What is Feed Grade Vitamin B6 - Global Market?

Feed Grade Vitamin B6 is a crucial component in the global market, primarily used in animal nutrition. This vitamin, also known as pyridoxine, plays a vital role in the metabolism of proteins, fats, and carbohydrates, making it essential for the growth and development of animals. The global market for Feed Grade Vitamin B6 is driven by the increasing demand for high-quality animal feed, which is necessary to meet the growing consumption of meat and dairy products worldwide. As livestock farming becomes more intensive, the need for efficient feed additives like Vitamin B6 becomes more pronounced. This vitamin helps improve the overall health and productivity of animals, leading to better yields for farmers. Additionally, the rising awareness about the benefits of balanced animal nutrition is propelling the demand for feed additives, including Vitamin B6. The market is characterized by a diverse range of suppliers and manufacturers who are constantly innovating to enhance the quality and efficacy of their products. As a result, the Feed Grade Vitamin B6 market is expected to witness steady growth in the coming years, driven by advancements in animal nutrition science and the increasing focus on sustainable farming practices.

Powder, Granule in the Feed Grade Vitamin B6 - Global Market:

In the global market for Feed Grade Vitamin B6, two primary forms are prevalent: powder and granule. Each form has its unique characteristics and applications, catering to different needs within the animal feed industry. Powdered Vitamin B6 is widely used due to its ease of mixing and uniform distribution in feed formulations. This form is particularly beneficial for manufacturers who require precise dosing and consistent quality in their feed products. The fine texture of the powder allows it to blend seamlessly with other feed ingredients, ensuring that animals receive the necessary nutrients in every bite. On the other hand, granule form offers advantages in terms of handling and storage. Granules are less prone to dust formation, reducing the risk of inhalation by workers during the manufacturing process. This form is also preferred in automated feed production systems, where flowability and ease of measurement are crucial. Granules tend to have a longer shelf life compared to powders, making them a cost-effective option for feed manufacturers. The choice between powder and granule forms often depends on the specific requirements of the feed formulation and the production capabilities of the manufacturer. In regions with high humidity, granules may be favored due to their resistance to moisture absorption, which helps maintain the stability and potency of the vitamin. Conversely, in areas where precise nutrient blending is critical, powders might be the preferred choice. The versatility of Feed Grade Vitamin B6 in both powder and granule forms allows it to cater to a wide range of applications in the animal feed industry. As the demand for high-quality animal nutrition continues to rise, manufacturers are investing in research and development to enhance the properties of both forms. Innovations in encapsulation and coating technologies are being explored to improve the stability and bioavailability of Vitamin B6 in feed formulations. These advancements aim to maximize the nutritional benefits of the vitamin while minimizing losses during storage and processing. Furthermore, the global market for Feed Grade Vitamin B6 is influenced by regulatory standards and quality certifications. Manufacturers must adhere to stringent guidelines to ensure the safety and efficacy of their products. This includes rigorous testing for purity, potency, and absence of contaminants. Compliance with international standards not only enhances the credibility of manufacturers but also boosts consumer confidence in the quality of feed products. As the market evolves, collaborations between feed manufacturers, nutritionists, and researchers are becoming increasingly important. These partnerships facilitate the exchange of knowledge and expertise, leading to the development of innovative feed solutions that address the specific needs of different animal species. The integration of advanced technologies, such as precision nutrition and data analytics, is also shaping the future of the Feed Grade Vitamin B6 market. By leveraging these tools, manufacturers can optimize feed formulations to meet the nutritional requirements of animals more effectively. In conclusion, the global market for Feed Grade Vitamin B6 in powder and granule forms is poised for growth, driven by the increasing demand for high-quality animal nutrition. The versatility and adaptability of these forms make them indispensable in the animal feed industry, catering to diverse needs and preferences. As manufacturers continue to innovate and improve their products, the market is expected to witness significant advancements in the coming years, contributing to the overall sustainability and efficiency of livestock farming.

Aquatic Feed, Poultry Feed, Others in the Feed Grade Vitamin B6 - Global Market:

Feed Grade Vitamin B6 plays a significant role in various areas of animal nutrition, including aquatic feed, poultry feed, and other livestock feed. In aquatic feed, Vitamin B6 is essential for the growth and development of fish and other aquatic species. It aids in the metabolism of amino acids, which are crucial for protein synthesis and energy production. This vitamin also supports the immune system of aquatic animals, helping them resist diseases and stress. The inclusion of Vitamin B6 in aquatic feed formulations ensures that fish and other species receive balanced nutrition, promoting healthy growth and improving feed conversion ratios. In poultry feed, Vitamin B6 is vital for the overall health and productivity of birds. It supports the synthesis of neurotransmitters, which are essential for proper nerve function and muscle coordination. This vitamin also plays a role in the formation of red blood cells, ensuring adequate oxygen transport throughout the body. By enhancing the immune response, Vitamin B6 helps poultry resist infections and recover quickly from illnesses. The use of this vitamin in poultry feed formulations contributes to better egg production, improved growth rates, and enhanced feed efficiency. In addition to aquatic and poultry feed, Feed Grade Vitamin B6 is used in the nutrition of other livestock, such as swine, cattle, and sheep. In swine feed, this vitamin supports the metabolism of fats and carbohydrates, providing energy for growth and reproduction. It also aids in the synthesis of hemoglobin, which is crucial for oxygen transport in pigs. In cattle and sheep, Vitamin B6 is important for the metabolism of amino acids and the synthesis of proteins, which are essential for muscle development and milk production. The inclusion of this vitamin in livestock feed formulations ensures that animals receive the necessary nutrients for optimal growth and productivity. The use of Feed Grade Vitamin B6 in these areas is driven by the increasing demand for high-quality animal products, such as meat, milk, and eggs. As consumers become more conscious of the nutritional value and safety of animal products, the need for balanced and nutritious feed formulations becomes more pronounced. Feed manufacturers are investing in research and development to enhance the efficacy and bioavailability of Vitamin B6 in feed formulations. This includes exploring new delivery systems and formulations that maximize the nutritional benefits of the vitamin while minimizing losses during storage and processing. In conclusion, Feed Grade Vitamin B6 is an essential component of animal nutrition, playing a crucial role in aquatic feed, poultry feed, and other livestock feed. Its benefits in supporting growth, metabolism, and immune function make it indispensable in the animal feed industry. As the demand for high-quality animal products continues to rise, the use of Vitamin B6 in feed formulations is expected to increase, contributing to the overall sustainability and efficiency of livestock farming.

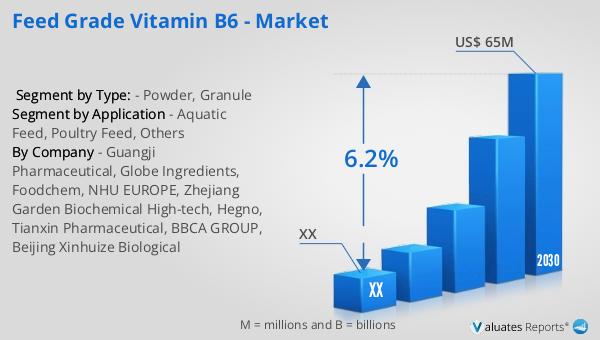

Feed Grade Vitamin B6 - Global Market Outlook:

The global market for Feed Grade Vitamin B6 was valued at approximately $43 million in 2023. Looking ahead, it is projected to grow significantly, reaching an estimated value of $65 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 6.2% over the forecast period from 2024 to 2030. This upward trend in the market is indicative of the increasing demand for high-quality animal nutrition products. As the livestock industry continues to expand, driven by the rising consumption of meat and dairy products, the need for efficient feed additives like Vitamin B6 becomes more critical. This vitamin is essential for the growth and development of animals, supporting various metabolic processes and enhancing overall health and productivity. The market's growth is also fueled by advancements in animal nutrition science and the increasing focus on sustainable farming practices. Manufacturers are investing in research and development to improve the quality and efficacy of their products, ensuring that they meet the evolving needs of the animal feed industry. Additionally, the rising awareness about the benefits of balanced animal nutrition is propelling the demand for feed additives, including Vitamin B6. As a result, the global market for Feed Grade Vitamin B6 is expected to witness steady growth in the coming years, contributing to the overall sustainability and efficiency of livestock farming.

| Report Metric | Details |

| Report Name | Feed Grade Vitamin B6 - Market |

| Forecasted market size in 2030 | US$ 65 million |

| CAGR | 6.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Guangji Pharmaceutical, Globe Ingredients, Foodchem, NHU EUROPE, Zhejiang Garden Biochemical High-tech, Hegno, Tianxin Pharmaceutical, BBCA GROUP, Beijing Xinhuize Biological |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |