What is Global Antiwear Hydraulic Oils Market?

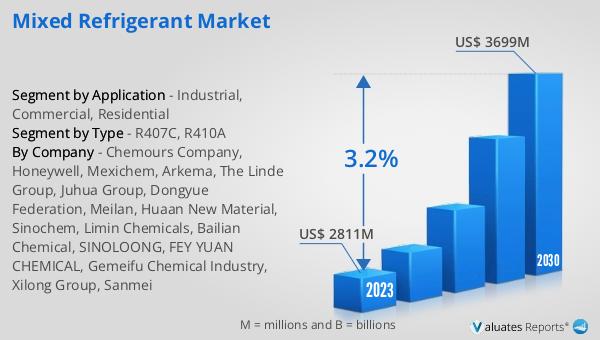

The Global Antiwear Hydraulic Oils Market is a specialized segment within the broader lubricants industry, focusing on products designed to prevent wear and tear in hydraulic systems. These oils are engineered to minimize the friction between moving parts, thereby extending the lifespan of machinery and reducing downtime due to maintenance. The market for these oils is driven by the need for efficient and reliable hydraulic systems in various industries, including construction, manufacturing, and automotive. As machinery becomes more sophisticated and the demand for higher performance and sustainability grows, the importance of antiwear hydraulic oils becomes increasingly critical. These oils not only protect the hydraulic systems but also contribute to the energy efficiency and overall performance of the equipment they lubricate. With a valuation of US$ 4351 million in 2023, the market is expected to expand to US$ 5717.1 million by 2030, growing at a compound annual growth rate (CAGR) of 3.6% from 2024 to 2030. This growth trajectory underscores the rising demand for high-quality lubricants that can meet the stringent requirements of modern machinery and industrial applications.

#32, #46, #68, Others in the Global Antiwear Hydraulic Oils Market:

Diving into the specifics of the Global Antiwear Hydraulic Oils Market, we find a range of products categorized mainly by their viscosity grades, such as #32, #46, #68, among others. Each of these grades serves different machinery needs and operational conditions. For instance, the #32 grade oil is typically used in environments where lower viscosity is required for finer control or in colder climates. On the other hand, #46 and #68 oils are suited for heavier duty applications where higher viscosity provides better lubrication under high pressure and temperature conditions. These grades cover a broad spectrum of industrial and mobile hydraulic systems, ensuring that there's a specific type of oil optimized for virtually any scenario. The diversity within this market segment is a testament to the technological advancements and rigorous research and development efforts by manufacturers to cater to the evolving needs of modern machinery. As industries continue to push for higher efficiency and performance, the demand for these specialized hydraulic oils is expected to grow, reflecting the critical role they play in operational reliability and equipment longevity.

Industrial Gear, Hydraulic Pump, Mechanical Equipment Hydraulic System, Others in the Global Antiwear Hydraulic Oils Market:

The usage of Global Antiwear Hydraulic Oils spans several critical areas, including Industrial Gear, Hydraulic Pump, Mechanical Equipment Hydraulic System, among others. In Industrial Gear applications, these oils help in reducing the friction and wear on the gears, which are subjected to high loads and speeds. For Hydraulic Pumps, the right antiwear hydraulic oil can significantly enhance the pump's efficiency and longevity by protecting it from wear and corrosion. In Mechanical Equipment Hydraulic Systems, these oils are indispensable for maintaining the smooth operation of various components, ensuring that they work seamlessly under different pressures and temperatures. The "Others" category encompasses a wide range of applications, including but not limited to, automotive braking systems, aerospace hydraulics, and marine equipment. The versatility and effectiveness of antiwear hydraulic oils in these applications underscore their importance in modern industrial and mechanical operations. By reducing wear and tear, these oils not only prolong the life of the equipment but also contribute to energy savings and reduced maintenance costs, highlighting their critical role in operational efficiency and sustainability.

Global Antiwear Hydraulic Oils Market Outlook:

Regarding the market outlook for Global Antiwear Hydraulic Oils, it's observed that the market, which was valued at US$ 4351 million in the year 2023, is on a growth trajectory. It's projected to escalate to a valuation of US$ 5717.1 million by the year 2030. This growth is expected to occur at a steady compound annual growth rate (CAGR) of 3.6% during the forecast period spanning from 2024 to 2030. This positive outlook is indicative of the increasing reliance on high-performance lubricants across various industries to ensure the longevity and efficiency of hydraulic systems. As businesses continue to seek solutions that can enhance operational reliability and reduce downtime, the demand for antiwear hydraulic oils is anticipated to rise. This market growth reflects the broader trends towards industrial automation and the adoption of sophisticated machinery, which necessitates the use of advanced lubrication solutions. Thus, the Global Antiwear Hydraulic Oils Market is set to witness significant expansion, driven by the need for high-quality lubricants that can meet the stringent requirements of modern industrial applications.

| Report Metric | Details |

| Report Name | Antiwear Hydraulic Oils Market |

| Accounted market size in 2023 | US$ 4351 million |

| Forecasted market size in 2030 | US$ 5717.1 million |

| CAGR | 3.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Mobil, Caltex, AMSOIL, Sinopec Sinolube, Nemco, China Petroleum Lubricants Corporation, Shell Tellus, Tianneng Battery Group, BOLUKE, Kroneseder, Hanzghou Derunbao, Valvoline, Chevron Oronite, SWEPCO, Castrol, Sinclair Oil Corporation, Royal MFG, Lucas Oil |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |