What is Baking Bread Mold Machines - Global Market?

Baking bread mold machines are specialized equipment used in the baking industry to shape and form dough into various bread types. These machines are crucial for both small-scale bakeries and large industrial baking operations. They help streamline the bread-making process by automating the shaping and molding stages, ensuring consistency in size and shape, which is vital for both aesthetic and functional purposes. The global market for these machines is driven by the increasing demand for bakery products worldwide, as bread remains a staple food in many cultures. Technological advancements have led to the development of more efficient and versatile machines that can handle different types of dough and produce a wide range of bread products. The market is also influenced by the growing trend of artisanal and specialty breads, which require specific molds and shapes. As consumer preferences evolve, manufacturers are focusing on creating machines that offer flexibility and customization to meet diverse baking needs. The market is expected to grow steadily as more bakeries and food service providers invest in modern equipment to enhance productivity and product quality.

Vertical, Horizontal in the Baking Bread Mold Machines - Global Market:

In the realm of baking bread mold machines, the market is segmented into vertical and horizontal machines, each serving distinct purposes and offering unique advantages. Vertical baking bread mold machines are designed to occupy less floor space, making them ideal for bakeries with limited space. These machines typically feature a vertical stacking system, where dough is fed from the top and shaped as it moves downward through the machine. This design allows for efficient use of space and is often favored by small to medium-sized bakeries. Vertical machines are known for their ease of use and maintenance, as well as their ability to produce consistent results. They are particularly suited for producing standard loaf shapes and are often used in conjunction with other baking equipment to streamline the production process. On the other hand, horizontal baking bread mold machines are designed for larger-scale operations and are capable of handling higher volumes of dough. These machines feature a horizontal conveyor system that moves dough through various shaping and molding stages. Horizontal machines are typically more robust and versatile, capable of producing a wide range of bread shapes and sizes. They are often used in industrial baking settings where high throughput and efficiency are paramount. The horizontal design allows for greater flexibility in terms of customization, as different molds and attachments can be used to create unique bread products. This makes them ideal for bakeries that produce a diverse range of bread types, from traditional loaves to specialty and artisanal breads. Both vertical and horizontal machines are equipped with advanced features such as programmable controls, automated cleaning systems, and energy-efficient components. These features enhance the overall efficiency and productivity of the machines, reducing labor costs and minimizing waste. As the demand for bakery products continues to rise, manufacturers are focusing on developing machines that offer greater precision and control over the baking process. This includes the ability to adjust parameters such as dough consistency, baking time, and temperature to achieve the desired results. In addition to their functional benefits, baking bread mold machines also contribute to sustainability efforts within the baking industry. By automating the shaping and molding process, these machines help reduce food waste and energy consumption. They also enable bakeries to produce consistent products with minimal variation, reducing the need for rework and ensuring customer satisfaction. As consumer preferences continue to evolve, the market for baking bread mold machines is expected to grow, driven by the need for efficient and versatile equipment that can meet the demands of modern bakeries.

Household, Commercial in the Baking Bread Mold Machines - Global Market:

Baking bread mold machines are utilized in both household and commercial settings, each with distinct applications and benefits. In household settings, these machines are often compact and user-friendly, designed to cater to the needs of home bakers who enjoy making bread from scratch. They offer convenience and consistency, allowing users to produce professional-quality bread with minimal effort. Household bread mold machines typically come with a variety of pre-set programs and adjustable settings, enabling users to experiment with different recipes and bread types. They are ideal for individuals who prefer homemade bread for its freshness and the ability to control ingredients. These machines also cater to the growing trend of home baking, fueled by the desire for healthier and more personalized food options. In commercial settings, baking bread mold machines play a crucial role in streamlining production processes and enhancing efficiency. Commercial machines are designed to handle larger volumes of dough and are equipped with advanced features to ensure consistent quality and output. They are used in bakeries, restaurants, and food service establishments to produce a wide range of bread products, from standard loaves to specialty and artisanal breads. The use of commercial bread mold machines allows businesses to meet high demand while maintaining product quality and consistency. These machines are often integrated with other baking equipment, such as ovens and proofers, to create a seamless production line. This integration helps reduce labor costs and improve overall productivity, enabling businesses to focus on innovation and customer satisfaction. In both household and commercial settings, baking bread mold machines contribute to sustainability efforts by reducing food waste and energy consumption. They enable precise control over the baking process, minimizing the risk of overproduction and ensuring that resources are used efficiently. As the demand for bakery products continues to grow, the use of baking bread mold machines in both household and commercial settings is expected to increase, driven by the need for efficient and reliable equipment that can meet the diverse needs of consumers and businesses alike.

Baking Bread Mold Machines - Global Market Outlook:

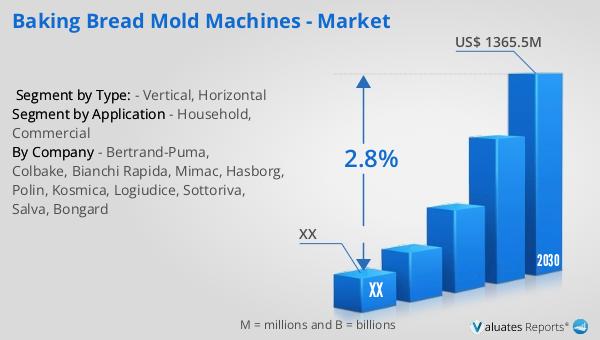

The global market for baking bread mold machines was valued at approximately $1,025 million in 2023. It is projected to grow to a revised size of around $1,365.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.8% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for efficient and versatile baking equipment across the globe. The North American market for baking bread mold machines, although not specified in exact figures, is also expected to experience growth during the same period. The market dynamics in North America are influenced by factors such as technological advancements, the rising popularity of artisanal and specialty breads, and the need for automation in the baking industry. As bakeries and food service providers in North America continue to invest in modern equipment to enhance productivity and product quality, the market for baking bread mold machines is poised for steady growth. The focus on sustainability and reducing food waste further drives the adoption of these machines, as they offer precise control over the baking process and help minimize resource consumption. Overall, the global and North American markets for baking bread mold machines are set to expand, driven by the evolving needs of consumers and businesses in the baking industry.

| Report Metric | Details |

| Report Name | Baking Bread Mold Machines - Market |

| Forecasted market size in 2030 | US$ 1365.5 million |

| CAGR | 2.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Bertrand-Puma, Colbake, Bianchi Rapida, Mimac, Hasborg, Polin, Kosmica, Logiudice, Sottoriva, Salva, Bongard |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |