What is Global Boron Doped Stress Rod Market?

The Global Boron Doped Stress Rod Market is a specialized segment within the materials industry, focusing on the production and application of stress rods that are enhanced with boron doping. These rods are primarily used in various high-tech and industrial applications due to their unique properties, such as increased strength, durability, and resistance to environmental stressors. Boron doping involves the introduction of boron atoms into the crystal lattice of the rod material, which significantly improves its mechanical and thermal properties. This makes boron-doped stress rods particularly valuable in industries that require materials capable of withstanding extreme conditions, such as aerospace, telecommunications, and heavy machinery. The market for these specialized rods is driven by the growing demand for advanced materials that can enhance the performance and longevity of critical components in various applications. As industries continue to push the boundaries of technology and performance, the need for materials like boron-doped stress rods is expected to grow, making this market an important area of focus for manufacturers and researchers alike.

Diameter Below 5mm, Diameter 5-10mm, Diameter above 10mm in the Global Boron Doped Stress Rod Market:

In the Global Boron Doped Stress Rod Market, the diameter of the rods plays a crucial role in determining their application and performance characteristics. Rods with a diameter below 5mm are typically used in applications where precision and flexibility are paramount. These smaller diameter rods are often employed in intricate components of electronic devices and communication systems, where space is limited, and the components must withstand significant stress without compromising performance. The smaller diameter allows for greater flexibility and adaptability in design, making them ideal for use in compact and complex assemblies. On the other hand, rods with a diameter ranging from 5mm to 10mm are commonly used in applications that require a balance between strength and flexibility. This size range is particularly popular in the aerospace industry, where components must be lightweight yet strong enough to endure the stresses of flight. The intermediate diameter provides the necessary strength without adding excessive weight, which is crucial for maintaining fuel efficiency and performance in aircraft. Additionally, these rods are used in industrial machinery and equipment, where they contribute to the durability and reliability of moving parts. For applications requiring maximum strength and durability, rods with a diameter above 10mm are preferred. These larger diameter rods are used in heavy-duty industrial applications, such as construction and mining equipment, where they must withstand extreme forces and harsh environmental conditions. The increased diameter provides the necessary structural integrity to support heavy loads and resist deformation, ensuring the longevity and safety of the equipment. Furthermore, these rods are also used in infrastructure projects, such as bridges and tunnels, where their strength and durability are critical to the stability and safety of the structures. Overall, the choice of rod diameter in the Global Boron Doped Stress Rod Market is dictated by the specific requirements of the application, with each size offering distinct advantages in terms of strength, flexibility, and performance.

Communication, Aerospace, Industrial, Others in the Global Boron Doped Stress Rod Market:

The Global Boron Doped Stress Rod Market finds its applications across various sectors, each benefiting from the unique properties of these advanced materials. In the communication sector, boron-doped stress rods are used in the construction of fiber optic cables and other communication infrastructure. The enhanced strength and durability of these rods ensure the reliability and longevity of communication networks, which are critical for maintaining connectivity in today's digital world. The rods' ability to withstand environmental stressors, such as temperature fluctuations and mechanical stress, makes them ideal for use in outdoor and underground installations, where they must endure harsh conditions without compromising performance. In the aerospace industry, boron-doped stress rods are used in the construction of aircraft components, where their lightweight and high-strength properties are essential for maintaining fuel efficiency and performance. These rods are used in various parts of the aircraft, including the fuselage, wings, and landing gear, where they contribute to the overall structural integrity and safety of the aircraft. The ability of these rods to withstand the extreme conditions of flight, such as high temperatures and mechanical stress, makes them an invaluable component in modern aerospace engineering. In the industrial sector, boron-doped stress rods are used in the construction of machinery and equipment, where their strength and durability are critical for ensuring the reliability and longevity of the equipment. These rods are used in various applications, including the construction of heavy-duty machinery, such as cranes and excavators, where they must withstand extreme forces and harsh environmental conditions. The enhanced properties of these rods ensure the safety and efficiency of industrial operations, making them a valuable asset in the manufacturing and construction industries. Additionally, boron-doped stress rods are used in other sectors, such as the automotive and energy industries, where their unique properties contribute to the performance and efficiency of various components. In the automotive industry, these rods are used in the construction of lightweight and high-strength components, such as chassis and suspension systems, where they contribute to the overall performance and safety of the vehicle. In the energy sector, boron-doped stress rods are used in the construction of wind turbines and other renewable energy infrastructure, where their strength and durability are essential for ensuring the reliability and efficiency of energy production. Overall, the Global Boron Doped Stress Rod Market plays a critical role in various industries, providing advanced materials that enhance the performance and longevity of critical components in a wide range of applications.

Global Boron Doped Stress Rod Market Outlook:

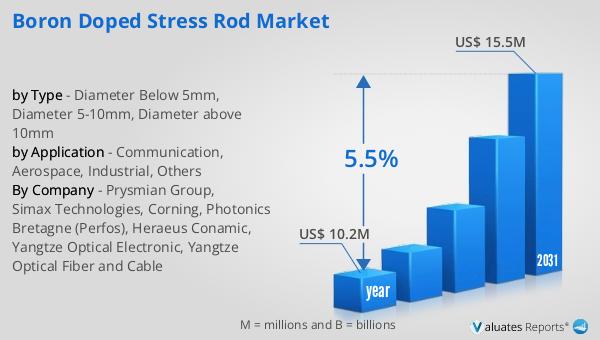

The global market for Boron Doped Stress Rods was valued at $10.2 million in 2024, with projections indicating a growth to $15.5 million by 2031. This growth represents a compound annual growth rate (CAGR) of 5.5% over the forecast period. This steady increase in market size reflects the growing demand for advanced materials that offer enhanced performance and durability across various industries. As industries continue to evolve and push the boundaries of technology, the need for materials that can withstand extreme conditions and enhance the performance of critical components is becoming increasingly important. Boron-doped stress rods, with their unique properties, are well-positioned to meet this demand, making them a valuable asset in the materials industry. The projected growth in the market size is a testament to the increasing recognition of the value of these advanced materials and their potential to drive innovation and efficiency in various applications. As the market continues to grow, manufacturers and researchers are likely to focus on developing new and improved boron-doped stress rods that offer even greater performance and durability, further driving the growth of this specialized market.

| Report Metric | Details |

| Report Name | Boron Doped Stress Rod Market |

| Accounted market size in year | US$ 10.2 million |

| Forecasted market size in 2031 | US$ 15.5 million |

| CAGR | 5.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Prysmian Group, Simax Technologies, Corning, Photonics Bretagne (Perfos), Heraeus Conamic, Yangtze Optical Electronic, Yangtze Optical Fiber and Cable |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |