What is Global Laser Material Processing Market?

The Global Laser Material Processing Market refers to the industry that focuses on the use of laser technology for various material processing applications. This market encompasses a wide range of laser-based processes such as cutting, welding, marking, and precision processing. Lasers are highly valued in industrial applications due to their precision, speed, and ability to work with a variety of materials including metals, plastics, and ceramics. The market is driven by the increasing demand for high-quality and efficient manufacturing processes across various industries such as automotive, electronics, aerospace, and medical devices. Technological advancements in laser systems, coupled with the growing adoption of automation in manufacturing, are also contributing to the market's growth. The global laser material processing market is characterized by a diverse range of products and services, catering to different industrial needs and applications.

Laser Cutting Machine, Laser Marking Machine, Laser Welding Machine, Precision Laser Processing System, Others in the Global Laser Material Processing Market:

Laser cutting machines are a crucial component of the global laser material processing market. These machines use a focused laser beam to cut materials with high precision and speed, making them ideal for applications in industries such as automotive, aerospace, and electronics. Laser marking machines, on the other hand, are used to engrave or mark materials with text, logos, or barcodes. This process is essential for product identification, traceability, and branding in sectors like packaging, medical devices, and consumer electronics. Laser welding machines are employed to join materials together by melting them with a laser beam. This technique offers advantages such as minimal heat distortion, high strength, and the ability to weld complex geometries, making it suitable for the automotive, aerospace, and machinery industries. Precision laser processing systems are designed for applications that require extremely high accuracy and fine detail, such as semiconductor manufacturing, medical device fabrication, and microelectronics. These systems can perform tasks like micro-cutting, micro-drilling, and micro-welding with exceptional precision. Other laser material processing equipment includes laser cleaning machines, which are used to remove contaminants from surfaces, and laser cladding machines, which are used to deposit material onto a substrate to improve its properties. The versatility and efficiency of these laser-based technologies make them indispensable in modern manufacturing processes.

Automotive, Semiconductor & Electronics, Packaging, Machine Industry, Aerospace & Defense, Food & Medicine, Oil & Gas, Others in the Global Laser Material Processing Market:

The global laser material processing market finds extensive usage across various industries due to its precision, efficiency, and versatility. In the automotive industry, laser processing is used for cutting, welding, and marking components, ensuring high-quality and reliable parts. This technology helps in reducing production time and costs while maintaining stringent quality standards. In the semiconductor and electronics sector, lasers are employed for precision cutting, drilling, and marking of electronic components and circuit boards. This ensures the accuracy and miniaturization required in modern electronic devices. The packaging industry benefits from laser marking for product identification, traceability, and anti-counterfeiting measures. Laser technology provides permanent and high-contrast markings that are essential for maintaining the integrity of packaged goods. In the machine industry, lasers are used for cutting and welding metal parts, offering high precision and strength. This is crucial for manufacturing machinery and equipment with complex geometries and tight tolerances. The aerospace and defense sectors utilize laser processing for cutting and welding aircraft components, ensuring lightweight and durable structures. Lasers are also used for marking and engraving parts for identification and traceability. In the food and medicine industries, laser technology is used for marking packaging, ensuring product safety and compliance with regulations. Lasers are also employed in medical device manufacturing for precision cutting and welding of components. The oil and gas industry uses laser processing for cutting and welding pipelines and equipment, ensuring high strength and reliability. Other industries, such as textiles and jewelry, also benefit from laser technology for cutting, engraving, and marking applications. The widespread adoption of laser material processing across these diverse industries highlights its importance in modern manufacturing and production processes.

Global Laser Material Processing Market Outlook:

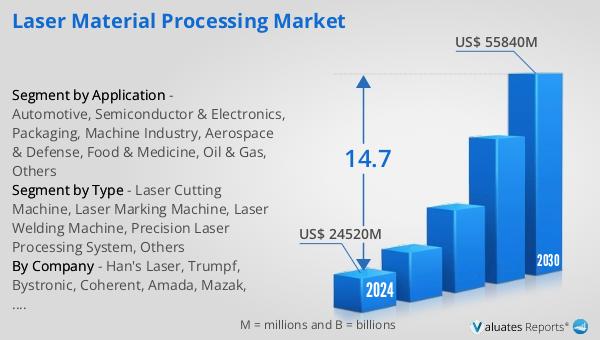

The global laser material processing market is anticipated to expand significantly, with projections indicating growth from US$ 24,520 million in 2024 to US$ 55,840 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 14.7% during the forecast period. The market is dominated by a few key players, with the top three manufacturers collectively holding over 20% of the market share. Hans Laser stands out as the largest manufacturer, commanding more than 10% of the market. The automotive industry is a major application area, accounting for approximately 30% of the market share. This substantial growth is driven by the increasing demand for efficient and precise manufacturing processes across various industries. The advancements in laser technology and the growing trend towards automation in production lines are also contributing factors. The market's expansion is further supported by the versatility of laser material processing, which caters to a wide range of applications from cutting and welding to marking and precision processing. The dominance of key players like Hans Laser underscores the competitive nature of the market and the importance of innovation and technological advancements in maintaining market leadership. The significant market share held by the automotive industry highlights the critical role of laser processing in producing high-quality and reliable automotive components.

| Report Metric | Details |

| Report Name | Laser Material Processing Market |

| Accounted market size in 2024 | US$ 24520 million |

| Forecasted market size in 2030 | US$ 55840 million |

| CAGR | 14.7 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Han's Laser, Trumpf, Bystronic, Coherent, Amada, Mazak, HGTECH, Trotec, Prima Power, Mitsubishi Electric, Jinan Bodor, Hymson Laser, HSG Laser, DR Laser, Quick Laser, Chutian Laser, Lead Laser, Gravotech, LVD Group, Tianqi Laser, Videojet Technologies Inc., IPG Photonics, Tanaka, Cincinnati, CTR Lasers, Koike, FOBA (ALLTEC GmbH), JiangSu YAWEI, United Winners Laser, Golden Laser |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |