What is Global Aerosol Refrigerants Market?

The Global Aerosol Refrigerants Market is a dynamic sector that plays a crucial role in various cooling systems, from air conditioners to refrigerators, and even in automotive air conditioning units. This market revolves around the production and distribution of aerosol propellants, which are substances used to push the refrigerant out of its container and into the system it's designed to cool. These refrigerants are essential for maintaining the desired temperature in cooling systems, ensuring they operate efficiently and effectively. As of 2023, the market has seen significant value, indicating its importance in the global economy and its role in everyday life. The demand for aerosol refrigerants is driven by several factors, including the increasing need for cooling systems in residential, commercial, and industrial settings, advancements in refrigeration technology, and the growing emphasis on reducing greenhouse gas emissions. The market's expansion is a testament to the ongoing innovation and environmental considerations shaping the industry, making it a key player in the global push towards more sustainable and efficient cooling solutions.

Aluminum Aerosol Refrigerants, Steel Aerosol Refrigerants in the Global Aerosol Refrigerants Market:

Diving into the specifics of the Global Aerosol Refrigerants Market, we find two primary materials at the forefront: Aluminum and Steel Aerosol Refrigerants. These materials are pivotal in the packaging and delivery of refrigerants, each offering unique benefits and challenges. Aluminum, known for its lightweight and corrosion-resistant properties, is a popular choice for aerosol refrigerants. It not only ensures the refrigerant is effectively contained but also contributes to the overall sustainability of the product through recyclability. On the other hand, steel, with its robustness and durability, offers a different set of advantages. It's capable of withstanding higher pressures, making it suitable for certain types of refrigerants that require more stringent containment measures. The choice between aluminum and steel often comes down to the specific needs of the refrigerant type, cost considerations, and environmental impact. Manufacturers in the Global Aerosol Refrigerants Market weigh these factors carefully to decide which material best suits their product's requirements and market demands. This decision-making process is influenced by ongoing research and development in the field, aiming to enhance the efficiency, safety, and environmental friendliness of aerosol refrigerants. As the market continues to evolve, the competition between aluminum and steel aerosol refrigerants remains a key area of focus, driving innovation and improvements in refrigerant packaging and delivery systems.

Household, Industrial, Others in the Global Aerosol Refrigerants Market:

The usage of Global Aerosol Refrigerants spans across various sectors, notably in Household, Industrial, and Other areas, showcasing the versatility and necessity of these products in modern society. In households, aerosol refrigerants are integral to the functioning of air conditioning systems and refrigerators, ensuring a comfortable living environment and the preservation of food, respectively. The demand in this sector is driven by the rising global temperatures and the increasing standards of living, which make efficient and reliable cooling systems essential for everyday life. In the industrial realm, aerosol refrigerants are crucial for processes requiring temperature control, including food processing, chemical manufacturing, and data center operations, among others. The precise temperature regulation provided by these refrigerants helps in maintaining the quality of products, ensuring safety, and enhancing operational efficiency. The "Others" category encompasses a wide range of applications, including automotive air conditioning, where aerosol refrigerants play a vital role in passenger comfort and vehicle performance. The broad applicability of aerosol refrigerants across these sectors highlights their importance in maintaining not only the quality of life but also the continuity and efficiency of various industrial processes. As the market grows, the innovation in aerosol refrigerant applications continues to expand, further solidifying their role in a wide array of cooling needs.

Global Aerosol Refrigerants Market Outlook:

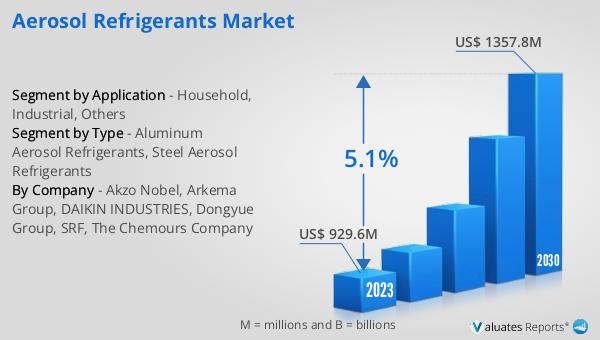

The market outlook for Global Aerosol Refrigerants presents a promising future, with the sector's value estimated at US$ 929.6 million in 2023, and projections suggest it will ascend to US$ 1357.8 million by 2030. This growth trajectory, marked by a Compound Annual Growth Rate (CAGR) of 5.1% during the forecast period from 2024 to 2030, underscores the increasing demand and potential for innovation within the market. Such expansion is indicative of the sector's resilience and its capacity to adapt to changing environmental standards, technological advancements, and consumer needs. The anticipated growth reflects the ongoing efforts to develop more sustainable and efficient refrigerant solutions, catering to a global clientele seeking to mitigate environmental impact while enhancing cooling system performance. This outlook not only highlights the economic significance of the aerosol refrigerants market but also its role in fostering a more sustainable future through the adoption of greener technologies and practices. As the market progresses, it is expected to offer new opportunities for businesses, innovators, and consumers alike, contributing to the global effort to address climate change and energy efficiency.

| Report Metric | Details |

| Report Name | Aerosol Refrigerants Market |

| Accounted market size in 2023 | US$ 929.6 million |

| Forecasted market size in 2030 | US$ 1357.8 million |

| CAGR | 5.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Akzo Nobel, Arkema Group, DAIKIN INDUSTRIES, Dongyue Group, SRF, The Chemours Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |