What is Track Geometry Measurement System (TGMS) - Global Market?

Track Geometry Measurement System (TGMS) is a crucial technology in the railway industry, designed to ensure the safety and efficiency of train operations by monitoring and maintaining the condition of railway tracks. These systems are employed to measure various parameters of the track, such as alignment, gauge, elevation, and curvature, which are essential for the smooth and safe operation of trains. The global market for TGMS is driven by the increasing demand for efficient and safe railway networks, especially in regions with extensive rail infrastructure. As railways continue to be a vital mode of transportation for both passengers and freight, the need for regular track maintenance and monitoring becomes paramount. TGMS provides real-time data and analytics, enabling railway operators to identify potential issues before they escalate into major problems, thereby reducing the risk of accidents and improving overall operational efficiency. The adoption of TGMS is further fueled by advancements in technology, which have made these systems more accurate, reliable, and cost-effective. As a result, the global market for TGMS is expected to witness significant growth in the coming years, with increasing investments in railway infrastructure and the modernization of existing rail networks.

No Contact Based Track Geometry Measurement System(TGMS), Contact Based Track Geometry Measurement System(TGMS) in the Track Geometry Measurement System (TGMS) - Global Market:

In the realm of Track Geometry Measurement Systems (TGMS), there are two primary types: No Contact Based TGMS and Contact Based TGMS. No Contact Based TGMS utilizes advanced technologies such as lasers, cameras, and sensors to measure track geometry without physically touching the tracks. This method offers several advantages, including high-speed data collection, minimal disruption to train operations, and the ability to measure tracks in challenging environments. The non-contact approach is particularly beneficial for high-speed railways, where traditional contact-based methods may not be feasible due to the speed and frequency of train operations. On the other hand, Contact Based TGMS involves physical contact with the tracks, typically using mechanical devices or sensors mounted on a rail vehicle. This method provides direct measurements of track parameters and is often used in scenarios where high precision is required. While contact-based systems may be slower and more intrusive compared to their non-contact counterparts, they offer a level of accuracy and reliability that is essential for certain applications, such as heavy haul railways where the tracks are subjected to significant stress and wear. Both types of TGMS play a vital role in ensuring the safety and efficiency of railway operations, with each offering unique benefits and challenges. The choice between contact and non-contact systems often depends on the specific requirements of the railway network, including factors such as speed, frequency of use, and environmental conditions. As technology continues to evolve, we can expect further innovations in both contact and non-contact TGMS, enhancing their capabilities and expanding their applications in the global railway industry.

High-Speed Railways, Mass Transit Railways, Heavy Haul Railways, Light Railways in the Track Geometry Measurement System (TGMS) - Global Market:

The usage of Track Geometry Measurement Systems (TGMS) varies across different types of railways, each with its unique requirements and challenges. In high-speed railways, TGMS is essential for maintaining the precise alignment and smoothness of tracks, which are critical for the safe and efficient operation of trains traveling at high speeds. The non-contact based TGMS is particularly advantageous in this context, as it allows for rapid data collection without disrupting train operations. By continuously monitoring track conditions, railway operators can quickly identify and address any issues, minimizing the risk of accidents and ensuring a comfortable ride for passengers. In mass transit railways, such as subways and commuter trains, TGMS plays a crucial role in maintaining the reliability and safety of the network. Given the high frequency of train operations and the dense urban environments in which these systems operate, regular track maintenance and monitoring are essential. TGMS provides real-time data on track conditions, enabling operators to schedule maintenance activities efficiently and reduce downtime. For heavy haul railways, which are often used for transporting large volumes of freight over long distances, TGMS is vital for ensuring the durability and stability of the tracks. The contact-based TGMS is commonly used in this context, as it provides accurate measurements of track parameters that are critical for handling the heavy loads and stresses associated with freight transport. Finally, in light railways, which are typically used for short-distance urban transit, TGMS helps maintain the smooth operation of the network by monitoring track conditions and identifying potential issues before they impact service. Overall, TGMS is an indispensable tool for railway operators, providing the data and insights needed to maintain safe, efficient, and reliable rail networks across various types of railways.

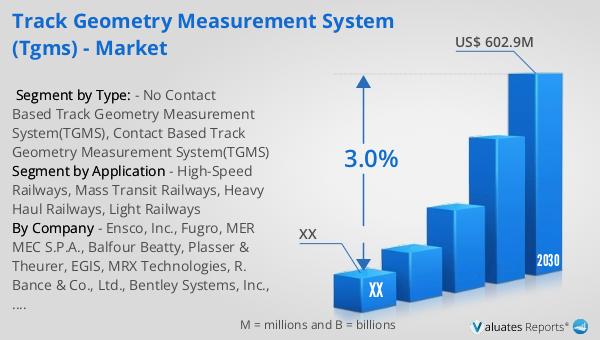

Track Geometry Measurement System (TGMS) - Global Market Outlook:

The global market for Track Geometry Measurement Systems (TGMS) was valued at approximately USD 488.4 million in 2023. It is projected to grow to a revised size of USD 602.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.0% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for efficient and safe railway networks, as well as advancements in TGMS technology that have made these systems more accurate and cost-effective. Major players in the TGMS market include Amberg Technologies, Trimble Railway GmbH, and Ensco, with the top three companies accounting for about 33% of the market share. These companies are at the forefront of innovation in TGMS, developing new technologies and solutions to meet the evolving needs of the railway industry. As the market continues to grow, we can expect increased competition and further advancements in TGMS technology, which will drive improvements in railway safety and efficiency worldwide. The ongoing investments in railway infrastructure and the modernization of existing rail networks are also expected to contribute to the growth of the TGMS market, as operators seek to enhance the safety and reliability of their services.

| Report Metric | Details |

| Report Name | Track Geometry Measurement System (TGMS) - Market |

| Forecasted market size in 2030 | US$ 602.9 million |

| CAGR | 3.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Ensco, Inc., Fugro, MER MEC S.P.A., Balfour Beatty, Plasser & Theurer, EGIS, MRX Technologies, R. Bance & Co., Ltd., Bentley Systems, Inc., Goldschmidt Thermit Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |