What is Aerial Work Platforms - Global Market?

Aerial Work Platforms (AWPs) are specialized mechanical devices designed to provide temporary access to elevated areas for people or equipment. These platforms are crucial in various industries, including construction, maintenance, and emergency services, where reaching high places safely and efficiently is essential. The global market for AWPs has been expanding steadily due to the increasing demand for infrastructure development and maintenance activities worldwide. AWPs come in various types, such as scissor lifts, boom lifts, and other specialized platforms, each catering to specific needs and height requirements. The versatility and safety features of these platforms make them indispensable tools in modern construction and maintenance projects. As urbanization and industrialization continue to rise, the demand for AWPs is expected to grow, driven by the need for efficient and safe access solutions in high-rise buildings, bridges, and other structures. The market's growth is also supported by technological advancements, which have led to the development of more efficient and environmentally friendly platforms. Overall, the AWP market is poised for significant growth as industries continue to prioritize safety and efficiency in their operations.

Scissor Lifts (up to 30’, 30’ – 50’, and more than 50’), Boom Lifts (up to 60’, 60’ – 100’, and more than 100’), Other AWPs in the Aerial Work Platforms - Global Market:

Scissor lifts are a type of Aerial Work Platform characterized by their crisscrossing support structure, which extends vertically to provide access to elevated areas. These lifts are categorized based on their height capabilities: up to 30 feet, 30 to 50 feet, and more than 50 feet. Scissor lifts are widely used in construction, maintenance, and warehousing due to their stability and ability to lift heavy loads. The compact design of scissor lifts makes them ideal for indoor use, where space is often limited. Boom lifts, on the other hand, offer greater flexibility with their extendable arms, allowing for both vertical and horizontal reach. They are categorized into three height ranges: up to 60 feet, 60 to 100 feet, and more than 100 feet. Boom lifts are particularly useful in situations where obstacles need to be navigated, such as in tree trimming or electrical line maintenance. Their ability to reach over and around obstacles makes them a preferred choice for outdoor applications. Other types of AWPs include vertical mast lifts and personal lifts, which are designed for specific tasks and environments. Vertical mast lifts are compact and lightweight, making them suitable for indoor maintenance tasks in tight spaces. Personal lifts are smaller, portable platforms designed for single-person use, often used in retail or small-scale maintenance tasks. The global market for AWPs is driven by the need for efficient and safe access solutions in various industries. As safety regulations become more stringent, the demand for reliable and versatile AWPs continues to grow. Manufacturers are constantly innovating to improve the safety, efficiency, and environmental impact of these platforms. For instance, electric-powered AWPs are becoming increasingly popular due to their lower emissions and quieter operation, making them suitable for indoor use. The market is also seeing a trend towards the integration of advanced technologies, such as telematics and automation, to enhance the functionality and safety of AWPs. These advancements allow for real-time monitoring of equipment performance and maintenance needs, reducing downtime and improving overall efficiency. As the global economy continues to recover and infrastructure projects resume, the demand for AWPs is expected to rise. The construction industry, in particular, is a major driver of AWP demand, as new buildings and infrastructure require safe and efficient access solutions. Additionally, the growing emphasis on worker safety and the need to comply with stringent safety regulations are further propelling the market's growth. In summary, the global market for Aerial Work Platforms is characterized by a diverse range of products designed to meet the specific needs of various industries. The continued focus on safety, efficiency, and technological innovation is expected to drive the market's growth in the coming years.

AWP Rental Service Providers, Commercial, Manufacturing, Others (Public Administration, Mining, Agriculture etc.) in the Aerial Work Platforms - Global Market:

Aerial Work Platforms are extensively used across various sectors, each with unique requirements and applications. AWP rental service providers play a crucial role in the market by offering flexible access to these platforms without the need for significant capital investment. Renting AWPs allows businesses to access the latest technology and equipment tailored to their specific needs, without the burden of ownership and maintenance costs. This is particularly beneficial for companies with fluctuating demand or short-term projects, as they can scale their equipment needs up or down as required. In the commercial sector, AWPs are indispensable tools for tasks such as building maintenance, window cleaning, and installation of signage or lighting. The ability to safely reach high places is essential in maintaining the aesthetic and functional aspects of commercial properties. AWPs provide a safe and efficient solution for these tasks, reducing the risk of accidents and improving productivity. In the manufacturing industry, AWPs are used for maintenance and repair of machinery, installation of equipment, and facility management. The ability to access high and hard-to-reach areas is crucial in ensuring the smooth operation of manufacturing processes. AWPs offer a safe and efficient means of performing these tasks, minimizing downtime and maintaining productivity. Other sectors, such as public administration, mining, and agriculture, also benefit from the use of AWPs. In public administration, AWPs are used for tasks such as streetlight maintenance, tree trimming, and infrastructure inspection. The ability to safely access elevated areas is essential in maintaining public safety and infrastructure integrity. In the mining industry, AWPs are used for equipment maintenance and inspection, providing a safe and efficient means of accessing high and hard-to-reach areas. In agriculture, AWPs are used for tasks such as orchard maintenance and crop inspection, providing a safe and efficient means of accessing elevated areas. Overall, the versatility and safety features of AWPs make them indispensable tools across various sectors. The ability to safely and efficiently access elevated areas is crucial in maintaining productivity and safety in these industries. As safety regulations become more stringent and the demand for efficient access solutions continues to grow, the use of AWPs is expected to increase across various sectors.

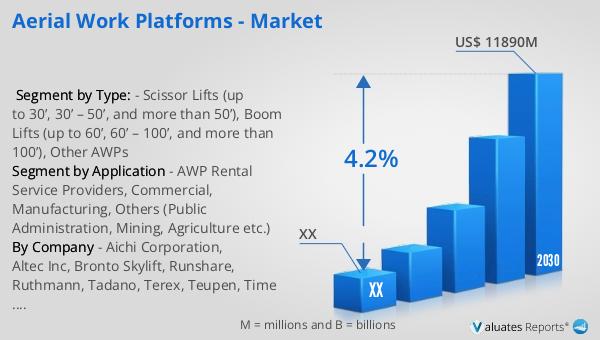

Aerial Work Platforms - Global Market Outlook:

The global market for Aerial Work Platforms was valued at approximately $8,858.5 million in 2023. It is projected to grow to a revised size of around $11,890 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.2% over the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for safe and efficient access solutions across various industries. The market is characterized by a high level of competition, with the top three players accounting for about 50% of the global market share. This concentration of market power highlights the importance of innovation and differentiation in maintaining a competitive edge. Companies in the AWP market are continually investing in research and development to enhance the safety, efficiency, and environmental impact of their products. The integration of advanced technologies, such as telematics and automation, is becoming increasingly important in meeting the evolving needs of customers. These technologies enable real-time monitoring of equipment performance and maintenance needs, reducing downtime and improving overall efficiency. As the global economy continues to recover and infrastructure projects resume, the demand for AWPs is expected to rise. The construction industry, in particular, is a major driver of AWP demand, as new buildings and infrastructure require safe and efficient access solutions. Additionally, the growing emphasis on worker safety and the need to comply with stringent safety regulations are further propelling the market's growth. In summary, the global market for Aerial Work Platforms is poised for significant growth, driven by the increasing demand for safe and efficient access solutions across various industries. The continued focus on safety, efficiency, and technological innovation is expected to drive the market's growth in the coming years.

| Report Metric | Details |

| Report Name | Aerial Work Platforms - Market |

| Forecasted market size in 2030 | US$ 11890 million |

| CAGR | 4.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Aichi Corporation, Altec Inc, Bronto Skylift, Runshare, Ruthmann, Tadano, Terex, Teupen, Time Benelux |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |