What is Threat Modeling Tool - Global Market?

The Threat Modeling Tool - Global Market is a rapidly evolving sector that focuses on identifying, understanding, and mitigating potential security threats within software systems. These tools are essential for organizations aiming to protect their digital assets from cyber threats by providing a structured approach to identifying vulnerabilities and assessing the potential impact of various threats. By simulating potential attack scenarios, threat modeling tools help organizations prioritize security measures and allocate resources effectively. The global market for these tools is driven by the increasing complexity of cyber threats and the growing need for robust security frameworks across industries. As businesses continue to digitize their operations, the demand for advanced threat modeling solutions is expected to rise, making it a critical component of modern cybersecurity strategies. These tools not only help in identifying potential threats but also assist in designing more secure systems by integrating security considerations into the development process. This proactive approach to security is becoming increasingly important as organizations strive to protect sensitive data and maintain customer trust in an ever-evolving digital landscape.

Cloud, On-premises in the Threat Modeling Tool - Global Market:

Cloud and on-premises solutions are two primary deployment models for threat modeling tools in the global market, each offering distinct advantages and challenges. Cloud-based threat modeling tools are hosted on remote servers and accessed via the internet, providing flexibility and scalability that are particularly appealing to businesses with fluctuating demands. These solutions allow organizations to quickly scale their security measures without the need for significant upfront investments in hardware or infrastructure. Additionally, cloud-based tools often come with automatic updates and maintenance, ensuring that users always have access to the latest features and security patches. This model is especially beneficial for small and medium-sized enterprises (SMEs) that may lack the resources to maintain extensive IT infrastructure. However, cloud-based solutions also raise concerns about data privacy and security, as sensitive information is stored off-site and potentially accessible to third-party providers. On the other hand, on-premises threat modeling tools are installed and operated within an organization's own IT environment, offering greater control over data security and compliance. This model is often preferred by large enterprises with stringent regulatory requirements or those handling highly sensitive data. On-premises solutions allow organizations to tailor their security measures to their specific needs and integrate them seamlessly with existing systems. However, they require significant upfront investment in hardware and ongoing maintenance, which can be a barrier for smaller organizations. Despite these challenges, on-premises solutions offer unparalleled control and customization, making them a popular choice for businesses with complex security needs. As the global market for threat modeling tools continues to grow, organizations must carefully evaluate their specific requirements and resources to choose the deployment model that best aligns with their security strategy. Both cloud and on-premises solutions have their unique strengths, and the choice between them often depends on factors such as budget, regulatory requirements, and the nature of the data being protected. Ultimately, the decision should be guided by a comprehensive understanding of the organization's security needs and the potential risks associated with each deployment model.

SMEs, Large Enterprises in the Threat Modeling Tool - Global Market:

The usage of threat modeling tools in small and medium-sized enterprises (SMEs) and large enterprises varies significantly due to differences in resources, regulatory requirements, and security needs. For SMEs, threat modeling tools provide a cost-effective way to enhance their cybersecurity posture without the need for extensive IT infrastructure. These tools help SMEs identify potential vulnerabilities and prioritize security measures, allowing them to allocate their limited resources more effectively. By integrating threat modeling into their development processes, SMEs can design more secure systems and reduce the risk of costly data breaches. Cloud-based solutions are particularly popular among SMEs due to their scalability and lower upfront costs, enabling these organizations to access advanced security features without significant investment. In contrast, large enterprises often have more complex security needs and regulatory requirements, necessitating a more comprehensive approach to threat modeling. These organizations typically handle vast amounts of sensitive data and must comply with stringent industry regulations, making robust security measures a top priority. Threat modeling tools help large enterprises identify and mitigate potential threats across their extensive IT environments, ensuring compliance and protecting valuable assets. On-premises solutions are often preferred by large enterprises due to the greater control they offer over data security and customization. These organizations have the resources to invest in the necessary infrastructure and maintenance, allowing them to tailor their security measures to their specific needs. However, cloud-based solutions are also gaining traction among large enterprises, particularly those looking to leverage the flexibility and scalability of the cloud to enhance their security posture. Regardless of the deployment model, threat modeling tools play a crucial role in helping both SMEs and large enterprises protect their digital assets and maintain customer trust in an increasingly digital world. By proactively identifying and addressing potential threats, organizations can reduce the risk of data breaches and ensure the security of their systems and data.

Threat Modeling Tool - Global Market Outlook:

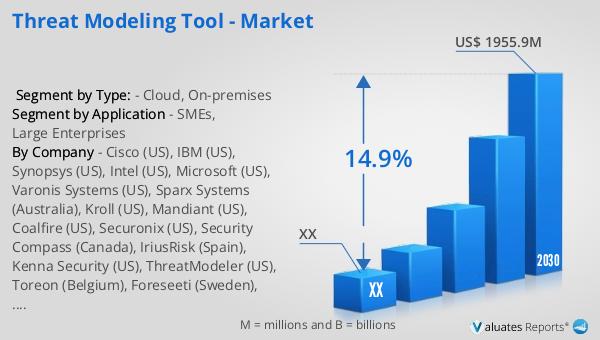

In 2023, the global market for Threat Modeling Tools was valued at approximately $800 million. This market is projected to grow significantly, reaching an estimated size of $1,955.9 million by 2030. This growth represents a compound annual growth rate (CAGR) of 14.9% over the forecast period from 2024 to 2030. The North American segment of this market also shows promising growth potential. Although specific figures for the North American market in 2023 and 2030 are not provided, it is expected to follow a similar upward trajectory during the same forecast period. The increasing demand for robust cybersecurity measures across various industries is a key driver of this growth. As organizations continue to digitize their operations and face increasingly sophisticated cyber threats, the need for advanced threat modeling tools is becoming more critical. These tools help organizations identify potential vulnerabilities and design more secure systems, making them an essential component of modern cybersecurity strategies. The projected growth of the global threat modeling tool market reflects the increasing importance of proactive security measures in protecting digital assets and maintaining customer trust. As the market continues to expand, organizations must stay informed about the latest developments and trends to effectively leverage these tools in their security strategies.

| Report Metric | Details |

| Report Name | Threat Modeling Tool - Market |

| Forecasted market size in 2030 | US$ 1955.9 million |

| CAGR | 14.9% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Cisco (US), IBM (US), Synopsys (US), Intel (US), Microsoft (US), Varonis Systems (US), Sparx Systems (Australia), Kroll (US), Mandiant (US), Coalfire (US), Securonix (US), Security Compass (Canada), IriusRisk (Spain), Kenna Security (US), ThreatModeler (US), Toreon (Belgium), Foreseeti (Sweden), Tutamantic (UK), Cymune (India), Avocado Systems (US), Secura (Netherlands), qSEAp (India), VerSprite (Georgia), IMQ Minded Security (taly) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |