What is Global MEMS Variable Optical Attenuators (VOA) Market?

The Global MEMS Variable Optical Attenuators (VOA) Market is a specialized segment within the broader optical components industry. MEMS, or Micro-Electro-Mechanical Systems, are tiny devices that integrate electrical and mechanical components at a microscale. In the context of VOAs, these systems are used to control the power levels of optical signals in fiber optic networks. This is crucial for maintaining signal integrity and preventing overloads in communication systems. The market for MEMS VOAs is driven by the increasing demand for high-speed internet and the expansion of telecommunication networks worldwide. As data consumption continues to rise, the need for efficient and reliable optical components becomes more critical. MEMS VOAs offer advantages such as compact size, low power consumption, and high precision, making them an attractive choice for network operators and equipment manufacturers. The market is characterized by technological advancements and innovations aimed at improving performance and reducing costs. As a result, the Global MEMS VOA Market is poised for steady growth, driven by the ongoing expansion of digital infrastructure and the increasing reliance on fiber optic communication systems.

Single Channel, Multi-Channel in the Global MEMS Variable Optical Attenuators (VOA) Market:

In the Global MEMS Variable Optical Attenuators (VOA) Market, Single Channel and Multi-Channel VOAs serve distinct yet complementary roles. Single Channel VOAs are designed to manage the optical signal power in a single fiber optic channel. They are typically used in applications where precise control of individual channels is required, such as in point-to-point communication links or in systems where channel-specific adjustments are necessary. These VOAs are valued for their simplicity and cost-effectiveness, making them suitable for smaller networks or specific applications where only a few channels need to be managed. On the other hand, Multi-Channel VOAs are engineered to handle multiple optical channels simultaneously. This capability is essential in dense wavelength division multiplexing (DWDM) systems, where numerous channels are transmitted over a single fiber. Multi-Channel VOAs provide the flexibility to adjust the power levels of multiple channels independently, ensuring optimal performance across the entire network. This is particularly important in large-scale telecommunication networks and data centers, where efficient management of numerous channels is crucial for maintaining high data throughput and network reliability. The choice between Single Channel and Multi-Channel VOAs depends on the specific requirements of the network and the level of control needed over the optical signals. As the demand for high-speed data transmission continues to grow, both types of VOAs play a vital role in ensuring the efficiency and reliability of fiber optic communication systems. The market for these devices is driven by the ongoing expansion of digital infrastructure and the increasing complexity of optical networks. Technological advancements in MEMS technology have enabled the development of more sophisticated and efficient VOAs, further enhancing their appeal to network operators and equipment manufacturers. As a result, the Global MEMS VOA Market is expected to witness continued growth, fueled by the rising demand for high-performance optical components in the telecommunications industry.

Fiber Optical Communiction System, Test Equipment, Others in the Global MEMS Variable Optical Attenuators (VOA) Market:

The usage of Global MEMS Variable Optical Attenuators (VOA) Market spans several critical areas, including Fiber Optical Communication Systems, Test Equipment, and other applications. In Fiber Optical Communication Systems, MEMS VOAs are essential for managing the power levels of optical signals transmitted over fiber optic cables. They help maintain signal integrity by preventing overloads and ensuring that the signals remain within the optimal power range. This is crucial for achieving high-speed data transmission and minimizing signal loss over long distances. MEMS VOAs are used in various components of fiber optic networks, including optical amplifiers, transceivers, and multiplexers, where precise control of signal power is necessary for optimal performance. In the realm of Test Equipment, MEMS VOAs are used to simulate different network conditions and test the performance of optical components and systems. They allow engineers to adjust the power levels of test signals, enabling them to evaluate the behavior of optical devices under various scenarios. This is important for ensuring the reliability and efficiency of optical networks before they are deployed in the field. MEMS VOAs are also used in laboratory settings for research and development purposes, where they provide the flexibility needed to conduct a wide range of experiments and tests. Beyond these primary applications, MEMS VOAs find use in other areas such as sensor networks, medical imaging, and industrial automation. In sensor networks, they help manage the power levels of optical signals used for data transmission and sensing applications. In medical imaging, MEMS VOAs are used to control the intensity of light sources, improving the quality and accuracy of imaging systems. In industrial automation, they are used to regulate the power levels of optical signals in automated systems, ensuring precise control and operation. The versatility and precision of MEMS VOAs make them valuable components in a wide range of applications, contributing to the growth and development of the Global MEMS VOA Market. As technology continues to advance, the demand for high-performance optical components is expected to rise, further driving the adoption of MEMS VOAs in various industries.

Global MEMS Variable Optical Attenuators (VOA) Market Outlook:

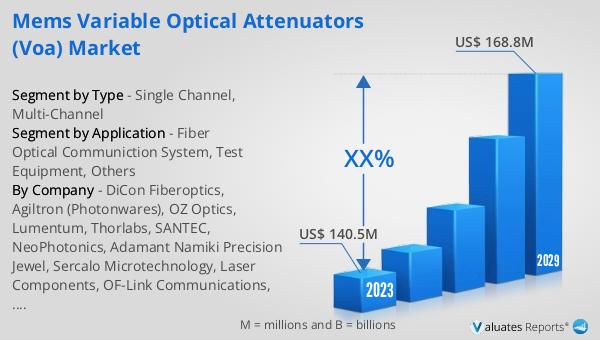

The global market for MEMS Variable Optical Attenuators (VOA) was valued at $144 million in 2024 and is anticipated to expand to a revised size of $178 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.1% during the forecast period. This growth trajectory underscores the increasing demand for MEMS VOAs across various industries, driven by the need for efficient and reliable optical components in fiber optic communication systems. The steady growth rate indicates a robust market outlook, supported by technological advancements and the ongoing expansion of digital infrastructure. As the telecommunications industry continues to evolve, the demand for high-speed data transmission and efficient network management solutions is expected to rise, further fueling the growth of the MEMS VOA market. The projected market size of $178 million by 2031 highlights the significant opportunities for manufacturers and suppliers in this sector, as they strive to meet the growing demand for high-performance optical components. The market's positive outlook is also indicative of the increasing adoption of MEMS technology in various applications, as industries seek to leverage the benefits of compact size, low power consumption, and high precision offered by MEMS VOAs. As a result, the Global MEMS VOA Market is poised for continued growth and development, driven by the increasing reliance on fiber optic communication systems and the need for advanced optical components to support the digital transformation of industries worldwide.

| Report Metric | Details |

| Report Name | MEMS Variable Optical Attenuators (VOA) Market |

| Accounted market size in year | US$ 144 million |

| Forecasted market size in 2031 | US$ 178 million |

| CAGR | 3.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | DiCon Fiberoptics, Agiltron (Photonwares), OZ Optics, Lumentum, Thorlabs, SANTEC, NeoPhotonics, Adamant Namiki Precision Jewel, Sercalo Microtechnology, Laser Components, OF-Link Communications, BizLink Group, Guilin GLsun Science and Tech, Sichuan Ziguan Photonics Technology, Shenzhen Anylink Technology, Huayue Technology, Honghui Optics Communication TECH |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |