What is Global Ceiling Axial Fan Market?

The Global Ceiling Axial Fan Market is a segment of the broader ventilation and air movement industry, focusing specifically on fans designed to be mounted on ceilings. These fans are engineered to move air efficiently across large spaces, making them ideal for various applications, from industrial to residential settings. Ceiling axial fans are characterized by their axial flow design, where air moves parallel to the fan's axis, allowing for high airflow rates with relatively low power consumption. This market is driven by the increasing demand for energy-efficient ventilation solutions, as well as the need for improved air quality in both commercial and residential buildings. Technological advancements have led to the development of more efficient and quieter models, further boosting their adoption. The market is also influenced by regulatory standards aimed at reducing energy consumption and improving indoor air quality. As urbanization and industrialization continue to rise globally, the demand for effective ventilation solutions like ceiling axial fans is expected to grow, making this market a vital component of the global HVAC (heating, ventilation, and air conditioning) industry.

AC Axial Fans, DC Axial Fans in the Global Ceiling Axial Fan Market:

AC axial fans and DC axial fans are two primary types of fans within the Global Ceiling Axial Fan Market, each with distinct characteristics and applications. AC axial fans operate on alternating current (AC) and are known for their robust performance and durability. They are typically used in environments where a consistent and reliable airflow is necessary, such as in industrial settings or large commercial spaces. AC fans are favored for their ability to handle high power loads and their compatibility with standard electrical systems, making them a practical choice for many applications. However, they tend to consume more energy compared to their DC counterparts, which can be a consideration in energy-conscious environments. On the other hand, DC axial fans operate on direct current (DC) and are celebrated for their energy efficiency and quieter operation. These fans are often used in applications where noise levels and energy consumption are critical factors, such as in residential settings or in commercial spaces where a quieter environment is desired. DC fans are also known for their ability to offer variable speed control, allowing for more precise airflow management. This feature makes them particularly appealing in applications where airflow needs may vary throughout the day or in response to changing environmental conditions. The choice between AC and DC axial fans often depends on the specific requirements of the application, including factors such as energy efficiency, noise levels, and the need for variable speed control. In the Global Ceiling Axial Fan Market, both AC and DC fans play crucial roles, catering to a wide range of needs and preferences. As technology continues to advance, the line between AC and DC fans may blur, with innovations leading to more hybrid models that combine the best features of both types. This evolution is likely to further expand the market and offer consumers even more options to meet their ventilation needs.

Industrial, Commercial, Other Applications in the Global Ceiling Axial Fan Market:

The Global Ceiling Axial Fan Market finds extensive usage across various sectors, including industrial, commercial, and other applications, each with unique requirements and challenges. In industrial settings, ceiling axial fans are crucial for maintaining optimal air circulation, which is essential for worker safety and equipment efficiency. These fans help in controlling temperature, reducing humidity, and dispersing fumes or dust, thereby creating a safer and more comfortable working environment. Industries such as manufacturing, warehousing, and food processing rely heavily on these fans to ensure compliance with health and safety regulations while also enhancing productivity. In commercial spaces, ceiling axial fans are used to improve air quality and comfort for occupants. Retail stores, office buildings, and hospitality venues utilize these fans to maintain a pleasant indoor climate, which can significantly impact customer satisfaction and employee performance. The ability of ceiling axial fans to provide consistent airflow without consuming excessive energy makes them an attractive option for businesses looking to reduce operational costs while maintaining a high standard of indoor air quality. Beyond industrial and commercial applications, ceiling axial fans are also used in other areas such as residential buildings, educational institutions, and healthcare facilities. In residential settings, these fans offer an energy-efficient solution for cooling and ventilation, contributing to lower utility bills and a reduced carbon footprint. In schools and hospitals, maintaining good air quality is paramount, and ceiling axial fans play a vital role in ensuring a healthy environment for students and patients. The versatility and efficiency of ceiling axial fans make them a valuable asset in a wide range of applications, driving their demand across different sectors. As awareness of the importance of indoor air quality continues to grow, the Global Ceiling Axial Fan Market is poised to expand, offering innovative solutions to meet the evolving needs of various industries.

Global Ceiling Axial Fan Market Outlook:

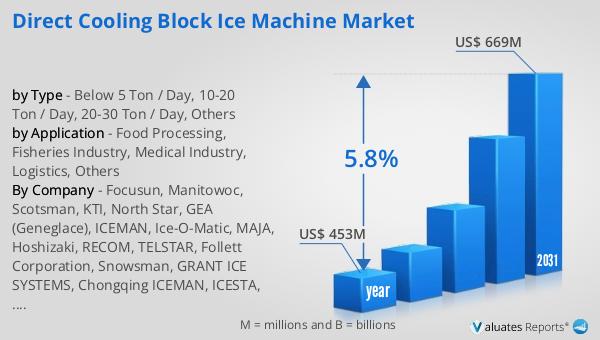

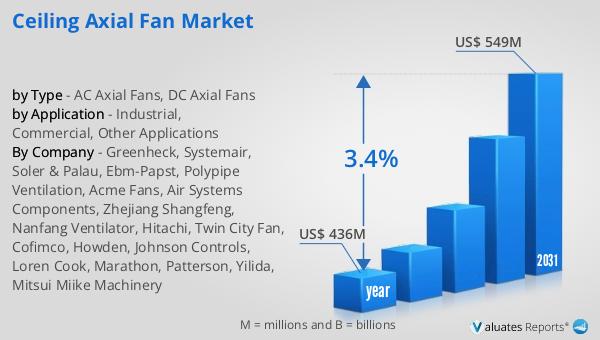

The global market for ceiling axial fans was valued at approximately $436 million in 2024, and it is anticipated to grow to a revised size of $549 million by 2031. This growth represents a compound annual growth rate (CAGR) of 3.4% over the forecast period. This steady increase in market size reflects the rising demand for efficient and effective ventilation solutions across various sectors. The growth is driven by several factors, including the increasing focus on energy efficiency, the need for improved indoor air quality, and the expansion of industrial and commercial infrastructure worldwide. As more businesses and consumers become aware of the benefits of ceiling axial fans, such as their ability to provide consistent airflow and reduce energy consumption, the market is expected to continue its upward trajectory. Additionally, advancements in technology are leading to the development of more efficient and quieter models, further boosting their adoption. The market's growth is also supported by regulatory standards aimed at reducing energy consumption and improving indoor air quality, which are encouraging the adoption of energy-efficient ventilation solutions like ceiling axial fans. As the market continues to evolve, it is likely to offer new opportunities for innovation and expansion, making it an exciting area for investment and development.

| Report Metric | Details |

| Report Name | Ceiling Axial Fan Market |

| Accounted market size in year | US$ 436 million |

| Forecasted market size in 2031 | US$ 549 million |

| CAGR | 3.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Greenheck, Systemair, Soler & Palau, Ebm-Papst, Polypipe Ventilation, Acme Fans, Air Systems Components, Zhejiang Shangfeng, Nanfang Ventilator, Hitachi, Twin City Fan, Cofimco, Howden, Johnson Controls, Loren Cook, Marathon, Patterson, Yilida, Mitsui Miike Machinery |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |