What is Global Ultrasonically Activated Scalpel (UAS) Market?

The Global Ultrasonically Activated Scalpel (UAS) Market is a specialized segment within the broader medical devices industry. Ultrasonically Activated Scalpels are advanced surgical instruments that utilize ultrasonic vibrations to cut and coagulate tissue simultaneously. This technology offers several advantages over traditional surgical tools, including reduced blood loss, minimized thermal damage to surrounding tissues, and enhanced precision. These scalpels are widely used in various surgical procedures, such as general surgery, gynecology, urology, and cardiovascular surgery. The market for UAS is driven by the increasing prevalence of chronic diseases, rising demand for minimally invasive surgeries, and technological advancements in surgical instruments. Additionally, the growing number of surgical procedures worldwide and the increasing adoption of UAS in emerging economies contribute to the market's growth. The market is characterized by the presence of several key players who are continuously investing in research and development to introduce innovative products and gain a competitive edge.

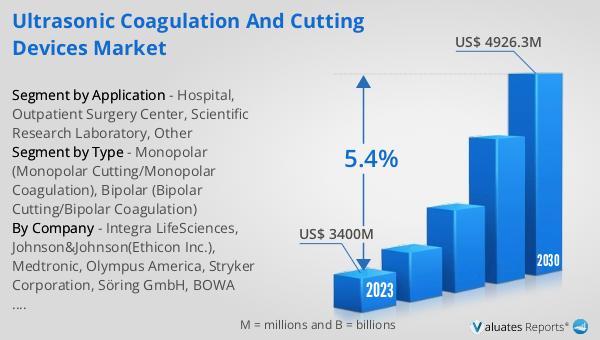

Monopolar (Monopolar Cutting/Monopolar Coagulation), Bipolar (Bipolar Cutting/Bipolar Coagulation) in the Global Ultrasonically Activated Scalpel (UAS) Market:

Monopolar and Bipolar technologies are two primary methods used in the Global Ultrasonically Activated Scalpel (UAS) Market. Monopolar technology involves a single electrode that delivers electrical energy to the tissue, which then returns through a grounding pad attached to the patient's body. This method is commonly used for cutting and coagulating tissues during surgical procedures. Monopolar cutting is highly effective for precise tissue dissection, while monopolar coagulation helps control bleeding by sealing blood vessels. However, the use of monopolar technology requires careful monitoring to prevent unintended thermal damage to surrounding tissues. On the other hand, Bipolar technology uses two electrodes placed close to each other, allowing the electrical current to pass between them and through the tissue. This method offers greater control and precision, making it ideal for delicate surgical procedures. Bipolar cutting provides clean and precise incisions, while bipolar coagulation effectively seals blood vessels with minimal thermal spread. The use of bipolar technology reduces the risk of accidental burns and enhances patient safety. Both monopolar and bipolar technologies are integral to the UAS market, offering surgeons versatile tools to perform a wide range of surgical procedures with improved outcomes. The choice between monopolar and bipolar technology depends on the specific surgical requirements and the surgeon's preference. As the UAS market continues to evolve, advancements in both monopolar and bipolar technologies are expected to further enhance the efficiency and safety of surgical procedures.

Hospital, Outpatient Surgery Center, Scientific Research Laboratory, Other in the Global Ultrasonically Activated Scalpel (UAS) Market:

The usage of Global Ultrasonically Activated Scalpel (UAS) Market spans across various healthcare settings, including hospitals, outpatient surgery centers, scientific research laboratories, and other medical facilities. In hospitals, UAS is extensively used in operating rooms for a wide range of surgical procedures. The precision and efficiency of UAS make it an invaluable tool for surgeons, enabling them to perform complex surgeries with reduced blood loss and minimal thermal damage to surrounding tissues. This results in faster recovery times and improved patient outcomes. In outpatient surgery centers, UAS is favored for minimally invasive procedures that require high precision and minimal tissue trauma. The use of UAS in these settings allows for shorter procedure times, reduced postoperative pain, and quicker patient discharge, enhancing the overall patient experience. Scientific research laboratories also benefit from the use of UAS, particularly in experimental surgeries and tissue studies. The precise cutting and coagulating capabilities of UAS enable researchers to conduct detailed and controlled experiments, contributing to advancements in medical research and surgical techniques. Additionally, UAS finds applications in other medical facilities, such as specialized clinics and ambulatory care centers, where it is used for various surgical interventions. The versatility and effectiveness of UAS make it a valuable asset in diverse healthcare environments, driving its adoption and market growth.

Global Ultrasonically Activated Scalpel (UAS) Market Outlook:

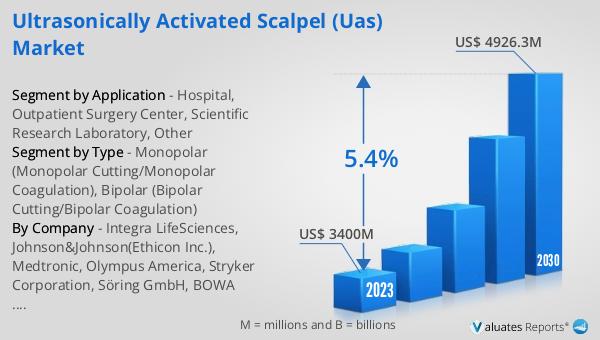

The global Ultrasonically Activated Scalpel (UAS) market was valued at US$ 3400 million in 2023 and is anticipated to reach US$ 4926.3 million by 2030, witnessing a CAGR of 5.4% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for advanced surgical instruments that offer precision, efficiency, and improved patient outcomes. The rising prevalence of chronic diseases, coupled with the growing number of surgical procedures worldwide, is driving the adoption of UAS in various healthcare settings. Technological advancements and continuous research and development efforts by key market players are also contributing to the market's expansion. As healthcare providers seek to enhance surgical outcomes and patient safety, the demand for ultrasonically activated scalpels is expected to rise, further propelling the market's growth.

| Report Metric | Details |

| Report Name | Ultrasonically Activated Scalpel (UAS) Market |

| Accounted market size in 2023 | US$ 3400 million |

| Forecasted market size in 2030 | US$ 4926.3 million |

| CAGR | 5.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Integra LifeSciences, Johnson&Johnson(Ethicon Inc.), Medtronic, Olympus America, Stryker Corporation, Söring GmbH, BOWA MEDICAL, Bioventus(MISONIX,Inc.), Genesis MedTech(Reach Surgical), Apollo Technosystems, Ethicon Endo-Surgery, VDW GmbH, Advanced Instrumentations, MISONIX,Inc., B. Braun Holding GmbH&Co.KG, CONMED, Heritage Electromedicine GmbH, LED SpA, Cooper Medical,Inc., Miconvey, Lepu Medical Technology, Innolcon Medical Technology Co.,Ltd., Hocermed (Tianjin) Medical Technology Co.,Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |