What is Global Tilapia Market?

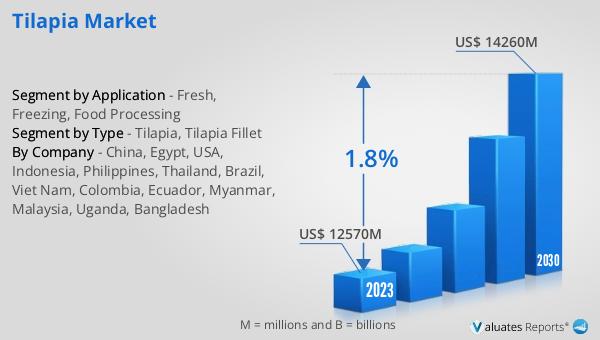

The global Tilapia market is projected to experience significant growth over the coming years. By 2024, the market is expected to reach a valuation of approximately US$ 12,820 million, and it is anticipated to further expand to US$ 14,260 million by 2030. This growth trajectory represents a Compound Annual Growth Rate (CAGR) of 1.8% during the forecast period. The market is dominated by the top five manufacturers, who collectively hold about 70% of the market share. Among the various product segments, Tilapia stands out as the largest, accounting for nearly 60% of the market share. This indicates a strong consumer preference and demand for Tilapia products, which is likely to drive the market's growth in the coming years. The increasing popularity of Tilapia can be attributed to its versatility in culinary applications, nutritional benefits, and relatively low production costs compared to other types of fish. As a result, Tilapia is becoming a staple in many households and food establishments worldwide, further bolstering its market presence.

Tilapia, Tilapia Fillet in the Global Tilapia Market:

Tilapia is a type of freshwater fish that is native to Africa but has been introduced to various parts of the world due to its adaptability and ease of farming. It is one of the most widely farmed fish globally, thanks to its rapid growth rate, resistance to diseases, and ability to thrive in diverse environmental conditions. Tilapia is often referred to as the "aquatic chicken" because of its mild flavor, versatility in cooking, and affordability. It is a popular choice for consumers looking for a healthy and sustainable source of protein. Tilapia fillets, in particular, are highly sought after in the global market. These fillets are typically boneless and skinless, making them convenient for cooking and consumption. They can be prepared in various ways, including grilling, baking, frying, and steaming, which adds to their appeal. The global Tilapia market is driven by the increasing demand for healthy and nutritious food options. Tilapia is rich in protein, low in fat, and contains essential nutrients such as omega-3 fatty acids, vitamins, and minerals. This makes it an attractive option for health-conscious consumers. Additionally, the relatively low cost of Tilapia compared to other fish species makes it accessible to a broader range of consumers. The global Tilapia market is also influenced by the growing trend of aquaculture, which is the farming of aquatic organisms. Aquaculture has become a vital component of the global food supply chain, providing a sustainable and efficient way to produce fish and other seafood. Tilapia farming, in particular, has gained popularity due to its high yield and low environmental impact. The use of advanced farming techniques and technologies has further enhanced the productivity and quality of Tilapia, making it a competitive product in the global market. The market for Tilapia fillets is also supported by the increasing demand from the food service industry. Restaurants, hotels, and catering services are incorporating Tilapia into their menus due to its versatility and ease of preparation. The growing popularity of seafood dishes and the rising trend of healthy eating have contributed to the increased consumption of Tilapia fillets. Furthermore, the global Tilapia market is influenced by the expanding distribution channels. Supermarkets, hypermarkets, and online retail platforms are making Tilapia products more accessible to consumers. The convenience of purchasing Tilapia fillets through these channels has boosted their sales and market penetration. In conclusion, the global Tilapia market is experiencing steady growth due to the increasing demand for healthy and affordable protein sources. Tilapia's versatility, nutritional benefits, and ease of farming make it a popular choice among consumers and food service providers. The market is further supported by the growing trend of aquaculture and the expansion of distribution channels. As a result, Tilapia is expected to continue its upward trajectory in the global market.

Fresh, Freezing, Food Processing in the Global Tilapia Market:

The global Tilapia market finds its usage in various areas, including fresh, freezing, and food processing. Fresh Tilapia is highly valued for its taste and nutritional benefits. It is often sold whole or as fillets in local markets and supermarkets. Fresh Tilapia is a popular choice among consumers who prefer to cook their meals from scratch. It can be grilled, baked, fried, or steamed, making it a versatile ingredient in various cuisines. The demand for fresh Tilapia is driven by the increasing awareness of healthy eating habits and the preference for fresh and natural food products. Consumers are becoming more health-conscious and are seeking out fresh fish options that are rich in protein and low in fat. Fresh Tilapia meets these criteria, making it a preferred choice for many. Freezing is another significant area of usage in the global Tilapia market. Frozen Tilapia products are widely available in supermarkets and online retail platforms. Freezing helps to preserve the fish's freshness and nutritional value, making it a convenient option for consumers. Frozen Tilapia fillets are particularly popular as they are easy to store and can be used in various recipes. The freezing process also extends the shelf life of Tilapia, reducing food waste and ensuring a steady supply of the product throughout the year. The demand for frozen Tilapia is driven by the busy lifestyles of consumers who seek convenient and quick meal options. Frozen Tilapia can be easily thawed and cooked, making it a practical choice for those with limited time for meal preparation. Food processing is another crucial area of usage in the global Tilapia market. Processed Tilapia products include items such as fish sticks, fish fillets, and fish patties. These products are often breaded, seasoned, and pre-cooked, making them ready-to-eat or easy to prepare. The food processing industry utilizes Tilapia due to its mild flavor and firm texture, which makes it suitable for various processed food products. The demand for processed Tilapia products is driven by the growing trend of convenience foods. Consumers are increasingly looking for ready-to-eat or easy-to-prepare meal options that fit into their busy schedules. Processed Tilapia products cater to this demand by offering quick and convenient meal solutions. Additionally, the food processing industry benefits from the consistent supply and cost-effectiveness of Tilapia, making it a preferred choice for producing processed fish products. In conclusion, the global Tilapia market finds its usage in fresh, freezing, and food processing areas. Fresh Tilapia is valued for its taste and nutritional benefits, making it a popular choice among health-conscious consumers. Frozen Tilapia products offer convenience and extended shelf life, catering to the busy lifestyles of modern consumers. Processed Tilapia products provide quick and easy meal solutions, meeting the demand for convenience foods. The versatility and affordability of Tilapia make it a valuable commodity in the global market, driving its usage across various sectors.

Global Tilapia Market Outlook:

English: #TilapiaMarket #GlobalSeafood #HealthyEating #Aquaculture #FreshTilapia #FrozenTilapia #FoodProcessing #SustainableProtein #SeafoodLovers #ConvenientMeals

| Report Metric | Details |

| Report Name | Tilapia Market |

| Accounted market size in 2024 | US$ 12820 million |

| Forecasted market size in 2030 | US$ 14260 million |

| CAGR | 1.8 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | USA, Indonesia, Philippines, Thailand, Brazil, Viet Nam, Colombia, Ecuador, Myanmar, Malaysia, Uganda, Bangladesh |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |