What is Global Educational Pro AV Market?

The Global Educational Pro AV Market refers to the market for professional audio-visual (AV) equipment and solutions specifically designed for educational institutions around the world. This market encompasses a wide range of products and technologies that enhance the learning experience by integrating advanced AV systems into classrooms, lecture halls, and other educational settings. These solutions include interactive displays, projectors, audio systems, control systems, and other AV equipment that facilitate effective communication, collaboration, and engagement among students and educators. The demand for educational Pro AV solutions is driven by the increasing adoption of digital learning tools, the need for interactive and immersive learning environments, and the growing emphasis on enhancing the quality of education through technology. As educational institutions continue to invest in modernizing their infrastructure and improving the learning experience, the Global Educational Pro AV Market is expected to witness significant growth in the coming years.

PC Workstations and Monitors, Projectors, Projection Screens, Document Cameras, Audio Systems and Speakers, Control Systems, Others in the Global Educational Pro AV Market:

PC workstations and monitors are essential components of the Global Educational Pro AV Market, providing the necessary computing power and display capabilities for various educational applications. These workstations are used by educators and students for tasks such as research, content creation, and interactive learning. High-resolution monitors ensure clear and detailed visuals, enhancing the overall learning experience. Projectors and projection screens are widely used in classrooms and lecture halls to display large-scale visuals, making it easier for students to view presentations, videos, and other educational content. Document cameras, also known as visualizers, are used to display documents, books, and other physical objects on a screen, allowing educators to share detailed information with the entire class. Audio systems and speakers play a crucial role in ensuring clear and audible communication in educational settings. These systems include microphones, amplifiers, and speakers that enhance the audio quality of lectures, presentations, and other educational activities. Control systems are used to manage and integrate various AV components, allowing educators to easily control and switch between different AV sources. These systems provide a seamless and user-friendly interface for managing AV equipment, ensuring a smooth and efficient learning experience. Other AV solutions in the Global Educational Pro AV Market include interactive whiteboards, digital signage, and video conferencing systems. Interactive whiteboards enable collaborative learning by allowing students and educators to interact with digital content using touch or stylus input. Digital signage is used to display important information, announcements, and schedules in educational institutions. Video conferencing systems facilitate remote learning and virtual collaboration, enabling students and educators to connect and interact from different locations. Overall, the Global Educational Pro AV Market offers a wide range of solutions that enhance the learning experience by integrating advanced AV technologies into educational environments.

Universities, Colleges in the Global Educational Pro AV Market:

In universities, the usage of Global Educational Pro AV Market solutions is extensive and varied. Lecture halls and classrooms are equipped with advanced AV systems, including projectors, interactive displays, and audio systems, to facilitate effective teaching and learning. Professors use these technologies to deliver engaging lectures, present multimedia content, and conduct interactive sessions with students. Document cameras are used to display detailed information, such as diagrams and text, on large screens, making it easier for students to follow along. Control systems allow professors to seamlessly switch between different AV sources, ensuring a smooth and efficient lecture experience. In addition to traditional classrooms, universities also use Pro AV solutions in specialized learning environments, such as laboratories, libraries, and research centers. These environments require advanced AV equipment to support various educational activities, including experiments, presentations, and collaborative projects. Video conferencing systems are widely used in universities to facilitate remote learning and virtual collaboration. These systems enable students and educators to connect and interact with peers and experts from different locations, enhancing the learning experience and providing access to a wider range of resources. Digital signage is used throughout university campuses to display important information, announcements, and schedules, ensuring that students and staff are well-informed. In colleges, the usage of Global Educational Pro AV Market solutions is similar to that in universities, with a focus on enhancing the learning experience through advanced AV technologies. Classrooms and lecture halls are equipped with projectors, interactive displays, and audio systems to support effective teaching and learning. Professors use these technologies to deliver engaging lectures, present multimedia content, and conduct interactive sessions with students. Document cameras are used to display detailed information on large screens, making it easier for students to follow along. Control systems allow professors to seamlessly switch between different AV sources, ensuring a smooth and efficient lecture experience. Colleges also use Pro AV solutions in specialized learning environments, such as laboratories, libraries, and research centers, to support various educational activities. Video conferencing systems are widely used to facilitate remote learning and virtual collaboration, enabling students and educators to connect and interact with peers and experts from different locations. Digital signage is used throughout college campuses to display important information, announcements, and schedules, ensuring that students and staff are well-informed. Overall, the usage of Global Educational Pro AV Market solutions in universities and colleges plays a crucial role in enhancing the learning experience by integrating advanced AV technologies into educational environments.

Global Educational Pro AV Market Outlook:

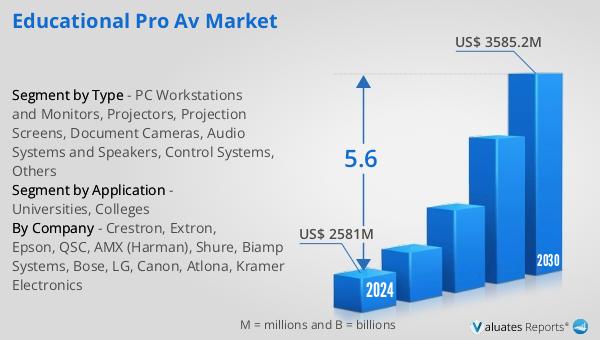

The global Educational Pro AV market is anticipated to expand from US$ 2581 million in 2024 to US$ 3585.2 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 5.6% over the forecast period. In the United States, key players in the educational Pro AV sector include Crestron, Extron, Epson, and QSC, with the top four companies collectively holding approximately 20% of the market share. Crestron stands out as the largest producer, commanding an 11% share. When it comes to product types, PC workstations and monitors represent the largest segment, accounting for about 42% of the market. In terms of application, universities dominate the market with a substantial 62% share. This data underscores the significant role that advanced AV technologies play in enhancing educational environments, particularly in higher education institutions.

| Report Metric | Details |

| Report Name | Educational Pro AV Market |

| Accounted market size in 2024 | US$ 2581 million |

| Forecasted market size in 2030 | US$ 3585.2 million |

| CAGR | 5.6 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Crestron, Extron, Epson, QSC, AMX (Harman), Shure, Biamp Systems, Bose, LG, Canon, Atlona, Kramer Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |