What is Global Rugged Tablet Computers Market?

The Global Rugged Tablet Computers Market refers to the industry focused on the production and distribution of tablets designed to withstand harsh environments and demanding conditions. Unlike regular tablets, rugged tablets are built with durable materials and reinforced components, making them resistant to water, dust, shock, and extreme temperatures. These tablets are essential for industries where standard devices would fail due to environmental challenges. The market for rugged tablets is driven by the need for reliable technology in sectors such as military, construction, and public safety, where durability and performance are critical. As technology advances, these tablets are becoming more sophisticated, offering features like enhanced connectivity, longer battery life, and advanced data security. The global demand for rugged tablets is increasing as more industries recognize their value in improving operational efficiency and reducing downtime. With ongoing innovations and a growing emphasis on mobility and remote work, the Global Rugged Tablet Computers Market is poised for continued growth, catering to a wide range of professional applications.

Fully-Rugged Tablet Computers, Semi-Rugged Tablet Computers, Ultra-Rugged Tablet Computers in the Global Rugged Tablet Computers Market:

Fully-Rugged Tablet Computers are designed to endure the most extreme conditions, making them ideal for industries that operate in harsh environments. These tablets are built with robust materials, such as magnesium alloy and hardened glass, to withstand drops, vibrations, and exposure to water and dust. They often meet military standards for durability and are equipped with features like sunlight-readable displays and extended battery life, ensuring they function reliably in challenging settings. Fully-rugged tablets are commonly used in military operations, field services, and outdoor construction sites where reliability is paramount. Semi-Rugged Tablet Computers, on the other hand, offer a balance between durability and cost. While not as robust as fully-rugged models, they are still designed to handle moderate environmental challenges. These tablets are often used in industries like manufacturing and transportation, where devices may be exposed to dust, moisture, and occasional drops. Semi-rugged tablets provide a cost-effective solution for businesses that require durable technology without the need for extreme protection. Ultra-Rugged Tablet Computers represent the pinnacle of durability, designed for the most demanding applications. These tablets are built to survive in environments where even fully-rugged devices might struggle. They are often used in industries like mining, oil and gas, and emergency services, where exposure to extreme temperatures, heavy vibrations, and hazardous materials is common. Ultra-rugged tablets are equipped with advanced features such as thermal imaging, biometric security, and specialized connectivity options to meet the unique needs of these industries. The Global Rugged Tablet Computers Market offers a range of options to cater to different levels of durability requirements, ensuring that businesses can find the right solution for their specific needs. As technology continues to evolve, the capabilities of rugged tablets are expanding, providing even more value to industries that rely on them for critical operations.

Energy, Manufacturing, Construction, Transportation & Distribution, Public Safety, Retail, Medical, Government, Military in the Global Rugged Tablet Computers Market:

The usage of Global Rugged Tablet Computers Market spans across various industries, each benefiting from the durability and reliability these devices offer. In the energy sector, rugged tablets are used for monitoring and managing operations in remote and harsh environments, such as oil rigs and wind farms. Their ability to withstand extreme temperatures and rough handling makes them indispensable for field technicians and engineers. In manufacturing, rugged tablets streamline processes by providing real-time data access and communication on the factory floor. They help improve efficiency and reduce downtime by enabling workers to quickly identify and address issues. In the construction industry, rugged tablets are used for project management, site inspections, and communication between teams. Their durability ensures they can withstand the dust, dirt, and rough handling common on construction sites. In transportation and distribution, rugged tablets are used for fleet management, route optimization, and inventory tracking. They provide drivers and logistics personnel with reliable access to critical information, even in challenging conditions. Public safety professionals, such as police officers and firefighters, rely on rugged tablets for communication, navigation, and accessing vital information during emergencies. In the retail sector, rugged tablets are used for inventory management, point-of-sale transactions, and customer service, providing a durable solution for high-traffic environments. In the medical field, rugged tablets are used for patient monitoring, data collection, and communication between healthcare professionals. Their durability ensures they can withstand the rigors of a busy hospital environment. Government and military applications of rugged tablets include communication, data collection, and mission planning, where reliability and security are crucial. The versatility and durability of rugged tablets make them an essential tool across these industries, enhancing productivity and ensuring operations run smoothly.

Global Rugged Tablet Computers Market Outlook:

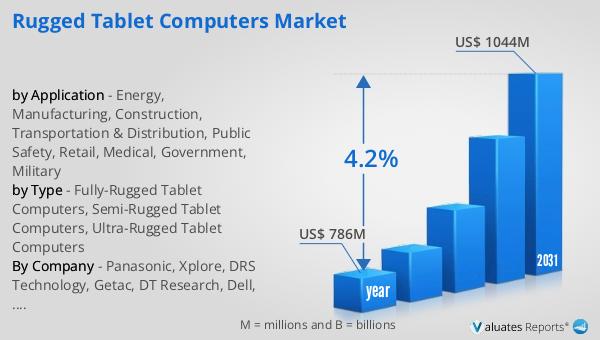

The global market for Rugged Tablet Computers was valued at $786 million in 2024 and is expected to grow to $1,044 million by 2031, with a compound annual growth rate (CAGR) of 4.2% during the forecast period. This growth reflects the increasing demand for durable and reliable technology solutions across various industries. As businesses and organizations continue to recognize the value of rugged tablets in improving operational efficiency and reducing downtime, the market is poised for expansion. The projected growth also indicates a trend towards greater adoption of rugged tablets in sectors that require robust technology to withstand challenging environments. With advancements in technology and a growing emphasis on mobility and remote work, the market for rugged tablets is expected to continue its upward trajectory. The increasing need for reliable communication, data access, and operational efficiency in industries such as military, construction, and public safety is driving the demand for rugged tablets. As a result, the Global Rugged Tablet Computers Market is set to play a crucial role in supporting the technological needs of various industries, ensuring they can operate effectively in even the most demanding conditions.

| Report Metric | Details |

| Report Name | Rugged Tablet Computers Market |

| Accounted market size in year | US$ 786 million |

| Forecasted market size in 2031 | US$ 1044 million |

| CAGR | 4.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Panasonic, Xplore, DRS Technology, Getac, DT Research, Dell, MobileDemand, AAEON, NEXCOM, HP, MilDef, Trimble, Kontron |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |