What is Global Military Communications Systems and Equipment Market?

The Global Military Communications Systems and Equipment Market encompasses a wide range of technologies and devices used by military forces worldwide to ensure secure, reliable, and efficient communication. These systems are crucial for coordinating operations, sharing intelligence, and maintaining situational awareness in various military scenarios. The market includes products such as radios, satellite communication systems, encryption devices, and other communication equipment designed to withstand harsh environments and provide robust performance. The demand for these systems is driven by the need for advanced communication capabilities in modern warfare, where real-time information exchange can significantly impact mission success. As military operations become more complex and geographically dispersed, the importance of reliable communication systems continues to grow, leading to ongoing investments in this market.

Military Satellite Communications, Military Radio Communications in the Global Military Communications Systems and Equipment Market:

Military Satellite Communications (MILSATCOM) and Military Radio Communications are two critical components of the Global Military Communications Systems and Equipment Market. MILSATCOM involves the use of satellites to provide secure and reliable communication links for military forces. These satellites enable long-distance communication, connecting troops in remote locations with command centers and other units. They support various applications, including voice communication, data transfer, and video conferencing, ensuring that military personnel can share information and coordinate actions effectively. MILSATCOM systems are designed to be resilient against jamming and other forms of electronic warfare, providing a dependable communication backbone even in contested environments. On the other hand, Military Radio Communications involve the use of radio frequencies to facilitate communication between military units. These radios are essential for tactical communication on the battlefield, allowing soldiers to communicate with each other and with command centers in real-time. Military radios are designed to be rugged and reliable, capable of operating in extreme conditions and providing secure communication channels. They support various communication modes, including voice, data, and video, and are often equipped with encryption capabilities to protect sensitive information. Both MILSATCOM and Military Radio Communications play a vital role in modern military operations, enabling effective coordination and information sharing across different levels of command. As military forces continue to modernize and adopt new technologies, the demand for advanced communication systems is expected to grow, driving further innovation and development in this market.

Airborne Communications, Maritime Communications, Terrestrial Communications, Others in the Global Military Communications Systems and Equipment Market:

The usage of Global Military Communications Systems and Equipment Market extends across various domains, including Airborne Communications, Maritime Communications, Terrestrial Communications, and others. In Airborne Communications, these systems are used to ensure seamless communication between aircraft, ground control stations, and other airborne assets. This includes communication for command and control, intelligence sharing, and coordination of air operations. Advanced communication systems enable pilots and crew members to receive real-time updates, share mission-critical information, and coordinate with other units, enhancing the overall effectiveness of air missions. In Maritime Communications, military communication systems are used to connect naval vessels, submarines, and shore-based command centers. These systems support various functions, including navigation, surveillance, and coordination of maritime operations. Reliable communication is essential for maintaining situational awareness, coordinating fleet movements, and ensuring the safety of naval personnel. Terrestrial Communications involve the use of communication systems for ground-based military operations. This includes communication between soldiers, vehicles, command posts, and other ground units. These systems enable real-time information exchange, coordination of movements, and effective command and control, which are crucial for the success of ground operations. Other areas where military communication systems are used include space-based operations, cyber warfare, and special operations. In space-based operations, communication systems are used to connect satellites, ground stations, and other space assets, enabling the exchange of information and coordination of space missions. In cyber warfare, secure communication systems are essential for protecting sensitive information and coordinating cyber defense and offense operations. Special operations require highly reliable and secure communication systems to ensure the success of covert missions and the safety of special forces personnel. Overall, the usage of military communication systems across these various domains highlights their importance in modern military operations and underscores the need for continued investment and innovation in this market.

Global Military Communications Systems and Equipment Market Outlook:

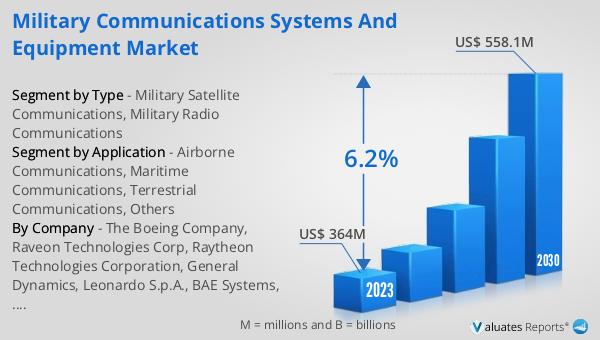

The global Military Communications Systems and Equipment market was valued at US$ 364 million in 2023 and is anticipated to reach US$ 558.1 million by 2030, witnessing a CAGR of 6.2% during the forecast period 2024-2030. This market outlook indicates a significant growth trajectory driven by the increasing demand for advanced communication systems in military operations. The projected growth reflects the ongoing investments in modernizing military communication infrastructure to enhance operational efficiency, situational awareness, and mission success. The market's expansion is also attributed to the rising complexity of military operations, which necessitates robust and reliable communication solutions. As military forces around the world continue to adopt new technologies and upgrade their communication capabilities, the market for military communication systems and equipment is expected to experience sustained growth. This positive outlook underscores the critical role of communication systems in modern warfare and highlights the importance of continued innovation and development in this sector.

| Report Metric | Details |

| Report Name | Military Communications Systems and Equipment Market |

| Accounted market size in 2023 | US$ 364 million |

| Forecasted market size in 2030 | US$ 558.1 million |

| CAGR | 6.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | The Boeing Company, Raveon Technologies Corp, Raytheon Technologies Corporation, General Dynamics, Leonardo S.p.A., BAE Systems, Collins Aerospace, Lockheed Martin, Northrop Grumman, Thales Group, Elbit Systems, Codan Group, L3Harris Technologies Inc., Saab AB, Kongsberg |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |