What is Embedded Wi-Fi Chip - Global Market?

Embedded Wi-Fi chips are integral components in the global market, serving as the backbone for wireless connectivity in a multitude of devices. These chips enable devices to connect to the internet without the need for physical cables, facilitating seamless communication and data exchange. The global market for embedded Wi-Fi chips is driven by the increasing demand for smart devices and the Internet of Things (IoT), which require reliable and efficient wireless connectivity. These chips are embedded in various electronic devices, ranging from smartphones and tablets to smart home appliances and industrial machinery. The market is characterized by rapid technological advancements, with manufacturers continuously innovating to improve the speed, range, and energy efficiency of these chips. As more devices become interconnected, the demand for embedded Wi-Fi chips is expected to grow, making them a crucial component in the digital ecosystem. The global market is also influenced by regional trends, with significant growth observed in regions with high technology adoption rates. Overall, embedded Wi-Fi chips play a vital role in enabling the digital transformation of industries and enhancing the connectivity of everyday devices.

WiFi 4/5, WiFi 6/7, Others in the Embedded Wi-Fi Chip - Global Market:

WiFi technology has evolved significantly over the years, with each new generation offering improved performance and capabilities. WiFi 4, also known as 802.11n, was a significant leap forward from its predecessors, offering faster speeds and better range. It introduced MIMO (Multiple Input Multiple Output) technology, which allowed for multiple data streams to be transmitted simultaneously, improving overall network efficiency. WiFi 5, or 802.11ac, further enhanced these capabilities by operating on the 5 GHz band, which is less congested than the 2.4 GHz band used by previous generations. This allowed for even faster data transfer rates and reduced interference from other devices. WiFi 6, or 802.11ax, represents a major advancement in WiFi technology, offering increased capacity, efficiency, and performance in dense environments. It introduces technologies such as OFDMA (Orthogonal Frequency Division Multiple Access) and MU-MIMO (Multi-User MIMO), which allow for more efficient use of available bandwidth and improved performance for multiple users. WiFi 6 also offers improved battery life for connected devices, thanks to its Target Wake Time (TWT) feature, which allows devices to schedule when they wake up to send or receive data. WiFi 7, or 802.11be, is the next step in WiFi evolution, promising even higher speeds and lower latency. It is expected to support new applications such as augmented reality (AR) and virtual reality (VR), which require high data rates and low latency. WiFi 7 will also introduce new features such as multi-link operation, which allows devices to connect to multiple WiFi bands simultaneously, improving reliability and performance. Other advancements in embedded Wi-Fi chips include improved security features, such as WPA3, which offers enhanced protection against cyber threats. These advancements are crucial as more devices become connected to the internet, increasing the potential for security breaches. The global market for embedded Wi-Fi chips is also influenced by the growing demand for smart home devices, which require reliable and secure wireless connectivity. As WiFi technology continues to evolve, embedded Wi-Fi chips will play a crucial role in enabling new applications and improving the performance of existing ones. The global market for these chips is expected to grow as more devices become connected and demand for high-speed, reliable wireless connectivity increases.

Consumer Electronic, Household Appliance, Automotive, Industrial, Others in the Embedded Wi-Fi Chip - Global Market:

Embedded Wi-Fi chips are used in a wide range of applications, each with its own unique requirements and challenges. In the consumer electronics sector, these chips are used in devices such as smartphones, tablets, and laptops, where they enable wireless internet connectivity and data transfer. The demand for high-speed, reliable Wi-Fi connectivity in these devices is driven by the increasing consumption of online content, such as streaming video and online gaming. In household appliances, embedded Wi-Fi chips are used to enable smart home features, such as remote control and monitoring. For example, smart refrigerators can use Wi-Fi connectivity to send alerts when the door is left open or when the temperature rises above a certain level. In the automotive industry, embedded Wi-Fi chips are used to enable features such as in-car entertainment systems, navigation, and vehicle-to-vehicle communication. These features require reliable, high-speed connectivity to function effectively, making embedded Wi-Fi chips a crucial component in modern vehicles. In the industrial sector, embedded Wi-Fi chips are used in applications such as remote monitoring and control of machinery, where they enable real-time data exchange and improve operational efficiency. Other applications of embedded Wi-Fi chips include healthcare devices, where they enable remote monitoring of patients and data exchange between medical devices. The global market for embedded Wi-Fi chips is driven by the increasing demand for these applications, as well as the growing adoption of IoT devices, which require reliable and efficient wireless connectivity. As more devices become connected, the demand for embedded Wi-Fi chips is expected to grow, making them a crucial component in the digital ecosystem.

Embedded Wi-Fi Chip - Global Market Outlook:

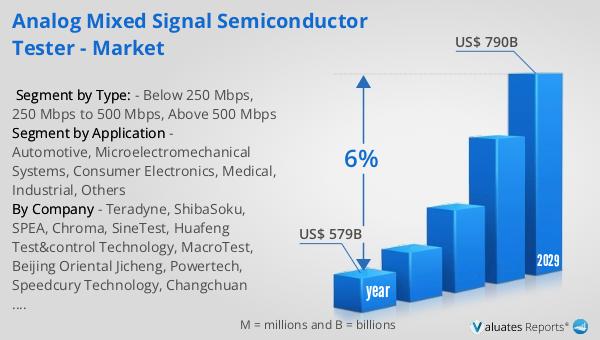

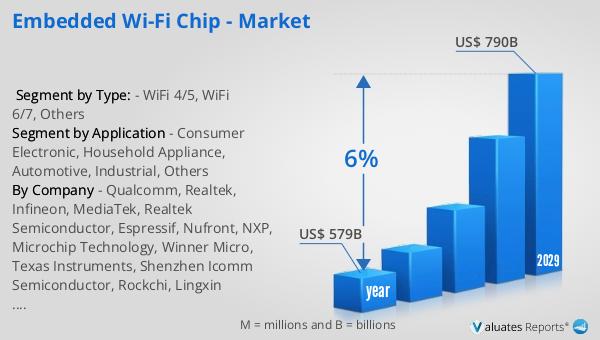

The semiconductor market, which includes embedded Wi-Fi chips, is experiencing significant growth. In 2022, the global semiconductor market was valued at approximately $579 billion. This market is projected to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, and industrial sectors. The rise of IoT devices and the growing need for high-speed, reliable wireless connectivity are also contributing to the expansion of the semiconductor market. As more devices become interconnected, the demand for semiconductors, including embedded Wi-Fi chips, is expected to increase. This growth presents significant opportunities for manufacturers and suppliers in the semiconductor industry, as they work to meet the increasing demand for these critical components. The global semiconductor market is also influenced by regional trends, with significant growth observed in regions with high technology adoption rates. Overall, the semiconductor market is poised for continued growth, driven by the increasing demand for advanced technologies and the ongoing digital transformation of industries.

| Report Metric | Details |

| Report Name | Embedded Wi-Fi Chip - Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Qualcomm, Realtek, Infineon, MediaTek, Realtek Semiconductor, Espressif, Nufront, NXP, Microchip Technology, Winner Micro, Texas Instruments, Shenzhen Icomm Semiconductor, Rockchi, Lingxin Microelectronics, Fn-Link Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |