What is Global 6-Axis Robotic Precision Positioning System Market?

The Global 6-Axis Robotic Precision Positioning System Market is a specialized segment within the broader robotics industry, focusing on systems that offer high precision and flexibility in positioning tasks. These systems are equipped with six axes, allowing for complex movements and rotations, which are essential in various high-tech applications. The market for these systems is driven by the increasing demand for automation and precision in industries such as aerospace, electronics, and manufacturing. These systems are crucial for tasks that require meticulous accuracy, such as assembling intricate components, conducting detailed inspections, and performing delicate operations. The versatility of 6-axis robotic systems makes them suitable for a wide range of applications, from industrial manufacturing to scientific research. As industries continue to seek ways to enhance efficiency and reduce human error, the demand for advanced robotic systems like these is expected to grow. The market is characterized by continuous technological advancements, with manufacturers focusing on improving the speed, accuracy, and adaptability of these systems to meet the evolving needs of various sectors. Overall, the Global 6-Axis Robotic Precision Positioning System Market represents a dynamic and rapidly evolving field with significant potential for growth and innovation.

Below 300 mm, 300mm-600mm, Above 600 mm in the Global 6-Axis Robotic Precision Positioning System Market:

In the Global 6-Axis Robotic Precision Positioning System Market, the systems are categorized based on their reach and size, which are typically defined by the length of their arms. The categories include Below 300 mm, 300 mm-600 mm, and Above 600 mm. Each category serves different industrial needs and applications. Systems with a reach Below 300 mm are often used in environments where space is limited, and tasks require high precision over short distances. These compact systems are ideal for small-scale assembly lines, intricate component handling, and precision tasks in electronics manufacturing. Their small size allows them to fit into tight spaces, making them highly versatile for applications where larger systems would be impractical. On the other hand, systems with a reach of 300 mm-600 mm offer a balance between size and reach, making them suitable for medium-sized operations. These systems are commonly used in automotive manufacturing, where they can handle tasks such as welding, painting, and assembly with high precision. Their moderate size allows them to perform a variety of tasks without taking up excessive space, making them a popular choice for many industries. Finally, systems with a reach Above 600 mm are designed for large-scale operations that require extensive reach and flexibility. These systems are often used in heavy industries such as aerospace and shipbuilding, where they can handle large components and perform complex tasks over a wide area. Their extended reach and robust design make them ideal for applications that require both strength and precision. Each category of the 6-axis robotic systems is designed to meet specific industrial needs, offering a range of options for businesses looking to enhance their automation capabilities. As industries continue to evolve and demand more sophisticated solutions, the diversity in the size and reach of these systems ensures that there is a suitable option for virtually any application. The ability to choose a system based on reach and size allows businesses to tailor their automation solutions to their specific requirements, optimizing efficiency and productivity. This categorization also highlights the adaptability of the 6-axis robotic systems, as they can be customized to fit the unique needs of different industries and applications. Whether it's a compact system for a small electronics workshop or a large-scale system for an aerospace manufacturing plant, the Global 6-Axis Robotic Precision Positioning System Market offers a wide range of options to meet the diverse needs of modern industries.

Aerospace, Satellite Sensor Test, Optical Wafer Inspection, Others in the Global 6-Axis Robotic Precision Positioning System Market:

The Global 6-Axis Robotic Precision Positioning System Market finds extensive usage across various high-tech industries, including aerospace, satellite sensor testing, optical wafer inspection, and others. In the aerospace sector, these systems are indispensable for tasks that require extreme precision and reliability. They are used in the assembly of aircraft components, where accuracy is crucial to ensure the safety and performance of the final product. The ability of these systems to perform complex movements and handle delicate components makes them ideal for the aerospace industry, where even the smallest error can have significant consequences. In satellite sensor testing, 6-axis robotic systems play a critical role in ensuring the accuracy and functionality of sensors before they are deployed into space. These systems can simulate the conditions that sensors will face in space, allowing for thorough testing and validation. The precision and flexibility of 6-axis systems make them well-suited for this application, as they can replicate the complex movements and orientations that sensors will encounter in orbit. Optical wafer inspection is another area where these systems are widely used. In the semiconductor industry, the production of wafers requires meticulous inspection to ensure quality and performance. 6-axis robotic systems are used to handle and inspect wafers with high precision, identifying defects and ensuring that only the highest quality products are produced. The ability to perform detailed inspections with minimal human intervention helps to improve efficiency and reduce the risk of errors. Beyond these specific applications, 6-axis robotic systems are also used in a variety of other industries, including automotive, electronics, and healthcare. In the automotive industry, they are used for tasks such as welding, painting, and assembly, where precision and consistency are essential. In electronics manufacturing, they are used for assembling and testing components, where their ability to handle small and delicate parts is invaluable. In healthcare, these systems are used in surgical procedures and laboratory automation, where their precision and reliability can significantly enhance outcomes. The versatility and adaptability of 6-axis robotic systems make them a valuable tool in a wide range of applications, helping industries to improve efficiency, reduce costs, and enhance the quality of their products and services. As technology continues to advance, the potential applications for these systems are likely to expand, offering even more opportunities for innovation and growth.

Global 6-Axis Robotic Precision Positioning System Market Outlook:

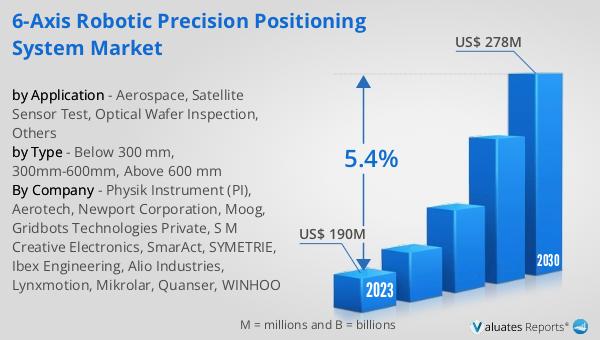

The outlook for the Global 6-Axis Robotic Precision Positioning System Market is promising, with significant growth anticipated in the coming years. In 2023, the market was valued at approximately US$ 190 million, reflecting the increasing demand for precision and automation across various industries. By 2030, the market is expected to reach around US$ 278 million, driven by a compound annual growth rate (CAGR) of 5.4% from 2024 to 2030. This growth is indicative of the expanding applications and technological advancements in the field of robotics. The increasing adoption of 6-axis robotic systems in industries such as aerospace, electronics, and manufacturing is a key factor contributing to this growth. As businesses continue to seek ways to enhance efficiency and reduce human error, the demand for advanced robotic systems is expected to rise. The market's growth is also supported by continuous innovations in robotics technology, which are improving the speed, accuracy, and adaptability of these systems. Manufacturers are focusing on developing more sophisticated and versatile systems to meet the evolving needs of various sectors. The projected growth of the Global 6-Axis Robotic Precision Positioning System Market underscores the importance of these systems in modern industries and highlights the potential for further advancements and applications in the future.

| Report Metric | Details |

| Report Name | 6-Axis Robotic Precision Positioning System Market |

| Accounted market size in 2023 | US$ 190 million |

| Forecasted market size in 2030 | US$ 278 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Physik Instrument (PI), Aerotech, Newport Corporation, Moog, Gridbots Technologies Private, S M Creative Electronics, SmarAct, SYMETRIE, Ibex Engineering, Alio Industries, Lynxmotion, Mikrolar, Quanser, WINHOO |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |