What is Global Industrial RJ45 Ethernet Connectors Market?

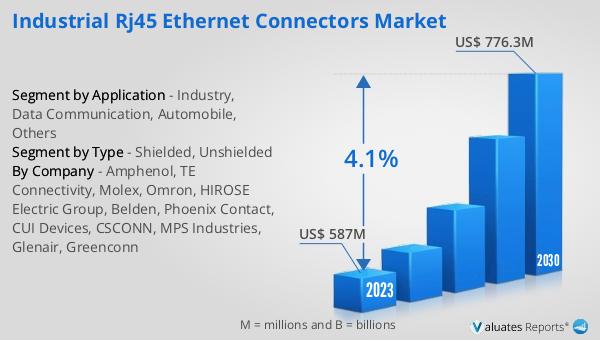

The global Industrial RJ45 Ethernet Connectors market was valued at US$ 587 million in 2023 and is anticipated to reach US$ 776.3 million by 2030, witnessing a CAGR of 4.1% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory for these connectors, which are essential components in various industrial applications. RJ45 Ethernet connectors are widely used for establishing reliable and high-speed network connections in industrial environments. They are designed to withstand harsh conditions, including extreme temperatures, vibrations, and electromagnetic interference, making them suitable for use in factories, data centers, and other industrial settings. The increasing demand for automation and the growing adoption of Industrial Internet of Things (IIoT) technologies are driving the need for robust and reliable network connectivity solutions, further propelling the market growth. Additionally, the rising trend of smart manufacturing and the need for seamless communication between machines and systems are contributing to the increasing demand for industrial RJ45 Ethernet connectors. As industries continue to embrace digital transformation and connectivity, the market for these connectors is expected to expand, offering significant opportunities for manufacturers and suppliers in the coming years.

Shielded, Unshielded in the Global Industrial RJ45 Ethernet Connectors Market:

The global Industrial RJ45 Ethernet Connectors market encompasses a wide range of products, including shielded and unshielded connectors. Shielded RJ45 connectors are designed to provide additional protection against electromagnetic interference (EMI) and radio frequency interference (RFI), which can disrupt data transmission and affect network performance. These connectors are typically used in environments with high levels of electrical noise, such as industrial automation systems, data centers, and telecommunications networks. The shielding helps to maintain signal integrity and ensures reliable data transmission, even in challenging conditions. On the other hand, unshielded RJ45 connectors are more commonly used in less demanding environments where EMI and RFI are not significant concerns. These connectors are often used in office networks, residential applications, and other settings where the risk of interference is minimal. Unshielded connectors are generally more cost-effective and easier to install compared to their shielded counterparts. However, they may not provide the same level of protection and performance in environments with high levels of electrical noise. The choice between shielded and unshielded RJ45 connectors depends on the specific requirements of the application and the level of protection needed. In industrial settings, where reliability and performance are critical, shielded connectors are often preferred to ensure uninterrupted data transmission and network stability. As the demand for high-speed and reliable network connectivity continues to grow, manufacturers are focusing on developing advanced RJ45 connectors with enhanced shielding capabilities and improved performance characteristics. This includes the use of advanced materials and innovative design techniques to minimize signal loss and interference. Additionally, the increasing adoption of PoE (Power over Ethernet) technology is driving the demand for RJ45 connectors that can support both data and power transmission. PoE-enabled RJ45 connectors are designed to deliver power to connected devices, such as IP cameras, wireless access points, and VoIP phones, while simultaneously transmitting data. This eliminates the need for separate power cables and simplifies network installation and maintenance. The growing trend of smart manufacturing and the Industrial Internet of Things (IIoT) is also contributing to the demand for advanced RJ45 connectors. These technologies require reliable and high-speed network connectivity to enable seamless communication between machines, sensors, and control systems. As a result, there is a growing need for RJ45 connectors that can support the high data rates and low latency required for real-time data exchange and control. In conclusion, the global Industrial RJ45 Ethernet Connectors market is characterized by a diverse range of products, including shielded and unshielded connectors, each with its own set of advantages and applications. The choice between these connectors depends on the specific requirements of the application and the level of protection needed against electromagnetic interference. As industries continue to embrace digital transformation and connectivity, the demand for advanced RJ45 connectors with enhanced performance characteristics is expected to grow, offering significant opportunities for manufacturers and suppliers in the coming years.

Industry, Data Communication, Automobile, Others in the Global Industrial RJ45 Ethernet Connectors Market:

The usage of global Industrial RJ45 Ethernet Connectors spans across various sectors, including industry, data communication, automobile, and others. In the industrial sector, these connectors are crucial for establishing reliable and high-speed network connections in automation systems, control panels, and machinery. They enable seamless communication between different components of the industrial network, ensuring efficient operation and real-time data exchange. The robust design of industrial RJ45 connectors allows them to withstand harsh environmental conditions, such as extreme temperatures, vibrations, and electromagnetic interference, making them ideal for use in factories and manufacturing plants. In the data communication sector, RJ45 Ethernet connectors are widely used in data centers, telecommunications networks, and office environments. They facilitate high-speed data transmission and ensure reliable network connectivity, which is essential for the smooth operation of data-intensive applications and services. The increasing demand for cloud computing, big data analytics, and high-speed internet services is driving the need for advanced RJ45 connectors that can support higher data rates and provide enhanced performance. In the automobile sector, RJ45 Ethernet connectors are used in various applications, including in-vehicle networking, infotainment systems, and advanced driver-assistance systems (ADAS). These connectors enable reliable communication between different electronic control units (ECUs) and sensors within the vehicle, ensuring the efficient operation of various systems and enhancing the overall driving experience. The growing trend of connected and autonomous vehicles is further driving the demand for high-speed and reliable network connectivity solutions, including RJ45 Ethernet connectors. In addition to these sectors, RJ45 Ethernet connectors are also used in various other applications, such as security and surveillance systems, healthcare equipment, and smart home devices. In security and surveillance systems, these connectors enable reliable data transmission between IP cameras, network video recorders (NVRs), and monitoring stations, ensuring real-time video streaming and recording. In healthcare equipment, RJ45 connectors are used to establish network connections between medical devices, such as patient monitors, imaging systems, and electronic health record (EHR) systems, facilitating efficient data exchange and improving patient care. In smart home devices, RJ45 connectors enable seamless communication between different connected devices, such as smart thermostats, lighting systems, and home automation hubs, enhancing the overall functionality and convenience of the smart home ecosystem. Overall, the usage of global Industrial RJ45 Ethernet Connectors is diverse and spans across various sectors, each with its own set of requirements and applications. The increasing demand for reliable and high-speed network connectivity, driven by trends such as automation, digital transformation, and the Internet of Things (IoT), is propelling the growth of the RJ45 Ethernet connectors market. As industries continue to adopt advanced technologies and connectivity solutions, the demand for robust and high-performance RJ45 connectors is expected to rise, offering significant opportunities for manufacturers and suppliers in the coming years.

Global Industrial RJ45 Ethernet Connectors Market Outlook:

English: #IndustrialRJ45 #EthernetConnectors #MarketGrowth #Automation #DataCommunication #AutomobileNetworking #SmartManufacturing #IIoT #PoE #NetworkConnectivity

| Report Metric | Details |

| Report Name | Industrial RJ45 Ethernet Connectors Market |

| Accounted market size in 2023 | US$ 587 million |

| Forecasted market size in 2030 | US$ 776.3 million |

| CAGR | 4.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Amphenol, TE Connectivity, Molex, Omron, HIROSE Electric Group, Belden, Phoenix Contact, CUI Devices, CSCONN, MPS Industries, Glenair, Greenconn |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |