What is Global High Purity Palladiums Market?

The Global High Purity Palladiums Market refers to a specialized segment within the broader precious metals industry, focusing on the production, distribution, and sale of exceptionally pure palladium. This market caters to a niche but critical demand for high-grade palladium, primarily used in various high-tech applications, including electronics, automotive catalysts, and hydrogen purification systems. Palladium, a platinum group metal, is prized for its excellent catalytic properties, corrosion resistance, and electrical conductivity. The market's significance stems from the metal's pivotal role in reducing harmful emissions, advancing renewable energy technologies, and its use in manufacturing sophisticated electronic components. As industries worldwide strive for more sustainable and efficient technologies, the demand for high purity palladium is expected to grow, reflecting its essential role in modern technological advancements and environmental solutions. This market's dynamics are influenced by factors such as mining output, recycling rates, technological innovations, and global economic trends, which together determine the availability and price of high purity palladium.

Powder, Ingots, Others in the Global High Purity Palladiums Market:

Diving into the Global High Purity Palladiums Market, we find it segmented by product forms such as Powder, Ingots, and Others, each catering to specific industrial needs and applications. Powdered high purity palladium, with its extensive surface area, is crucial for chemical reactions in catalytic converters used in the automotive industry and in the production of electronics, where it serves as a conductive paste in multilayer ceramic capacitors. Ingots, on the other hand, are preferred for their ease of storage and transport, finding their use in investment, jewelry making, and as a raw material in the manufacturing of high-purity palladium components for various industrial applications. The 'Others' category includes forms like palladium sponge and wire, essential for specialized applications such as dental alloys and fine jewelry, respectively. The diversity in product forms underscores the versatility of high purity palladium, making it indispensable across a broad spectrum of industries. This segmentation not only reflects the varied applications of palladium but also highlights the market's adaptability in meeting specific industrial requirements, thereby driving innovation and efficiency in its applications.

Electronic, Industrial, Others in the Global High Purity Palladiums Market:

The usage of the Global High Purity Palladiums Market spans across Electronic, Industrial, and Other sectors, showcasing the metal's versatility and critical role in modern technology and industrial processes. In the electronics sector, high purity palladium is a key component in manufacturing capacitors and conductive inks, owing to its excellent electrical conductivity and resistance to oxidation. This ensures the reliability and longevity of electronic devices, from smartphones to sophisticated aerospace systems. In the industrial realm, palladium's catalytic properties are harnessed in automotive exhaust systems to reduce harmful emissions, playing a vital role in environmental protection efforts. Additionally, its use in hydrogen purification technologies is pivotal for fuel cell development, marking a significant step towards cleaner energy sources. The 'Others' category encompasses uses in jewelry, where its luster and durability make it a preferred material, and in dental applications, where its biocompatibility and mechanical properties are valued. This wide-ranging application of high purity palladium underscores its importance in advancing both technological innovation and sustainability, reflecting its indispensable role across various sectors.

Global High Purity Palladiums Market Outlook:

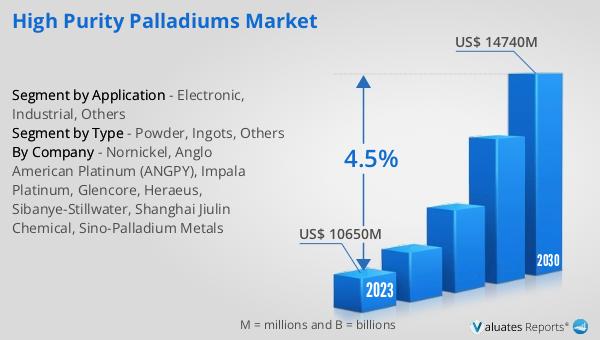

The market outlook for Global High Purity Palladiums presents a promising future, with the market's value estimated at US$ 10,650 million in 2023, and projections suggest it will ascend to US$ 14,740 million by 2030. This growth trajectory, marked by a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030, underscores the increasing demand and significance of high purity palladium across various industries. The market's expansion is further highlighted by the dominance of the world's three major manufacturers, who collectively are expected to hold more than 70% of the market share, reflecting a concentrated industry landscape. This outlook not only signifies the robust health and potential of the Global High Purity Palladiums Market but also points towards the strategic importance of these key players in shaping the market dynamics. Their significant market share underscores their influence in setting industry standards, driving technological advancements, and meeting the growing demand for high purity palladium, essential for a wide range of applications from environmental technologies to electronic devices.

| Report Metric | Details |

| Report Name | High Purity Palladiums Market |

| Accounted market size in 2023 | US$ 10650 million |

| Forecasted market size in 2030 | US$ 14740 million |

| CAGR | 4.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Nornickel, Anglo American Platinum (ANGPY), Impala Platinum, Glencore, Heraeus, Sibanye-Stillwater, Shanghai Jiulin Chemical, Sino-Palladium Metals |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |