What is Global Digital Body Fat Scale Market?

The Global Digital Body Fat Scale Market refers to the worldwide industry focused on the production, distribution, and sale of digital scales that measure body fat percentage. These scales use advanced technology to provide users with accurate readings of their body composition, including fat, muscle, water, and bone mass. The market encompasses a variety of products designed for different user needs, from basic models for home use to more sophisticated versions for professional and commercial applications. The increasing awareness of health and fitness, coupled with the growing prevalence of obesity and related health issues, has driven the demand for these scales. Additionally, advancements in technology, such as the integration of Wi-Fi and Bluetooth, have made these devices more user-friendly and efficient, further boosting their popularity. The market is characterized by a diverse range of players, including established brands and new entrants, all competing to offer innovative and reliable products to consumers.

Wi-Fi, Bluetooth in the Global Digital Body Fat Scale Market:

Wi-Fi and Bluetooth technologies play a crucial role in the Global Digital Body Fat Scale Market, enhancing the functionality and user experience of these devices. Wi-Fi-enabled body fat scales allow users to connect their scales to their home networks, enabling seamless data transfer to various health and fitness apps. This connectivity ensures that users can easily track their progress over time, set goals, and receive personalized insights and recommendations. Bluetooth-enabled scales, on the other hand, offer a more direct connection to smartphones and other devices. By pairing the scale with a mobile app via Bluetooth, users can instantly view their measurements and sync data without the need for an internet connection. Both technologies provide a level of convenience and accuracy that traditional scales cannot match. They enable real-time data synchronization, which is particularly beneficial for users who are serious about monitoring their health metrics. Moreover, these connected scales often come with additional features such as multi-user profiles, allowing different family members to track their data separately. The integration of Wi-Fi and Bluetooth also facilitates the use of advanced algorithms and machine learning to provide more accurate and personalized health insights. For instance, some scales can analyze trends and patterns in the data to offer tailored advice on diet and exercise. This level of personalization is a significant selling point for consumers looking to make informed decisions about their health. Furthermore, the ability to share data with healthcare providers or fitness coaches can enhance the overall effectiveness of health and wellness programs. In the commercial sector, Wi-Fi and Bluetooth-enabled body fat scales are invaluable tools for gyms, fitness centers, and medical facilities. They allow for efficient data management and provide a comprehensive view of clients' or patients' health metrics. This data can be used to design customized fitness plans or medical treatments, improving outcomes and client satisfaction. The integration of these technologies also opens up opportunities for remote health monitoring and telehealth services, which have become increasingly important in the wake of the COVID-19 pandemic. Overall, the incorporation of Wi-Fi and Bluetooth technologies in digital body fat scales represents a significant advancement in the market, offering enhanced functionality, convenience, and accuracy for both individual and commercial users.

Home, Commercial, Other in the Global Digital Body Fat Scale Market:

The Global Digital Body Fat Scale Market finds extensive usage across various sectors, including home, commercial, and other specialized areas. In the home setting, digital body fat scales have become an essential tool for individuals and families focused on maintaining a healthy lifestyle. These scales provide users with detailed insights into their body composition, helping them track their fitness progress and make informed decisions about their diet and exercise routines. The convenience of having a digital body fat scale at home allows users to monitor their health metrics regularly without the need for frequent visits to a healthcare provider or fitness center. This regular monitoring can be particularly beneficial for individuals managing chronic conditions such as obesity, diabetes, or cardiovascular diseases, as it enables them to keep a close eye on their health and make necessary adjustments to their lifestyle. In the commercial sector, digital body fat scales are widely used in gyms, fitness centers, and wellness clinics. These facilities rely on accurate body composition measurements to design personalized fitness programs for their clients. By using digital body fat scales, fitness trainers and health professionals can assess the effectiveness of exercise routines and dietary plans, making necessary adjustments to ensure optimal results. The ability to track progress over time also helps in motivating clients, as they can see tangible improvements in their body composition. Additionally, digital body fat scales are used in medical facilities for diagnostic and monitoring purposes. Healthcare providers use these scales to assess patients' body composition as part of routine check-ups or specific medical evaluations. This information is crucial for diagnosing and managing various health conditions, including obesity, malnutrition, and metabolic disorders. In other specialized areas, digital body fat scales are used in research and sports science. Researchers use these scales to study the effects of different interventions on body composition, contributing to the development of new health and fitness strategies. In sports science, athletes and coaches use digital body fat scales to monitor the physical condition of athletes, ensuring they maintain optimal body composition for peak performance. Overall, the versatility and accuracy of digital body fat scales make them valuable tools across various sectors, contributing to improved health and wellness outcomes.

Global Digital Body Fat Scale Market Outlook:

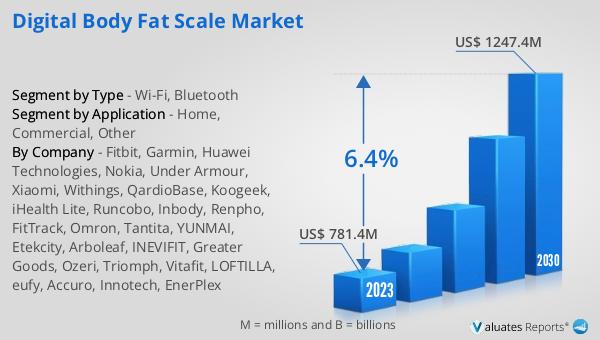

The global Digital Body Fat Scale market was valued at US$ 781.4 million in 2023 and is anticipated to reach US$ 1247.4 million by 2030, witnessing a CAGR of 6.4% during the forecast period 2024-2030. This market outlook indicates a significant growth trajectory for the industry, driven by increasing health awareness and technological advancements. The rising prevalence of obesity and related health issues has led to a growing demand for accurate and reliable body composition measurement tools. Digital body fat scales, with their advanced features and user-friendly interfaces, have become a popular choice among consumers. The integration of Wi-Fi and Bluetooth technologies has further enhanced the functionality of these devices, making them more convenient and efficient for users. The market is characterized by a diverse range of players, including established brands and new entrants, all competing to offer innovative products. This competitive landscape is expected to drive further advancements in the technology and design of digital body fat scales, contributing to the market's growth. Additionally, the increasing adoption of these scales in commercial and medical settings is likely to boost market demand. Overall, the global Digital Body Fat Scale market is poised for substantial growth in the coming years, reflecting the growing emphasis on health and wellness.

| Report Metric | Details |

| Report Name | Digital Body Fat Scale Market |

| Accounted market size in 2023 | US$ 781.4 million |

| Forecasted market size in 2030 | US$ 1247.4 million |

| CAGR | 6.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Fitbit, Garmin, Huawei Technologies, Nokia, Under Armour, Xiaomi, Withings, QardioBase, Koogeek, iHealth Lite, Runcobo, Inbody, Renpho, FitTrack, Omron, Tantita, YUNMAI, Etekcity, Arboleaf, INEVIFIT, Greater Goods, Ozeri, Triomph, Vitafit, LOFTILLA, eufy, Accuro, Innotech, EnerPlex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |