What is Global Fluoride Dental Consumables Market?

The Global Fluoride Dental Consumables Market refers to the industry focused on products that contain fluoride and are used in dental care to prevent tooth decay and enhance oral health. Fluoride is a naturally occurring mineral known for its ability to strengthen tooth enamel and make teeth more resistant to decay. The market includes a variety of products such as fluoride varnishes, rinses, gels, and other dental care items that are used by dental professionals and consumers alike. These products are essential in both preventive and therapeutic dental care, helping to reduce the incidence of cavities and other dental issues. The market is driven by increasing awareness about oral health, advancements in dental care technologies, and the rising prevalence of dental problems across the globe. As more people seek effective ways to maintain their oral hygiene, the demand for fluoride dental consumables continues to grow, making it a significant segment within the broader dental care industry. The market is also influenced by regulatory guidelines and recommendations from health organizations that advocate for the use of fluoride in dental care products to promote better oral health outcomes.

Varnish, Rinsing, Topical Gel, Others in the Global Fluoride Dental Consumables Market:

In the Global Fluoride Dental Consumables Market, several key products play a crucial role in dental care, including varnishes, rinses, topical gels, and others. Fluoride varnish is a highly concentrated form of fluoride that is applied to the tooth's surface by dental professionals. It is used primarily for its ability to adhere to the teeth for an extended period, allowing fluoride to be absorbed into the enamel and providing long-lasting protection against decay. This product is particularly beneficial for children and individuals at high risk of cavities, as it can significantly reduce the incidence of dental caries. Fluoride rinses, on the other hand, are liquid solutions that can be used by individuals at home as part of their daily oral hygiene routine. These rinses help to wash away food particles and bacteria while delivering fluoride to the teeth, offering an easy and effective way to maintain oral health. They are especially useful for people who have braces or other dental appliances that make brushing and flossing challenging. Topical fluoride gels are another important product in this market, often used in dental offices during routine check-ups. These gels are applied directly to the teeth and left in place for a few minutes to allow the fluoride to penetrate the enamel. They are particularly effective for patients with a history of dental decay or those undergoing orthodontic treatment. Other fluoride dental consumables include toothpaste, tablets, and supplements, which provide additional fluoride exposure to help strengthen teeth and prevent cavities. Each of these products serves a unique purpose in dental care, catering to different needs and preferences of consumers and dental professionals. The availability of various fluoride dental consumables allows for personalized oral care regimens, ensuring that individuals can choose the products that best suit their specific dental health requirements. As the market continues to evolve, innovations in product formulations and delivery methods are expected to enhance the effectiveness and convenience of fluoride dental consumables, further driving their adoption in dental care practices worldwide.

Dental Hospitals and Clinics, Dental Academic and Research Institutions, Forensic Laboratory, Others in the Global Fluoride Dental Consumables Market:

The usage of Global Fluoride Dental Consumables Market products spans across various settings, including dental hospitals and clinics, dental academic and research institutions, forensic laboratories, and other areas. In dental hospitals and clinics, fluoride dental consumables are integral to preventive and therapeutic care. Dentists and dental hygienists use fluoride varnishes, gels, and rinses to protect patients' teeth from decay and to treat early signs of cavities. These products are part of routine dental check-ups and cleanings, helping to maintain oral health and prevent more serious dental issues. In dental academic and research institutions, fluoride dental consumables are used for educational and research purposes. Students and researchers study the effects of fluoride on dental health, exploring new formulations and delivery methods to improve the efficacy of these products. This research contributes to the development of innovative dental care solutions and informs best practices in the use of fluoride in dentistry. Forensic laboratories also utilize fluoride dental consumables in their work, particularly in the analysis of dental evidence. Fluoride levels in teeth can provide valuable information in forensic investigations, helping to identify individuals and determine certain aspects of their health history. Other areas where fluoride dental consumables are used include community health programs and public health initiatives aimed at improving oral health outcomes. These programs often provide fluoride treatments to underserved populations, helping to reduce the prevalence of dental caries and promote better oral hygiene practices. The widespread use of fluoride dental consumables in these various settings underscores their importance in maintaining oral health and preventing dental diseases. As awareness of the benefits of fluoride continues to grow, the demand for these products is expected to increase, further solidifying their role in dental care across different sectors.

Global Fluoride Dental Consumables Market Outlook:

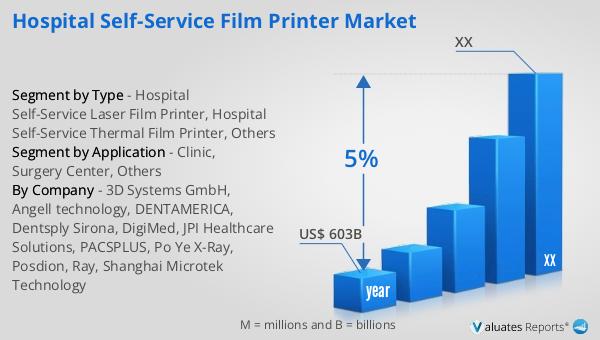

Our research indicates that the global market for medical devices, which includes fluoride dental consumables, is projected to reach approximately $603 billion in 2023. This market is anticipated to expand at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is driven by several factors, including advancements in medical technology, increasing demand for innovative healthcare solutions, and a growing focus on preventive care. The inclusion of fluoride dental consumables within this broader market highlights their significance in the healthcare industry. As dental care becomes an increasingly important aspect of overall health and wellness, the demand for effective and convenient fluoride products is expected to rise. This growth is further supported by the increasing prevalence of dental issues worldwide and the rising awareness of the benefits of fluoride in maintaining oral health. The market's expansion also reflects the ongoing efforts of manufacturers to develop new and improved fluoride dental consumables that cater to the diverse needs of consumers and dental professionals. As the market continues to evolve, it is likely to see further innovations in product formulations and delivery methods, enhancing the effectiveness and accessibility of fluoride dental care solutions. This positive outlook for the Global Fluoride Dental Consumables Market underscores its potential for continued growth and development in the coming years.

| Report Metric | Details |

| Report Name | Fluoride Dental Consumables Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | 3M ESPE, Danaher, Dentatus USA, Dentsply Sirona, GC Corporation, Zimmer Biomet Holdings, Institut Straumann AG, Ivoclar Vivadent, Mitsui Chemicals, Shofu, Ultradent Products, VOCO GmbH, Young Innovations |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |