What is Global Large Dozers Market?

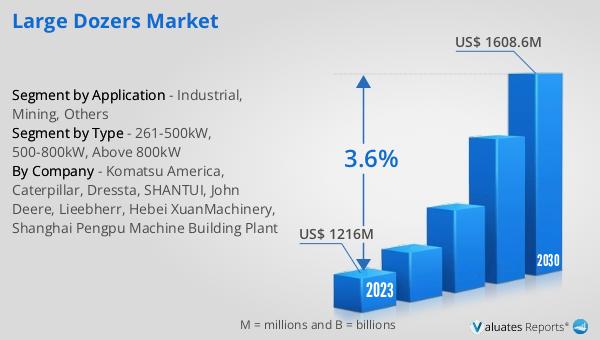

The Global Large Dozers Market is a sector that focuses on the production, distribution, and sale of heavy-duty dozers used across various industries. These machines are pivotal in operations that require significant earthmoving, grading, and material handling capabilities. Large dozers, as the name suggests, are on the higher end of the size and power spectrum, designed to tackle the most demanding tasks in construction, mining, and other industrial applications. The market's value, pegged at US$ 1216 million in 2023, underscores the critical role these machines play in modern infrastructure development and resource extraction. With an expected growth to US$ 1608.6 million by 2030, the market is set to expand at a compound annual growth rate (CAGR) of 3.6% over the forecast period from 2024 to 2030. This growth trajectory highlights the increasing demand for more efficient, powerful, and technologically advanced dozers capable of meeting the evolving needs of industries reliant on heavy machinery for their operations. The Global Large Dozers Market thus represents a significant component of the global construction and mining equipment industry, reflecting broader economic and industrial trends.

261-500kW, 500-800kW, Above 800kW in the Global Large Dozers Market:

Diving into the specifics of the Global Large Dozers Market, the segmentation based on power output, namely 261-500kW, 500-800kW, and Above 800kW, offers a detailed view of the market's dynamics. Dozers within the 261-500kW range are versatile machines capable of performing a wide array of tasks, from grading and clearing to heavy earthmoving, making them suitable for both construction and mining applications. The mid-range, 500-800kW dozers, offer increased power and efficiency, ideal for more demanding tasks that require additional horsepower and durability. These machines are often the workhorses in large-scale construction projects and open-pit mining operations where their robustness and reliability can significantly enhance productivity. The highest category, Above 800kW, includes some of the most powerful dozers available on the market. These behemoths are designed for the most challenging environments and tasks, such as moving large volumes of earth and rock in mining operations or large-scale land clearing and development projects. The segmentation of the Global Large Dozers Market by power output not only highlights the diverse applications of these machines but also underscores the technological advancements and engineering prowess that go into their development. Manufacturers in this space continuously innovate to offer machines that provide not just greater power, but also improved efficiency, reliability, and environmental compliance, catering to the evolving needs of the global industries they serve.

Industrial, Mining, Others in the Global Large Dozers Market:

The usage of the Global Large Dozers Market spans across various sectors, notably in industrial, mining, and other areas. In the industrial sector, large dozers play a crucial role in the construction and maintenance of infrastructure, including roads, bridges, and buildings. Their ability to move large volumes of materials quickly and efficiently makes them indispensable in projects that require significant earthmoving and grading tasks. In mining, large dozers are fundamental in the extraction process, used for stripping, overburden removal, and stockpile management. Their robust build and high power output enable them to operate in the harsh conditions of mining sites, contributing to the efficiency and safety of mining operations. Beyond these, large dozers find applications in other areas such as agriculture, where they are used for land clearing and preparation, and in waste management, where they help in landfill operations. The versatility of large dozers, coupled with advancements in technology that enhance their performance and environmental compliance, ensures their continued relevance across these sectors. The Global Large Dozers Market, therefore, not only reflects the demand for heavy machinery in traditional industries like construction and mining but also its adaptability and utility in addressing the needs of various other applications.

Global Large Dozers Market Outlook:

Regarding the market outlook for the Global Large Dozers Market, it's noteworthy to mention that the sector, valued at US$ 1216 million in 2023, is on a growth trajectory with projections estimating it to reach US$ 1608.6 million by 2030. This anticipated growth, marked by a compound annual growth rate (CAGR) of 3.6% during the forecast period from 2024 to 2030, signifies the robust demand and expanding applications for large dozers across the globe. The market's expansion is driven by the need for more efficient, technologically advanced, and environmentally friendly heavy machinery in construction, mining, and other industrial activities. As industries strive to increase productivity while minimizing environmental impact, the development and adoption of large dozers that meet these criteria are expected to rise. This outlook underscores the importance of innovation and sustainability in the heavy machinery sector, reflecting broader trends towards more responsible and efficient industrial practices. The Global Large Dozers Market, therefore, represents a dynamic and evolving segment of the global economy, with significant implications for industries reliant on heavy equipment.

| Report Metric | Details |

| Report Name | Large Dozers Market |

| Accounted market size in 2023 | US$ 1216 million |

| Forecasted market size in 2030 | US$ 1608.6 million |

| CAGR | 3.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Komatsu America, Caterpillar, Dressta, SHANTUI, John Deere, Lieebherr, Hebei XuanMachinery, Shanghai Pengpu Machine Building Plant |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |