What is Global Cutting Tool Materials Market?

The Global Cutting Tool Materials Market refers to the worldwide industry that produces and supplies materials used in cutting tools. These materials are essential for various machining processes, including drilling, milling, turning, and grinding. Cutting tools are used to remove material from a workpiece to shape or finish it to the desired dimensions and surface quality. The market encompasses a wide range of materials, each with specific properties that make them suitable for different applications. These materials include carbon steel, high-speed steel, cemented carbide, ceramics, and others. The demand for cutting tool materials is driven by the need for precision, durability, and efficiency in manufacturing processes across various industries. As technology advances and industries seek to improve productivity and reduce costs, the cutting tool materials market continues to evolve, offering innovative solutions to meet these demands. The market is influenced by factors such as industrial growth, technological advancements, and the increasing complexity of manufacturing processes.

Carbon Steel, High Speed Steel, Cemented Carbide, Ceramics, Other in the Global Cutting Tool Materials Market:

Carbon steel is one of the most basic and widely used materials in the cutting tool industry. It is known for its affordability and ease of sharpening, making it suitable for general-purpose cutting tasks. However, carbon steel tools tend to wear out quickly and are not ideal for high-speed or high-temperature applications. High-speed steel (HSS) is an improvement over carbon steel, offering better hardness and heat resistance. HSS tools can maintain their cutting edge at higher temperatures, making them suitable for more demanding applications such as drilling and milling. Cemented carbide, also known as tungsten carbide, is a composite material made of tungsten carbide particles bonded with a metallic binder. It is known for its exceptional hardness and wear resistance, making it ideal for high-speed and high-precision machining. Cemented carbide tools are commonly used in industries that require high-performance cutting, such as aerospace and automotive manufacturing. Ceramics are another advanced material used in cutting tools. They offer excellent hardness and heat resistance, making them suitable for high-speed machining of hard materials. Ceramic tools are often used in applications where other materials would fail due to high temperatures or abrasive conditions. Other materials used in cutting tools include cubic boron nitride (CBN) and polycrystalline diamond (PCD). CBN is known for its hardness and thermal stability, making it ideal for machining hard ferrous materials. PCD, on the other hand, is extremely hard and wear-resistant, making it suitable for cutting non-ferrous materials and composites. Each of these materials has its own set of advantages and limitations, and the choice of material depends on the specific requirements of the application. The global cutting tool materials market is diverse and dynamic, with continuous advancements in material science driving the development of new and improved cutting tools.

General Manufacturing, Automotive And Transportation, Construction & Building, Aerospace, Other in the Global Cutting Tool Materials Market:

The usage of cutting tool materials spans across various industries, each with its unique requirements and challenges. In general manufacturing, cutting tools are essential for producing a wide range of products, from small components to large machinery. The choice of cutting tool material in this sector depends on factors such as the type of material being machined, the required precision, and the production volume. High-speed steel and cemented carbide are commonly used in general manufacturing due to their versatility and performance. In the automotive and transportation industry, cutting tools are used to manufacture engine components, transmission parts, and other critical components. The demand for high precision and durability in this sector drives the use of advanced materials such as cemented carbide and ceramics. These materials can withstand the high temperatures and stresses associated with automotive manufacturing processes. The construction and building industry also relies heavily on cutting tools for tasks such as drilling, cutting, and shaping construction materials. Carbon steel and high-speed steel are commonly used in this sector due to their affordability and ease of use. However, for more demanding applications, such as cutting reinforced concrete or hard stones, cemented carbide and diamond tools are preferred. In the aerospace industry, cutting tools are used to manufacture complex and high-precision components for aircraft and spacecraft. The materials used in this sector must withstand extreme conditions, including high temperatures and abrasive environments. As a result, advanced materials such as ceramics, CBN, and PCD are commonly used in aerospace manufacturing. Other industries that utilize cutting tool materials include medical device manufacturing, electronics, and energy. Each of these industries has specific requirements that drive the choice of cutting tool materials. For example, the medical device industry requires tools that can produce highly precise and clean cuts, while the electronics industry demands tools that can handle delicate and intricate components. Overall, the global cutting tool materials market plays a crucial role in enabling the efficient and precise manufacturing of products across various industries.

Global Cutting Tool Materials Market Outlook:

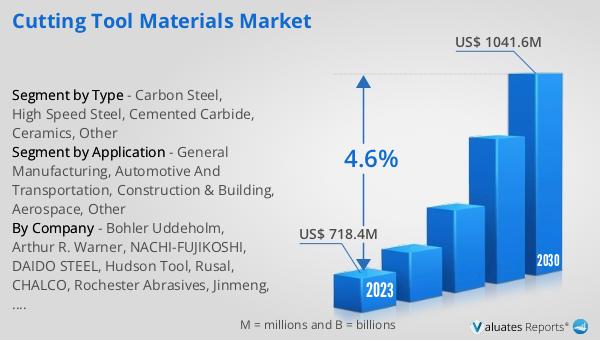

The global Cutting Tool Materials market was valued at US$ 718.4 million in 2023 and is anticipated to reach US$ 1041.6 million by 2030, witnessing a CAGR of 4.6% during the forecast period 2024-2030. This market growth reflects the increasing demand for high-performance cutting tools across various industries. As manufacturing processes become more complex and require higher precision, the need for advanced cutting tool materials continues to rise. The market's expansion is also driven by technological advancements in material science, which lead to the development of new and improved cutting tool materials. These advancements enable manufacturers to achieve better performance, longer tool life, and higher efficiency in their machining processes. Additionally, the growing emphasis on reducing production costs and improving productivity further fuels the demand for cutting tool materials. As industries continue to evolve and adopt new technologies, the global cutting tool materials market is expected to witness sustained growth, offering innovative solutions to meet the ever-changing needs of modern manufacturing.

| Report Metric | Details |

| Report Name | Cutting Tool Materials Market |

| Accounted market size in 2023 | US$ 718.4 million |

| Forecasted market size in 2030 | US$ 1041.6 million |

| CAGR | 4.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bohler Uddeholm, Arthur R. Warner, NACHI-FUJIKOSHI, DAIDO STEEL, Hudson Tool, Rusal, CHALCO, Rochester Abrasives, Jinmeng, SAINT-GORBIN, Nippon Steel Corporation, Baowu Steel, Element Six, Sandvik Hyperion, ILJIN Diamond, Hitachi, Sandvik, Xiamen Tungsten, China Minmetals Corporation, Plansee(GTP), JXTC, Japan New Metals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |