What is Global Medical Image Sharing Software Market?

The Global Medical Image Sharing Software Market refers to the industry focused on the development, distribution, and utilization of software solutions that enable the sharing and exchange of medical images across various healthcare settings. These software solutions facilitate the seamless transfer of medical images such as X-rays, MRIs, CT scans, and ultrasounds between healthcare providers, specialists, and patients. The primary goal is to enhance the efficiency and accuracy of medical diagnoses, treatment planning, and patient care by ensuring that critical imaging data is readily accessible to authorized personnel regardless of their location. This market is driven by the increasing demand for advanced healthcare IT solutions, the need for improved patient outcomes, and the growing adoption of digital health technologies. Additionally, the rising prevalence of chronic diseases and the need for timely and accurate medical imaging further propel the demand for medical image sharing software. The market encompasses a wide range of software solutions, including cloud-based and on-premises systems, each offering unique benefits and features tailored to the specific needs of healthcare providers.

Cloud Based, On-premises in the Global Medical Image Sharing Software Market:

Cloud-based and on-premises solutions are two primary deployment models in the Global Medical Image Sharing Software Market, each offering distinct advantages and considerations for healthcare providers. Cloud-based medical image sharing software is hosted on remote servers and accessed via the internet, providing several benefits such as scalability, cost-effectiveness, and ease of access. These solutions allow healthcare providers to store and share medical images without the need for significant upfront investments in hardware and infrastructure. Cloud-based systems also offer enhanced data security through advanced encryption and compliance with regulatory standards such as HIPAA. Additionally, they enable seamless collaboration among healthcare professionals by providing real-time access to medical images from any location with an internet connection. This is particularly beneficial for telemedicine and remote consultations, where timely access to imaging data is crucial. On the other hand, on-premises medical image sharing software is installed and operated on local servers within a healthcare facility. This deployment model offers greater control over data management and security, as healthcare providers have direct oversight of their IT infrastructure. On-premises solutions are often preferred by larger healthcare organizations with the resources to maintain and manage their own servers. They provide faster access to medical images since data retrieval does not depend on internet connectivity. However, on-premises systems require significant initial investments in hardware, software, and IT personnel for maintenance and updates. They may also pose challenges in terms of scalability, as expanding storage capacity or adding new features often involves additional costs and infrastructure upgrades. Despite these differences, both cloud-based and on-premises solutions aim to improve the efficiency and accuracy of medical image sharing, ultimately enhancing patient care. The choice between the two deployment models depends on various factors, including the size and resources of the healthcare organization, specific use cases, and regulatory requirements. As the healthcare industry continues to evolve, many providers are adopting hybrid approaches that combine the benefits of both cloud-based and on-premises solutions to meet their diverse needs.

Hospital, Clinic, Image Center, Other in the Global Medical Image Sharing Software Market:

The usage of Global Medical Image Sharing Software Market spans across various healthcare settings, including hospitals, clinics, imaging centers, and other medical facilities. In hospitals, medical image sharing software plays a crucial role in streamlining the workflow of radiologists, physicians, and other healthcare professionals. It enables the efficient sharing of imaging data between departments, facilitating timely diagnoses and treatment planning. For instance, a radiologist can quickly share an MRI scan with a neurologist for consultation, leading to faster decision-making and improved patient outcomes. Additionally, hospitals often deal with a high volume of medical images, making the scalability and storage capabilities of these software solutions essential. In clinics, medical image sharing software enhances the ability of healthcare providers to collaborate with specialists and other clinics. This is particularly important in cases where patients require referrals to specialists or second opinions. The software allows for the secure and efficient transfer of imaging data, ensuring that specialists have access to the necessary information to provide accurate diagnoses and treatment recommendations. Imaging centers, which primarily focus on diagnostic imaging services, benefit significantly from medical image sharing software. These centers often work with multiple healthcare providers and need to share imaging data with referring physicians promptly. The software facilitates the seamless transfer of images, reducing the turnaround time for reports and improving patient satisfaction. Additionally, imaging centers can leverage cloud-based solutions to manage large volumes of imaging data without the need for extensive on-site storage infrastructure. Other medical facilities, such as outpatient surgery centers and specialized treatment centers, also utilize medical image sharing software to enhance their operations. For example, outpatient surgery centers can use the software to share pre-operative and post-operative imaging data with surgeons and other healthcare providers, ensuring comprehensive patient care. Specialized treatment centers, such as oncology centers, can benefit from the software by enabling multidisciplinary teams to collaborate on treatment plans based on shared imaging data. Overall, the usage of medical image sharing software across these various healthcare settings leads to improved efficiency, better collaboration among healthcare professionals, and enhanced patient care.

Global Medical Image Sharing Software Market Outlook:

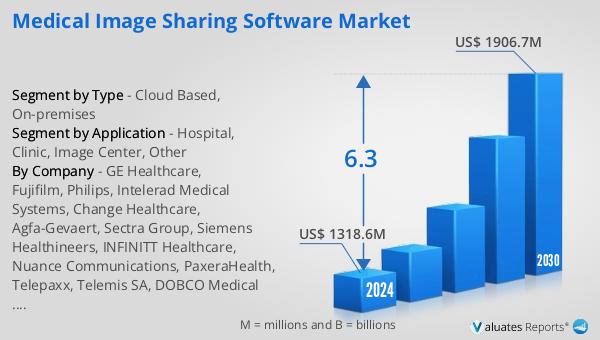

The global Medical Image Sharing Software market is anticipated to expand from US$ 1318.6 million in 2024 to US$ 1906.7 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 6.3% during the forecast period. Key players in this market include GE Healthcare, Fujifilm, Philips, Intelerad Medical Systems, Change Healthcare, and Agfa-Gevaert, with the top five companies collectively holding approximately 63% of the market share. GE Healthcare stands out as the largest producer, commanding a 14% share. In terms of product types, cloud-based solutions dominate the market, accounting for about 67% of the total share. When it comes to applications, hospitals represent the largest segment, making up approximately 59% of the market. These statistics highlight the significant role that cloud-based solutions and hospital applications play in driving the growth and adoption of medical image sharing software globally. The increasing demand for efficient and secure ways to share medical images is propelling the market forward, with major industry players continuously innovating to meet the evolving needs of healthcare providers.

| Report Metric | Details |

| Report Name | Medical Image Sharing Software Market |

| Accounted market size in 2024 | US$ 1318.6 million |

| Forecasted market size in 2030 | US$ 1906.7 million |

| CAGR | 6.3 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | GE Healthcare, Fujifilm, Philips, Intelerad Medical Systems, Change Healthcare, Agfa-Gevaert, Sectra Group, Siemens Healthineers, INFINITT Healthcare, Nuance Communications, PaxeraHealth, Telepaxx, Telemis SA, DOBCO Medical Systems, eHealth Technologies, OneMedNet, Vigilant Medical, Vaultara, Tencent, itMD LLC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |