What is Global Enterprise PACS Market?

The Global Enterprise PACS (Picture Archiving and Communication System) Market is a comprehensive digital solution designed to manage, store, and distribute medical images and related data across various healthcare departments. This market encompasses a wide range of medical imaging technologies, including radiology, cardiology, dermatology, and oncology, among others. PACS systems are essential for modern healthcare facilities as they enable the efficient handling of large volumes of medical images, facilitating quick access and improved patient care. These systems integrate seamlessly with Electronic Health Records (EHRs), ensuring that patient data is readily available to healthcare providers. The global enterprise PACS market is driven by the increasing demand for advanced medical imaging solutions, the need for efficient data management, and the growing adoption of digital healthcare technologies. As healthcare providers continue to seek ways to enhance patient outcomes and streamline operations, the global enterprise PACS market is expected to play a crucial role in the future of medical imaging and data management.

Radiology PACS, Cardiology PACS, Dermatology PACS, Oncology PACS in the Global Enterprise PACS Market:

Radiology PACS, Cardiology PACS, Dermatology PACS, and Oncology PACS are specialized segments within the Global Enterprise PACS Market, each catering to the unique imaging needs of their respective medical fields. Radiology PACS is perhaps the most well-known and widely used, focusing on the storage, retrieval, and distribution of radiological images such as X-rays, CT scans, and MRIs. These systems allow radiologists to quickly access and analyze images, leading to faster diagnosis and treatment planning. Cardiology PACS, on the other hand, is tailored to the needs of cardiologists, providing tools for managing images and data related to cardiac procedures, such as echocardiograms, angiograms, and cardiac MRIs. This specialized PACS helps cardiologists monitor heart conditions, plan interventions, and track patient progress over time. Dermatology PACS is designed to handle images of the skin, including photographs and dermoscopic images used to diagnose and monitor skin conditions and diseases. This system enables dermatologists to compare images over time, aiding in the early detection of skin cancers and other dermatological issues. Oncology PACS focuses on the imaging needs of cancer diagnosis and treatment, managing images from various modalities such as PET scans, CT scans, and MRIs. This system supports oncologists in tracking tumor progression, planning radiation therapy, and evaluating treatment efficacy. Each of these specialized PACS systems plays a vital role in their respective fields, contributing to improved patient care and streamlined workflows within healthcare facilities.

Electronic Health Records (EHRS), Secure Storage of Multiple Departments, Visualization of 2D and 3D Imaging, Other in the Global Enterprise PACS Market:

The usage of the Global Enterprise PACS Market extends to several critical areas within healthcare, including Electronic Health Records (EHRs), secure storage of multiple departments, visualization of 2D and 3D imaging, and other applications. Integrating PACS with EHRs is a significant advancement, as it allows for seamless access to medical images alongside patient records. This integration ensures that healthcare providers have a comprehensive view of a patient's medical history, facilitating more accurate diagnoses and personalized treatment plans. Secure storage of medical images across multiple departments is another crucial aspect of PACS. These systems provide a centralized repository for images from various specialties, ensuring that data is stored securely and can be accessed by authorized personnel when needed. This centralized approach not only enhances data security but also improves collaboration among different departments, leading to more coordinated and efficient patient care. Visualization of 2D and 3D imaging is a key feature of modern PACS systems. Advanced visualization tools enable healthcare providers to view and manipulate images in multiple dimensions, providing a more detailed and accurate understanding of a patient's condition. This capability is particularly valuable in complex cases, such as surgical planning or tumor assessment, where precise imaging is critical. Other applications of PACS include telemedicine, where images can be shared with specialists in remote locations for consultation, and research, where large datasets of medical images can be analyzed to identify trends and improve treatment protocols. Overall, the Global Enterprise PACS Market plays a pivotal role in enhancing the efficiency, accuracy, and quality of healthcare delivery.

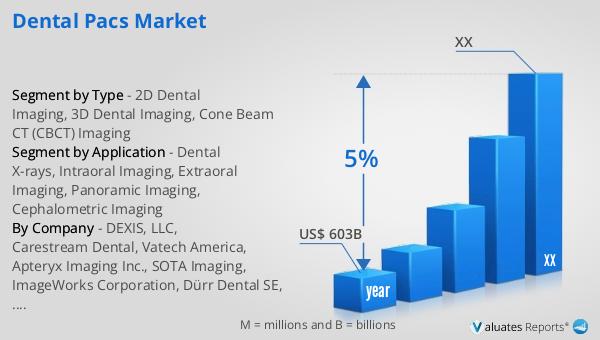

Global Enterprise PACS Market Outlook:

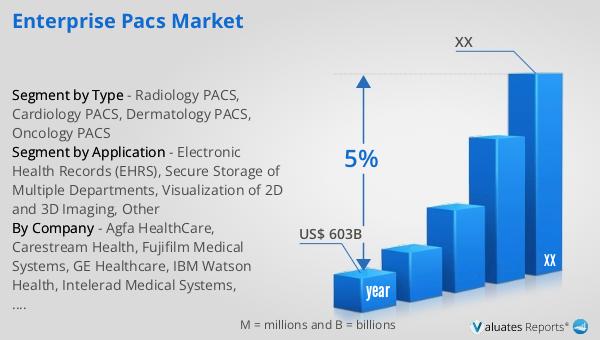

According to our research, the global market for medical devices is projected to reach approximately US$ 603 billion in 2023, with an anticipated growth rate of 5% CAGR over the next six years. This robust growth is indicative of the increasing demand for advanced medical technologies and the continuous innovation within the healthcare sector. The expansion of the medical device market is driven by several factors, including the rising prevalence of chronic diseases, an aging population, and the growing emphasis on early diagnosis and preventive care. Additionally, advancements in medical imaging, minimally invasive procedures, and digital health solutions are contributing to the market's growth. As healthcare providers strive to improve patient outcomes and operational efficiency, the adoption of cutting-edge medical devices is becoming increasingly essential. The projected growth of the global medical device market underscores the importance of ongoing research and development, as well as the need for regulatory frameworks that support innovation while ensuring patient safety. This dynamic market landscape presents numerous opportunities for stakeholders, including manufacturers, healthcare providers, and investors, to collaborate and drive the future of healthcare forward.

| Report Metric | Details |

| Report Name | Enterprise PACS Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Agfa HealthCare, Carestream Health, Fujifilm Medical Systems, GE Healthcare, IBM Watson Health, Intelerad Medical Systems, McKesson Corporation, Philips Healthcare, Sectra AB, Siemens Healthineers, TeraRecon, Inc., Infinitt Healthcare Co., Ltd., Novarad Corporation, Visage Imaging, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |