What is Global Re-dispersible Latex Powder (RDP) Market?

The Global Re-dispersible Latex Powder (RDP) Market is a specialized segment within the broader chemical industry, focusing on the production and distribution of re-dispersible latex powders. These powders are essentially polymer emulsions that have been transformed into a powder form through spray drying. When mixed with water, they re-disperse back into a liquid form, making them highly versatile for various applications. RDPs are primarily used in the construction industry, where they enhance the properties of cement and gypsum-based products. They improve adhesion, flexibility, and water resistance, making them ideal for use in tile adhesives, exterior insulation systems, and self-leveling compounds. The market for RDPs is driven by the growing demand for high-performance building materials, particularly in emerging economies where construction activities are booming. Additionally, the push for sustainable and energy-efficient building solutions is further propelling the market. The global RDP market is characterized by a high level of competition, with several key players dominating the landscape. These companies are continually investing in research and development to innovate and improve the performance characteristics of their products.

VAE Type, VAE-Veo Va Type, Others in the Global Re-dispersible Latex Powder (RDP) Market:

In the Global Re-dispersible Latex Powder (RDP) Market, there are several types of products, each with unique properties and applications. The VAE Type, or Vinyl Acetate Ethylene, is the most prevalent, accounting for over 80% of the market share. VAE-based RDPs are known for their excellent adhesion, flexibility, and water resistance, making them ideal for a wide range of construction applications. They are particularly effective in tile adhesives, where strong bonding and flexibility are crucial. The VAE-Veo Va Type is another significant segment within the RDP market. This type combines the properties of VAE with those of Veo Va, or Vinyl Ester of Versatic Acid. The result is a product that offers enhanced chemical resistance and durability. VAE-Veo Va RDPs are often used in applications where exposure to harsh chemicals or extreme weather conditions is a concern. They are commonly found in exterior insulation and finish systems (EIFS) and other demanding construction environments. Other types of RDPs include those based on acrylic, styrene-butadiene, and other polymers. These products are typically used in specialized applications where specific performance characteristics are required. For example, acrylic-based RDPs are known for their excellent UV resistance and are often used in exterior coatings and sealants. Styrene-butadiene RDPs, on the other hand, offer superior water resistance and are commonly used in waterproofing applications. The diversity of RDP types allows manufacturers to tailor their products to meet the specific needs of different construction projects. This flexibility is one of the key factors driving the growth of the RDP market. As construction techniques and materials continue to evolve, the demand for high-performance, versatile building products like RDPs is expected to increase.

Exterior Insulation and Finish Systems (EIFS), Construction and Tile Adhesives, Putty Powder, Dry-mix Mortars, Self-leveling Flooring Compounds, Caulks, Other Applications in the Global Re-dispersible Latex Powder (RDP) Market:

The Global Re-dispersible Latex Powder (RDP) Market finds extensive usage in various construction-related applications, each benefiting from the unique properties of RDPs. In Exterior Insulation and Finish Systems (EIFS), RDPs are used to enhance the adhesion and flexibility of the insulation layers, ensuring that they remain firmly attached to the building structure while accommodating any movement or thermal expansion. This results in improved energy efficiency and durability of the building envelope. In the realm of Construction and Tile Adhesives, RDPs play a crucial role in improving the bonding strength and flexibility of the adhesives. This ensures that tiles remain securely attached to surfaces, even in areas subjected to high moisture or temperature fluctuations. The enhanced flexibility also helps in preventing cracks and other forms of damage. Putty Powder, another significant application area, benefits from the addition of RDPs by gaining improved workability, adhesion, and crack resistance. This makes it easier to apply and ensures a smooth, durable finish. Dry-mix Mortars, which are used in a variety of construction tasks such as plastering, rendering, and screeding, also see significant performance improvements with the inclusion of RDPs. The powders enhance the workability, adhesion, and water resistance of the mortars, making them more effective and durable. Self-leveling Flooring Compounds, which require a high degree of flowability and smoothness, benefit from the addition of RDPs by achieving a more uniform and level surface. This is particularly important in commercial and industrial settings where floor flatness is critical. In Caulks, RDPs improve the flexibility and adhesion of the sealants, ensuring that they remain effective in sealing joints and gaps even under movement or stress. Other Applications of RDPs include their use in waterproofing membranes, repair mortars, and various specialty coatings. In each of these applications, the unique properties of RDPs, such as improved adhesion, flexibility, and water resistance, contribute to enhanced performance and durability.

Global Re-dispersible Latex Powder (RDP) Market Outlook:

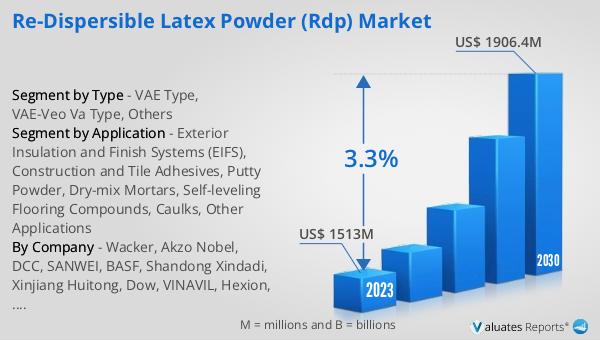

The global market for Re-dispersible Latex Powder (RDP) is anticipated to expand from $1,568.9 million in 2024 to $1,906.4 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.3% over the forecast period. The top four global manufacturers collectively hold a market share exceeding 40%. Among the various product types, the VAE Type stands out as the largest segment, commanding over 80% of the market share. This dominance is attributed to the superior properties of VAE-based RDPs, such as excellent adhesion, flexibility, and water resistance, which make them highly suitable for a wide range of construction applications. The market's growth is driven by the increasing demand for high-performance building materials, particularly in emerging economies where construction activities are on the rise. Additionally, the push for sustainable and energy-efficient building solutions is further fueling the demand for RDPs. The competitive landscape of the RDP market is characterized by continuous innovation and product development, as manufacturers strive to meet the evolving needs of the construction industry.

| Report Metric | Details |

| Report Name | Re-dispersible Latex Powder (RDP) Market |

| Accounted market size in 2024 | US$ 1568.9 million |

| Forecasted market size in 2030 | US$ 1906.4 million |

| CAGR | 3.3 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Wacker, Akzo Nobel, DCC, SANWEI, BASF, Shandong Xindadi, Xinjiang Huitong, Dow, VINAVIL, Hexion, Ashland, Wanwei, Acquos, Organik, Fenghua, Shaanxi Xutai, Puyang Yintai, Gemez Chemical, Guangzhou Yuanye, Zhaojia, Sailun Building, Henan Tiansheng Chem, Xinjiang Su Nok, Mizuda Bioscience, Shandong Micron |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |