What is Silicon Nitride Ceramic Ferrule - Global Market?

Silicon Nitride Ceramic Ferrule is a crucial component in the global market, primarily used in fiber optic communication systems. These ferrules are small cylindrical structures that align and protect the delicate fibers, ensuring efficient signal transmission. Silicon nitride, a high-performance ceramic material, is favored for its exceptional mechanical strength, thermal stability, and resistance to wear and corrosion. This makes it ideal for demanding applications where precision and durability are paramount. The global market for silicon nitride ceramic ferrules is driven by the increasing demand for high-speed internet and data services, which rely on robust fiber optic networks. As industries and consumers alike seek faster and more reliable connectivity, the need for advanced materials like silicon nitride in optical components continues to grow. The market is characterized by ongoing research and development efforts aimed at enhancing the performance and cost-effectiveness of these ferrules, making them more accessible for widespread use. With the rapid expansion of telecommunications infrastructure worldwide, the silicon nitride ceramic ferrule market is poised for significant growth, reflecting the broader trends in digital transformation and connectivity.

Single Mode Ferrule, Multimode Ferrule in the Silicon Nitride Ceramic Ferrule - Global Market:

In the realm of fiber optics, ferrules play a pivotal role in ensuring the precise alignment and protection of optical fibers. Silicon nitride ceramic ferrules, known for their superior mechanical properties and thermal stability, are increasingly being used in both single-mode and multimode fiber optic systems. Single-mode ferrules are designed for applications requiring high precision and minimal signal loss over long distances. They are typically used in telecommunications and data centers where high-speed data transmission is critical. The use of silicon nitride in single-mode ferrules enhances their durability and performance, making them ideal for environments where reliability is paramount. On the other hand, multimode ferrules are used in applications where data transmission over shorter distances is required, such as in local area networks (LANs) and data centers. These ferrules accommodate multiple light paths, allowing for greater data throughput. Silicon nitride's robustness ensures that multimode ferrules can withstand the rigors of high-density data environments. The global market for silicon nitride ceramic ferrules is witnessing a surge in demand due to the increasing reliance on fiber optic networks for high-speed internet and data services. As industries and consumers seek faster and more reliable connectivity, the need for advanced materials like silicon nitride in optical components continues to grow. The market is characterized by ongoing research and development efforts aimed at enhancing the performance and cost-effectiveness of these ferrules, making them more accessible for widespread use. With the rapid expansion of telecommunications infrastructure worldwide, the silicon nitride ceramic ferrule market is poised for significant growth, reflecting the broader trends in digital transformation and connectivity.

Aerospace, Military, Medical, Industrial, Others in the Silicon Nitride Ceramic Ferrule - Global Market:

Silicon nitride ceramic ferrules find extensive applications across various sectors, including aerospace, military, medical, industrial, and others, owing to their exceptional properties. In the aerospace industry, these ferrules are used in advanced communication systems, ensuring reliable data transmission in aircraft and spacecraft. Their high thermal stability and resistance to wear make them suitable for the harsh conditions encountered in aerospace applications. In the military sector, silicon nitride ceramic ferrules are employed in secure communication networks, where durability and precision are crucial. They are used in fiber optic systems for secure data transmission, ensuring that military operations can rely on robust and reliable communication channels. In the medical field, these ferrules are used in diagnostic equipment and surgical instruments, where precision and reliability are essential. Silicon nitride's biocompatibility and resistance to wear make it an ideal material for medical applications. In the industrial sector, silicon nitride ceramic ferrules are used in manufacturing processes that require high precision and durability. They are employed in fiber optic sensors and control systems, ensuring accurate data transmission and monitoring. Other applications include telecommunications and data centers, where the demand for high-speed internet and data services drives the need for advanced materials like silicon nitride. The global market for silicon nitride ceramic ferrules is witnessing a surge in demand due to the increasing reliance on fiber optic networks for high-speed internet and data services. As industries and consumers seek faster and more reliable connectivity, the need for advanced materials like silicon nitride in optical components continues to grow. The market is characterized by ongoing research and development efforts aimed at enhancing the performance and cost-effectiveness of these ferrules, making them more accessible for widespread use. With the rapid expansion of telecommunications infrastructure worldwide, the silicon nitride ceramic ferrule market is poised for significant growth, reflecting the broader trends in digital transformation and connectivity.

Silicon Nitride Ceramic Ferrule - Global Market Outlook:

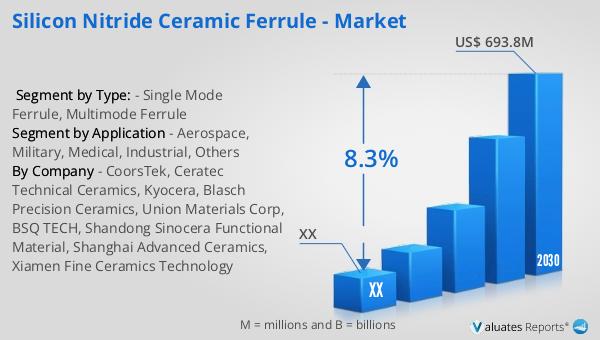

The global market for silicon nitride ceramic ferrules was valued at approximately $379 million in 2023. It is projected to grow significantly, reaching an estimated size of $693.8 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 8.3% during the forecast period from 2024 to 2030. The North American market for silicon nitride ceramic ferrules is also anticipated to experience substantial growth during this period. While specific figures for the North American market in 2023 and 2030 are not provided, it is clear that the region will contribute significantly to the overall market expansion. The increasing demand for high-speed internet and data services, coupled with the rapid expansion of telecommunications infrastructure, is driving the growth of the silicon nitride ceramic ferrule market. As industries and consumers seek faster and more reliable connectivity, the need for advanced materials like silicon nitride in optical components continues to grow. The market is characterized by ongoing research and development efforts aimed at enhancing the performance and cost-effectiveness of these ferrules, making them more accessible for widespread use. With the rapid expansion of telecommunications infrastructure worldwide, the silicon nitride ceramic ferrule market is poised for significant growth, reflecting the broader trends in digital transformation and connectivity.

| Report Metric | Details |

| Report Name | Silicon Nitride Ceramic Ferrule - Market |

| Forecasted market size in 2030 | US$ 693.8 million |

| CAGR | 8.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | CoorsTek, Ceratec Technical Ceramics, Kyocera, Blasch Precision Ceramics, Union Materials Corp, BSQ TECH, Shandong Sinocera Functional Material, Shanghai Advanced Ceramics, Xiamen Fine Ceramics Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |