US$ 34770 million |

| CAGR | 17.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Juniper Networks, Huawei, Sierra Wireless, Dell Emc, Cisco, Rockwell Automation, Eaton, Veryx Technologies, HPE, Moxa, ABB, Belden |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |