What is Global Medical Device Reprocessing Equipment Market?

The Global Medical Device Reprocessing Equipment Market refers to the industry focused on the cleaning, disinfecting, and sterilizing of medical devices so they can be safely reused. This market is essential because it helps healthcare facilities reduce costs and minimize medical waste. Reprocessing involves several steps, including cleaning, disinfection, and sterilization, to ensure that medical devices are safe for reuse. The equipment used in this market includes various machines and tools designed to handle these processes efficiently. The demand for reprocessing equipment is driven by the need for cost-effective healthcare solutions and stringent regulations regarding medical waste management. As healthcare costs continue to rise, the importance of reprocessing equipment in maintaining affordable and sustainable healthcare services becomes increasingly significant. This market is expected to grow as more healthcare facilities adopt reprocessing practices to improve their operational efficiency and reduce environmental impact.

Disinfection and Sterilization Equipment, Packaging and Delivery Equipment in the Global Medical Device Reprocessing Equipment Market:

Disinfection and sterilization equipment are crucial components of the Global Medical Device Reprocessing Equipment Market. These machines are designed to eliminate harmful microorganisms from medical devices, ensuring they are safe for reuse. Disinfection equipment typically uses chemical solutions or heat to kill bacteria, viruses, and other pathogens. Common types of disinfection equipment include automated washers, ultrasonic cleaners, and chemical disinfectors. These machines are essential for the initial cleaning phase, where visible debris and contaminants are removed from the devices. Sterilization equipment, on the other hand, goes a step further by completely eradicating all forms of microbial life. This is achieved through methods such as steam sterilization, ethylene oxide gas, and hydrogen peroxide plasma. Autoclaves are a popular type of steam sterilization equipment used in many healthcare facilities. They use high-pressure steam to penetrate and sterilize medical devices thoroughly. Ethylene oxide gas sterilizers are used for heat-sensitive devices, as the gas can sterilize without damaging the equipment. Hydrogen peroxide plasma sterilizers are another option, offering a low-temperature sterilization method that is effective and environmentally friendly. Packaging and delivery equipment are also vital in the reprocessing market. After disinfection and sterilization, medical devices need to be packaged in a way that maintains their sterility until they are used again. This involves using specialized packaging materials and sealing machines to ensure that the devices remain uncontaminated. Packaging equipment includes heat sealers, vacuum sealers, and automated packaging systems. These machines help in creating airtight packages that protect the sterilized devices from exposure to the environment. Delivery equipment ensures that the reprocessed devices are transported safely within the healthcare facility. This includes carts, trays, and storage systems designed to keep the devices organized and sterile. Proper packaging and delivery are essential to maintaining the integrity of the reprocessed devices and ensuring they are ready for use when needed. The integration of advanced technologies in disinfection, sterilization, packaging, and delivery equipment has significantly improved the efficiency and effectiveness of the reprocessing process. Automated systems and digital monitoring tools have made it easier to track and manage the reprocessing workflow, ensuring that all devices meet the required safety standards. The use of environmentally friendly sterilization methods and sustainable packaging materials has also contributed to the market's growth, as healthcare facilities strive to reduce their environmental footprint. Overall, the Global Medical Device Reprocessing Equipment Market plays a critical role in supporting the healthcare industry by providing cost-effective and sustainable solutions for medical device reuse.

Private Hospitals, Public Hospitals, Others in the Global Medical Device Reprocessing Equipment Market:

The usage of Global Medical Device Reprocessing Equipment Market in private hospitals, public hospitals, and other healthcare facilities is extensive and varied. In private hospitals, the focus is often on maintaining high standards of patient care while managing costs effectively. Reprocessing equipment helps private hospitals achieve this by allowing them to reuse expensive medical devices safely. This not only reduces the need for purchasing new devices but also minimizes medical waste, contributing to environmental sustainability. Private hospitals often invest in advanced reprocessing equipment to ensure that their devices meet stringent safety standards. This includes high-end disinfection and sterilization machines, as well as sophisticated packaging and delivery systems. The use of automated and digital technologies in these facilities helps streamline the reprocessing workflow, ensuring that devices are cleaned, sterilized, and ready for use promptly. Public hospitals, on the other hand, face different challenges. These facilities often operate with limited budgets and high patient volumes, making cost-effective solutions essential. Reprocessing equipment provides a way for public hospitals to manage their resources efficiently while maintaining patient safety. By reusing medical devices, public hospitals can reduce their procurement costs and allocate their budgets to other critical areas of patient care. The use of reprocessing equipment in public hospitals also helps address the issue of medical waste management, which is a significant concern for these facilities. Properly reprocessed devices reduce the amount of waste generated, contributing to a cleaner and safer environment. Public hospitals may use a range of reprocessing equipment, from basic disinfection machines to more advanced sterilization systems, depending on their specific needs and budget constraints. Other healthcare facilities, such as outpatient clinics, dental offices, and ambulatory surgical centers, also benefit from the Global Medical Device Reprocessing Equipment Market. These facilities often have unique requirements and may not have the same level of resources as larger hospitals. Reprocessing equipment provides a cost-effective solution for these smaller facilities, allowing them to maintain high standards of patient care without incurring significant expenses. The use of reprocessing equipment in these settings helps ensure that medical devices are safe for reuse, reducing the risk of infections and complications. This is particularly important in outpatient and ambulatory settings, where patients may be more vulnerable to infections. The availability of compact and user-friendly reprocessing equipment makes it easier for these facilities to implement effective reprocessing practices. Overall, the Global Medical Device Reprocessing Equipment Market plays a vital role in supporting various healthcare facilities by providing cost-effective and sustainable solutions for medical device reuse. Whether in private hospitals, public hospitals, or other healthcare settings, reprocessing equipment helps improve operational efficiency, reduce costs, and enhance patient safety.

Global Medical Device Reprocessing Equipment Market Outlook:

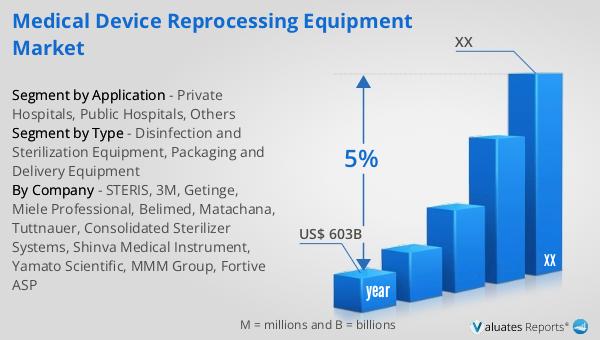

According to our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This substantial market size underscores the critical role that medical devices play in modern healthcare. The steady growth rate indicates a robust demand for medical devices, driven by factors such as technological advancements, an aging population, and the increasing prevalence of chronic diseases. As healthcare systems around the world continue to evolve, the need for innovative and reliable medical devices becomes even more pronounced. This growth trajectory also highlights the importance of the Global Medical Device Reprocessing Equipment Market, as the reuse of medical devices can significantly contribute to cost savings and sustainability in healthcare. By investing in reprocessing equipment, healthcare facilities can extend the lifespan of their medical devices, reduce waste, and ensure that they are prepared to meet the growing demand for high-quality patient care. The projected growth of the medical device market reflects the ongoing efforts to improve healthcare outcomes and the critical role that medical devices play in achieving these goals.

| Report Metric | Details |

| Report Name | Medical Device Reprocessing Equipment Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | STERIS, 3M, Getinge, Miele Professional, Belimed, Matachana, Tuttnauer, Consolidated Sterilizer Systems, Shinva Medical Instrument, Yamato Scientific, MMM Group, Fortive ASP |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |