What is Global Semiconductor Thermal Type Mass Flow Controller Market?

The Global Semiconductor Thermal Type Mass Flow Controller Market is a specialized segment within the broader semiconductor industry, focusing on devices that precisely control the flow of gases during semiconductor manufacturing processes. These controllers are crucial for maintaining the exact conditions required for producing high-quality semiconductor wafers. They ensure that the flow of gases, which are often used in various stages of semiconductor fabrication, is consistent and accurate. This precision is vital because even minor deviations can lead to defects in the semiconductor products, affecting their performance and reliability. The market for these controllers is driven by the increasing demand for semiconductors across various industries, including electronics, automotive, and telecommunications. As technology advances, the need for more sophisticated and efficient semiconductor devices grows, further propelling the demand for thermal type mass flow controllers. These controllers are integral to processes such as chemical vapor deposition (CVD), physical vapor deposition (PVD), and etching, all of which are essential in creating the intricate structures found in modern semiconductor devices. The market is characterized by continuous innovation, with manufacturers striving to develop controllers that offer greater precision, reliability, and ease of integration into existing semiconductor manufacturing systems.

Digital MFC, Analog MFC in the Global Semiconductor Thermal Type Mass Flow Controller Market:

Digital Mass Flow Controllers (MFCs) and Analog MFCs are two primary types of devices used in the Global Semiconductor Thermal Type Mass Flow Controller Market, each offering distinct advantages and features. Digital MFCs are known for their advanced capabilities, including enhanced accuracy, repeatability, and the ability to interface with digital systems. They utilize microprocessors to control and monitor the flow of gases, allowing for precise adjustments and real-time data feedback. This digital interface enables seamless integration with modern semiconductor manufacturing equipment, which often relies on computerized systems for operation. The ability to store and recall flow settings is another advantage of digital MFCs, making them ideal for processes that require frequent changes in gas flow parameters. Additionally, digital MFCs often come with self-diagnostic features, which help in maintaining optimal performance and reducing downtime. On the other hand, Analog MFCs are valued for their simplicity and reliability. They operate using analog signals to control gas flow, which can be advantageous in environments where digital systems may be susceptible to interference or failure. Analog MFCs are often easier to troubleshoot and repair, as they do not rely on complex software or digital components. This makes them a preferred choice in applications where robustness and ease of maintenance are prioritized. Despite their differences, both digital and analog MFCs play crucial roles in the semiconductor manufacturing process. They ensure that the precise flow of gases is maintained, which is essential for achieving the desired chemical reactions and physical properties in semiconductor materials. The choice between digital and analog MFCs often depends on the specific requirements of the manufacturing process, including factors such as the level of precision needed, the complexity of the system, and the available budget. As the semiconductor industry continues to evolve, the demand for both types of MFCs is expected to grow, driven by the need for more efficient and reliable manufacturing processes. Manufacturers of MFCs are continually innovating to improve the performance and capabilities of their products, ensuring that they meet the ever-changing needs of the semiconductor industry. This includes developing MFCs that can handle a wider range of gases, operate at higher temperatures, and provide more accurate flow measurements. The integration of advanced materials and technologies, such as MEMS (Micro-Electro-Mechanical Systems) and IoT (Internet of Things), is also playing a significant role in the evolution of MFCs, offering new possibilities for enhancing their functionality and performance. Overall, both digital and analog MFCs are indispensable tools in the semiconductor manufacturing process, each offering unique benefits that cater to different aspects of the industry's needs.

Semiconductor Processing Furnace, PVD&CVD equipment, Etching equipment, Others in the Global Semiconductor Thermal Type Mass Flow Controller Market:

The Global Semiconductor Thermal Type Mass Flow Controller Market finds extensive usage in various areas of semiconductor manufacturing, including Semiconductor Processing Furnaces, PVD & CVD equipment, Etching equipment, and other related processes. In Semiconductor Processing Furnaces, mass flow controllers are essential for regulating the flow of gases that are used to create the ideal environment for processing semiconductor wafers. These furnaces require precise control of temperature and gas composition to ensure that the wafers are processed correctly, and MFCs play a crucial role in achieving this precision. In PVD (Physical Vapor Deposition) and CVD (Chemical Vapor Deposition) equipment, MFCs are used to control the flow of precursor gases that are deposited onto the wafer surface to form thin films. The accuracy and consistency of gas flow are critical in these processes, as they directly impact the quality and uniformity of the deposited films. MFCs ensure that the correct amount of gas is delivered at the right time, enabling the formation of high-quality films with the desired properties. In Etching equipment, MFCs are used to control the flow of etching gases that remove material from the wafer surface to create the desired patterns and structures. The precision of gas flow is vital in etching processes, as it determines the accuracy and resolution of the etched features. MFCs help maintain the necessary conditions for achieving the desired etching results, ensuring that the final semiconductor devices meet the required specifications. Beyond these specific applications, MFCs are also used in other areas of semiconductor manufacturing, such as doping, annealing, and cleaning processes. In each of these applications, the ability to precisely control gas flow is essential for achieving the desired outcomes and ensuring the quality and reliability of the final semiconductor products. The versatility and reliability of MFCs make them indispensable tools in the semiconductor industry, enabling manufacturers to produce high-performance devices that meet the demands of modern technology. As the semiconductor industry continues to advance, the role of MFCs in these processes is expected to grow, driven by the need for more efficient and precise manufacturing techniques.

Global Semiconductor Thermal Type Mass Flow Controller Market Outlook:

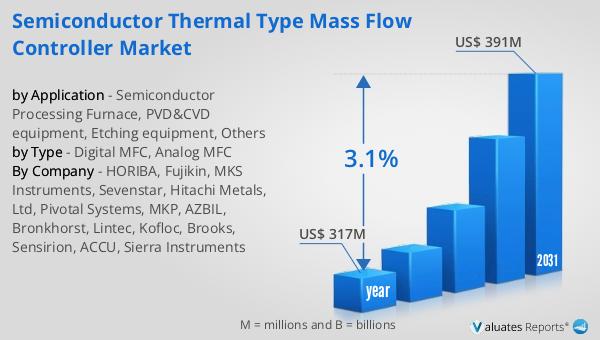

The outlook for the Global Semiconductor Thermal Type Mass Flow Controller Market indicates a promising growth trajectory. In 2024, the market was valued at approximately $317 million, and it is anticipated to expand to around $391 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.1% over the forecast period. This growth is indicative of the increasing demand for precision and efficiency in semiconductor manufacturing processes, where thermal type mass flow controllers play a critical role. These devices are essential for maintaining the precise flow of gases required in various stages of semiconductor fabrication, ensuring the production of high-quality semiconductor wafers. The broader semiconductor market also shows robust growth potential. In 2022, the global semiconductor market was estimated at $579 billion, with projections suggesting it could reach $790 billion by 2029, growing at a CAGR of 6% during the forecast period. This growth is driven by the rising demand for semiconductors across various industries, including electronics, automotive, and telecommunications. As technology continues to evolve, the need for more sophisticated and efficient semiconductor devices is expected to increase, further boosting the demand for thermal type mass flow controllers. These controllers are integral to processes such as chemical vapor deposition (CVD), physical vapor deposition (PVD), and etching, all of which are essential in creating the intricate structures found in modern semiconductor devices. The market is characterized by continuous innovation, with manufacturers striving to develop controllers that offer greater precision, reliability, and ease of integration into existing semiconductor manufacturing systems. Overall, the outlook for the Global Semiconductor Thermal Type Mass Flow Controller Market is positive, with steady growth expected in the coming years.

| Report Metric | Details |

| Report Name | Semiconductor Thermal Type Mass Flow Controller Market |

| Accounted market size in year | US$ 317 million |

| Forecasted market size in 2031 | US$ 391 million |

| CAGR | 3.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | HORIBA, Fujikin, MKS Instruments, Sevenstar, Hitachi Metals, Ltd, Pivotal Systems, MKP, AZBIL, Bronkhorst, Lintec, Kofloc, Brooks, Sensirion, ACCU, Sierra Instruments |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |